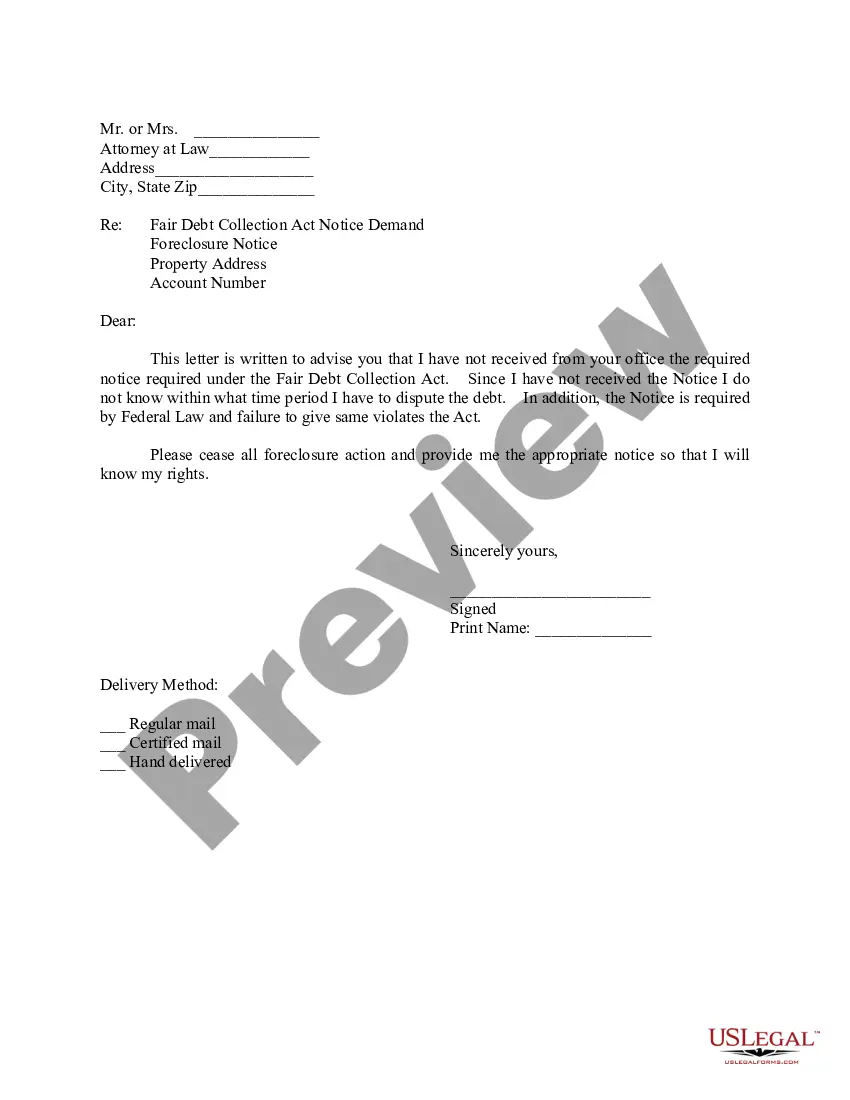

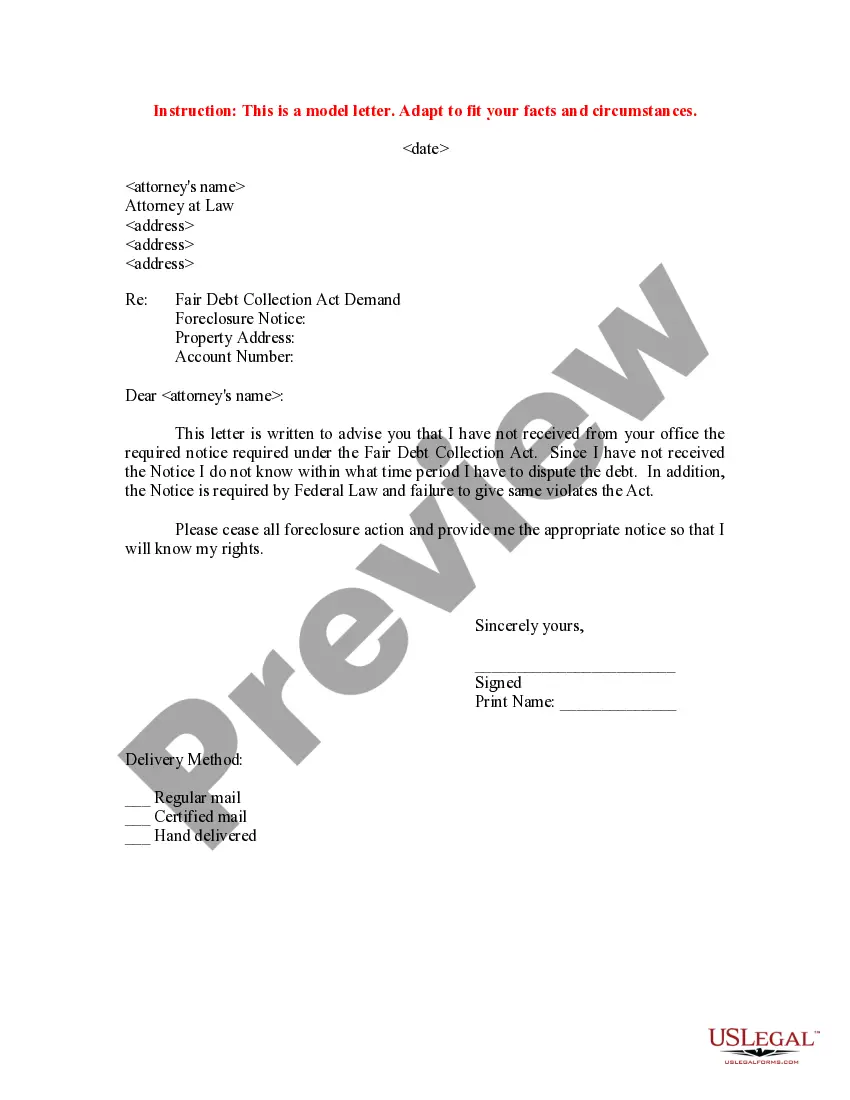

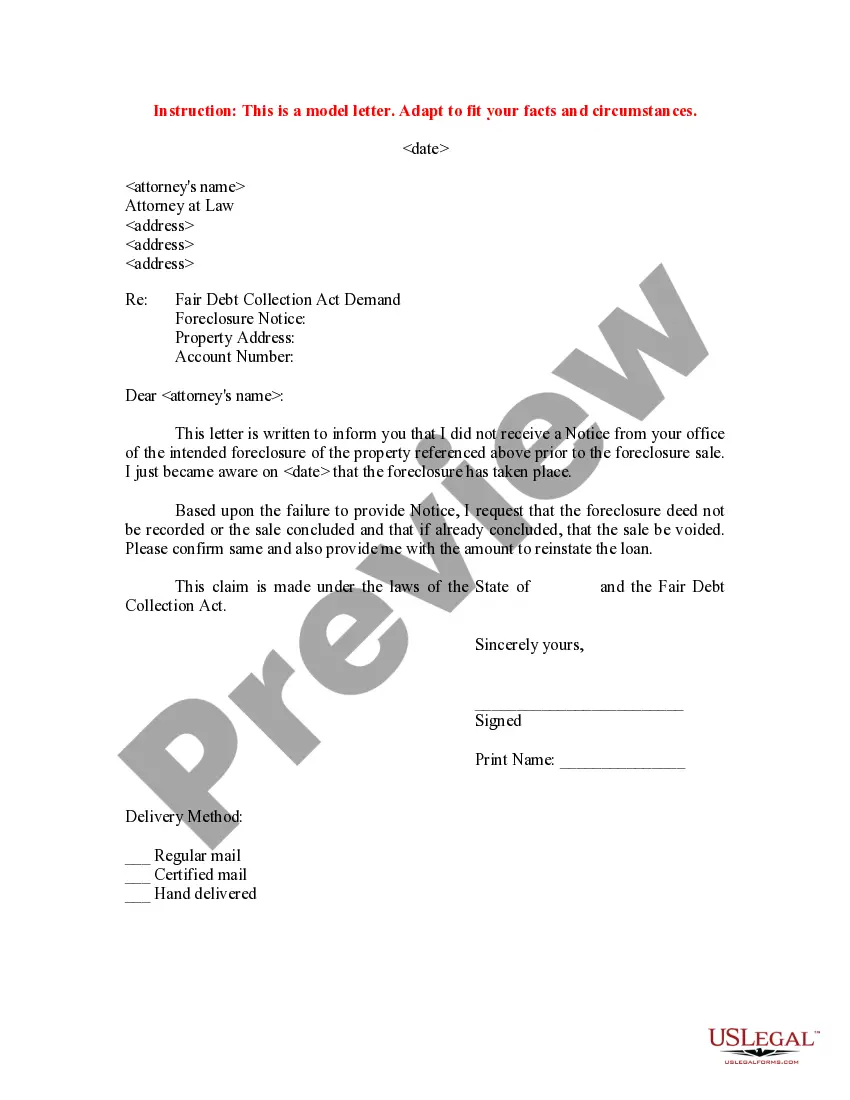

Petitioner states that he/she did not receive a Notice of Intended Foreclosure prior to the foreclosure sale. Petitioner also requests that the foreclosure deed not be recorded or the sale concluded based on a failure to provide adequate notice.

Indiana Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice of

Instant download

Description

How to fill out Letter To Foreclosure Attorney - After Foreclosure - Did Not Receive Notice Of?

Choosing the best lawful record web template might be a battle. Obviously, there are a variety of web templates available online, but how can you find the lawful type you need? Take advantage of the US Legal Forms website. The support offers 1000s of web templates, for example the Indiana Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice of, that you can use for organization and private demands. Each of the kinds are checked out by professionals and satisfy federal and state specifications.

When you are already registered, log in for your bank account and click the Download option to obtain the Indiana Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice of. Make use of bank account to look throughout the lawful kinds you might have ordered formerly. Visit the My Forms tab of the bank account and get an additional backup of the record you need.

When you are a whole new user of US Legal Forms, listed here are easy guidelines for you to adhere to:

- Initial, be sure you have chosen the proper type for your personal area/state. You may check out the shape using the Review option and read the shape explanation to make sure it will be the right one for you.

- In the event the type will not satisfy your requirements, utilize the Seach field to get the proper type.

- When you are certain the shape is suitable, click the Purchase now option to obtain the type.

- Select the prices program you want and enter in the essential information and facts. Make your bank account and buy your order with your PayPal bank account or credit card.

- Opt for the data file format and obtain the lawful record web template for your gadget.

- Comprehensive, change and produce and indicator the attained Indiana Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice of.

US Legal Forms may be the biggest library of lawful kinds where you can see numerous record web templates. Take advantage of the service to obtain professionally-produced files that adhere to condition specifications.

Form popularity

FAQ

How Do I Get Out of Foreclosure in Indiana? A few potential ways to stop a foreclosure include reinstating the loan, redeeming the property before the sale, or filing for bankruptcy. Of course, if you're able to work out a loss mitigation option, like a loan modification, that will also stop a foreclosure.

In Indiana, the statute of limitations on a mortgage foreclosure is ten (10) years from the last installment of the debt becoming due, as indicated by the record of the lien. This means that if the debt has not been paid within ten years, the lender can no longer pursue foreclosure.

Notice of Default ? Foreclosure starts when your lender records a Notice of Default against your property with the Registrar Recorder's office. The Notice of Default tells you the total amount you owe including missed payments and foreclosure fees.

Indiana Does Not Have a Post Sale Redemption Period To be clear, redeeming the property means paying to bring any loan payments and late fees owed up to date, and then you will have to continue to make your regular loan payments.

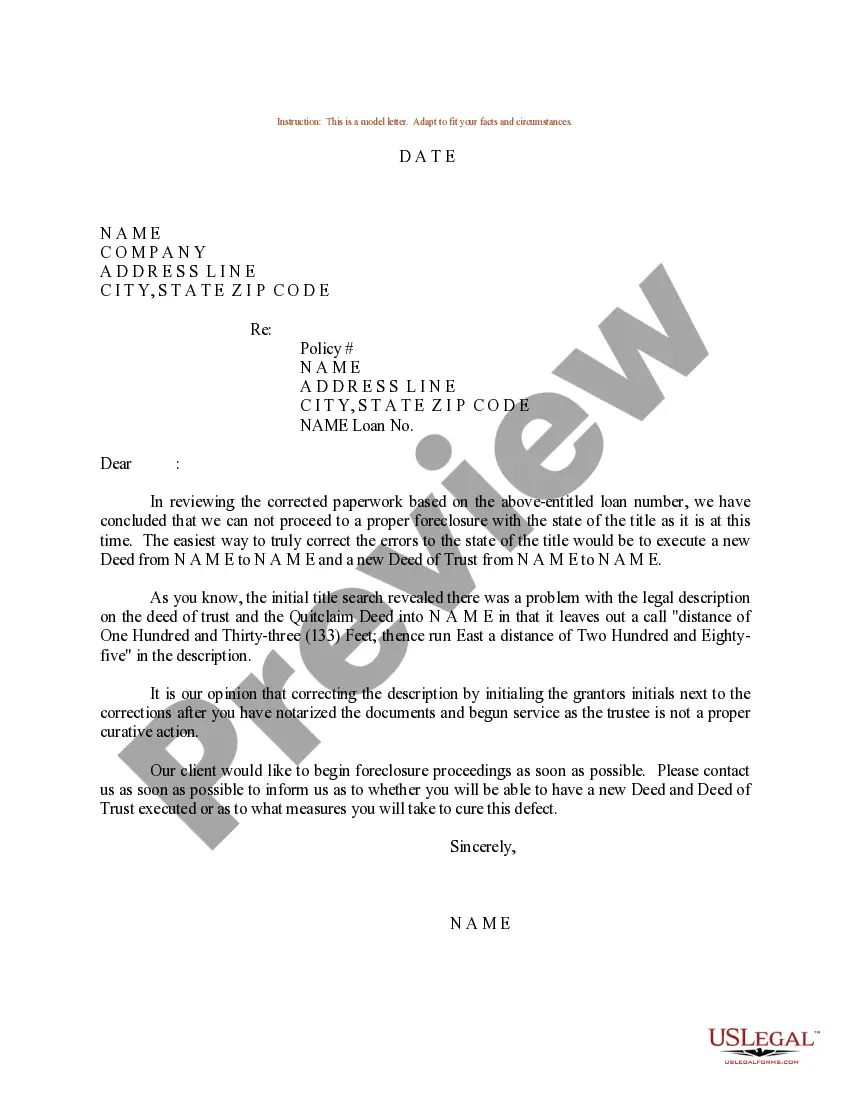

In the context of mortgage foreclosure, a notice of default is a formal notice that a lender filed with courts to notify the borrower who has failed to make payments that the lender intends to conduct a sale foreclosure.

Technically speaking, a notice of default is not a foreclosure. Instead, it serves as notice that you are behind in your payments and that your property may be sold as a result of foreclosure if you don't act soon.

A Notice of Default is filed when the debtor has defaulted on the terms of a previously-filed agreed entry and the filing party wishes the court to take action such as granting relief from stay. The court may decide to set the matter for hearing or the order may be granted without hearing.

Indiana foreclosures have four basic parts. The (1) initial ?behind-in-payments? period, (2) the foreclosure lawsuit, (3) the foreclosure judgment, and (4) the sheriff's sale. This entire process from start to finish usually takes about 8-10 months in Indiana.