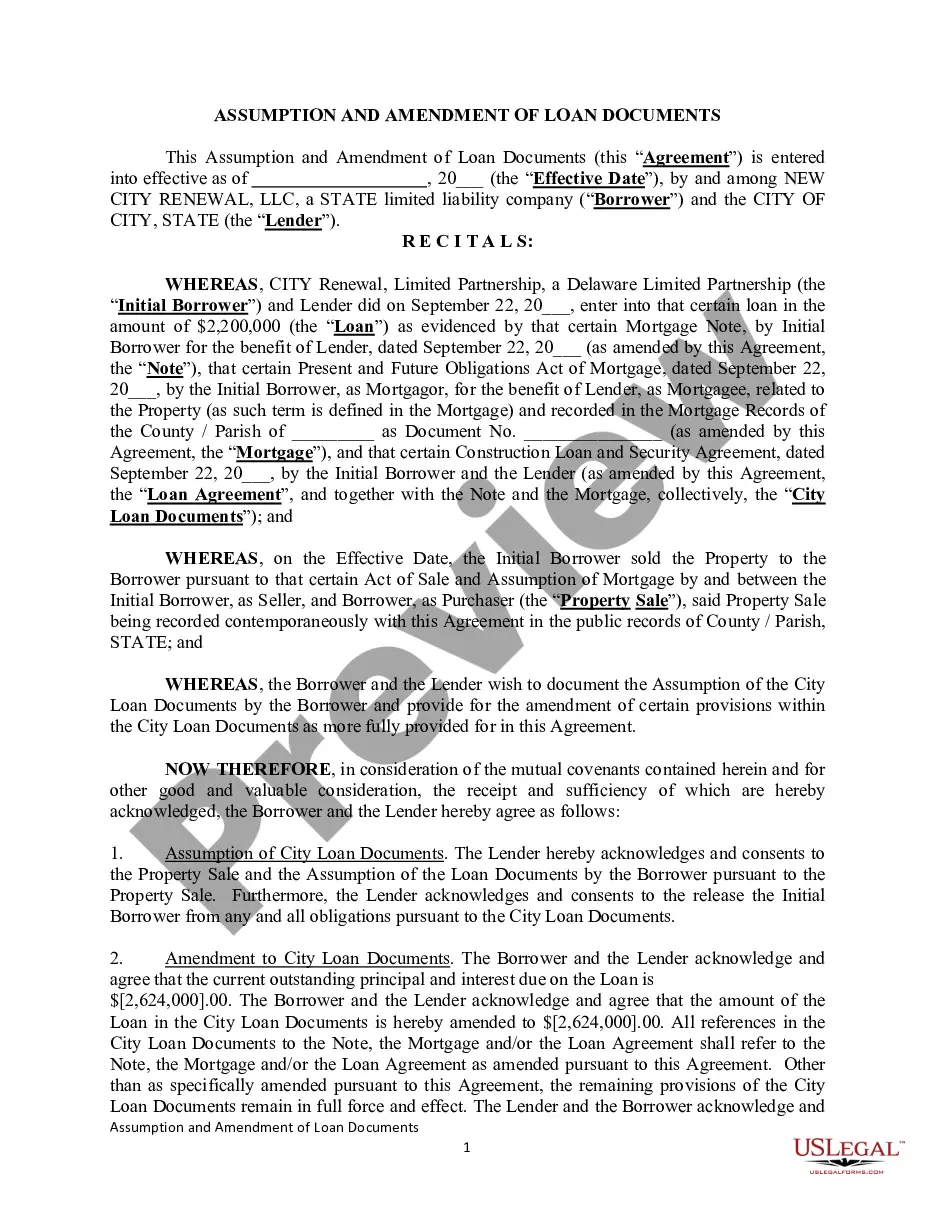

This form is an Assumption Agreement. The form provides that the grantee will assume a lien on property described in the agreement. The assumption will become effective on the date provided in the agreement.

Indiana Assumption Agreement of Loan Payments

Category:

State:

Multi-State

Control #:

US-00424

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Assumption Agreement Of Loan Payments?

Locating the appropriate sanctioned document template can be rather challenging. Clearly, there are numerous designs accessible online, but how do you find the official form you need? Utilize the US Legal Forms website. The platform offers thousands of templates, including the Indiana Assumption Agreement of Loan Payments, which can be utilized for business and personal purposes. All of the documents are reviewed by experts and comply with state and federal regulations.

If you are already registered, sign in to your account and then click the Download button to locate the Indiana Assumption Agreement of Loan Payments. Use your account to review the legal forms you have previously acquired. Navigate to the My documents section of your account and download another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions that you can follow: First, ensure you have chosen the correct form for your city/state. You can browse the template using the Preview button and read the form description to confirm it is the right one for you. If the form does not meet your requirements, use the Search field to find the appropriate form. Once you are confident that the template is correct, click on the Get now button to obtain the form. Select the pricing plan you desire and enter the necessary information. Create your account and complete the transaction using your PayPal account or credit card. Choose the file format and download the legal document template to your device. Complete, edit, print, and sign the downloaded Indiana Assumption Agreement of Loan Payments.

Utilize this service to obtain well-structured papers that comply with state requirements.

- US Legal Forms is the largest repository of legal forms.

- Easily find numerous document templates.

- Access professionally crafted documents that adhere to state regulations.

- Eliminate the hassle of searching through unverified sources.

- Ensure compliance with legal standards with every document.

- Streamline your legal document needs efficiently.

Form popularity

FAQ

A loan assumption agreement is a legal document that allows a buyer to take over the payments of an existing loan from the seller. In the context of an Indiana Assumption Agreement of Loan Payments, this process can simplify the transfer of property ownership while maintaining the original loan terms. It ensures that the buyer assumes responsibility for the debt, which can be beneficial for both parties involved. Utilizing platforms like US Legal Forms can help you easily create and customize this agreement to meet your specific needs.

Documenting a loan assumption involves creating a formal Indiana Assumption Agreement of Loan Payments. This agreement outlines the terms of the assumption, including responsibilities and obligations of both parties. It is crucial to have the agreement signed by the lender, the original borrower, and the new borrower. Utilizing platforms like USLegalForms can simplify this documentation process, providing templates and guidance to help you navigate the legal requirements.

To successfully execute an Indiana Assumption Agreement of Loan Payments, specific requirements must be met. Generally, the current borrower must be in good standing, and the lender must approve the assumption. Additionally, the new borrower typically needs to demonstrate creditworthiness and financial stability. Ensuring you meet these requirements can facilitate a more efficient loan assumption process.

When you pursue an Indiana Assumption Agreement of Loan Payments, you typically need several key documents. These often include the original loan agreement, a written request for assumption, and the borrower's financial information. Depending on the lender, you may also need to provide proof of income and credit history. Gathering these documents ensures a smooth transition during the assumption process.

An assumption agreement, sometimes called an assignment and assumption agreement, is a legal document that allows one party to transfer rights and/or obligations to another party. It allows one party to "assume" the rights and responsibilities of the other party.

Assumption of Obligations. New Borrower covenants, promises, and agrees that New Borrower, jointly and severally if more than one, will unconditionally assume and be bound by all terms, provisions, and covenants of the Assumed Loan Documents as if New Borrower had been the original maker of the Assumed Loan Documents.

An assumable mortgage is a home loan that can be transferred from the original borrower to the next homeowner. The interest rate and payment period stay the same. For example, if a 30-year mortgage is three years old, the person assuming the loan has 27 years to pay it off.

Loan assumption, however, allows a buyer to take over the current owner's mortgage while the loan's terms ? including the repayment period and interest rate ? remain the same. Ultimately, it can help people get into a home at a lower interest rate even as the housing market around them becomes more expensive.

If the mortgage loan is assumable, a seller can sell their home to a qualified buyer, allowing the buyer to purchase the home by way of assuming responsibility for the seller's loan terms and remaining balance.