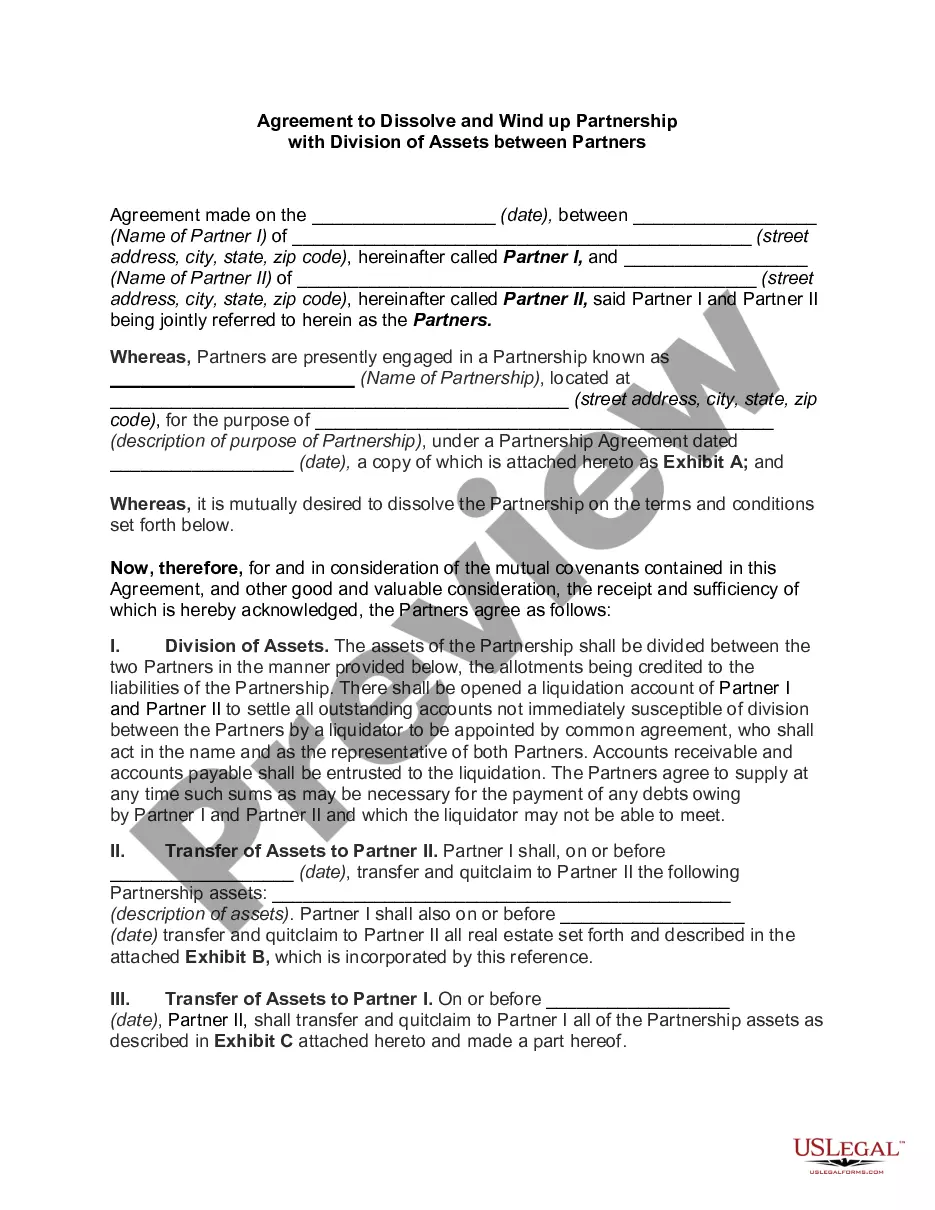

Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner

Description

How to fill out Agreement To Dissolve And Wind Up Partnership Between Surviving Partners And Estate Of Deceased Partner?

Have you ever found yourself in a situation where you frequently require documents for business or personal purposes almost every day.

There is a plethora of valid document templates accessible online, yet finding trustworthy ones can be challenging.

US Legal Forms provides an extensive collection of form templates, including the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner, designed to meet both federal and state requirements.

Choose a convenient document format and download your copy.

Access all the document templates you have purchased from the My documents section. You can download another copy of the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner any time you need it. Just select the desired form to download or print the document template. Use US Legal Forms, the most extensive collection of valid forms, to save time and avoid errors. The service provides properly crafted legal document templates suitable for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Then, you can retrieve the Indiana Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is suitable for your specific city/county.

- Utilize the Preview button to review the form.

- Examine the details to confirm that you have selected the correct document.

- If the document is not what you are looking for, utilize the Search field to find a form that meets your needs and requirements.

- Once you have located the appropriate document, click Get now.

- Select the pricing plan you prefer, complete the required information to create your account, and purchase the order using PayPal, Visa, or Mastercard.

Form popularity

FAQ

Only partnership assets are to be divided among partners upon dissolution. If assets were used by the partnership, but did not form part of the partnership assets, then those assets will not be divided upon dissolution (see, for example, Hansen v Hansen, 2005 SKQB 436).

Upon the winding up of a limited partnership, the assets shall be distributed as follows: (1) To creditors, including partners who are creditors, to the extent permitted by law, in satisfaction of liabilities of the limited partnership other than liabilities for distributions to partners under section 34-20d or 34-27d;

Removing a partner from a general partnership is the act of removing someone from your business that operates as a partnership. It can happen in several different ways, but the most common option is through a clause in the partnership agreement itself.

If a company goes into liquidation, all of its assets are distributed to its creditors. Secured creditors are first in line. Next are unsecured creditors, including employees who are owed money. Stockholders are paid last.

On dissolution of firm, when assets are distributed, liabilities are disposed in a proper order wherein payment to third party debt is on priority, followed by amount due to partners and in the end the residual amount is divided amongst the partners in profit sharing ratio.

Death of the partner If there are only two partners, and one of the partner dies, the partnership firm will automatically dissolve. If there are more than two partners, other partners may continue to run the firm.

Death of the partner If there are only two partners, and one of the partner dies, the partnership firm will automatically dissolve. If there are more than two partners, other partners may continue to run the firm.

On the death of a partner, subject to any contract to the contrary, the partnership ceases to exist. Here, the contract on the contrary means the partnership need not be dissolved if it is expressly mentioned in the partnership deed that the remaining partners (not a partner) can continue the firm's business.

The death of a partner or the unauthorized transfer of ownership of his share in the partnership in case there is a limitation to this effect results in the dissolution thereof. In other words, any change in the composition of the partnership, unless so allowed, will result in the dissolution thereof.

Upon the winding up of a limited partnership, the assets shall be distributed as follows: (1) To creditors, including partners who are creditors, to the extent permitted by law, in satisfaction of liabilities of the limited partnership other than liabilities for distributions to partners under section 34-20d or 34-27d;