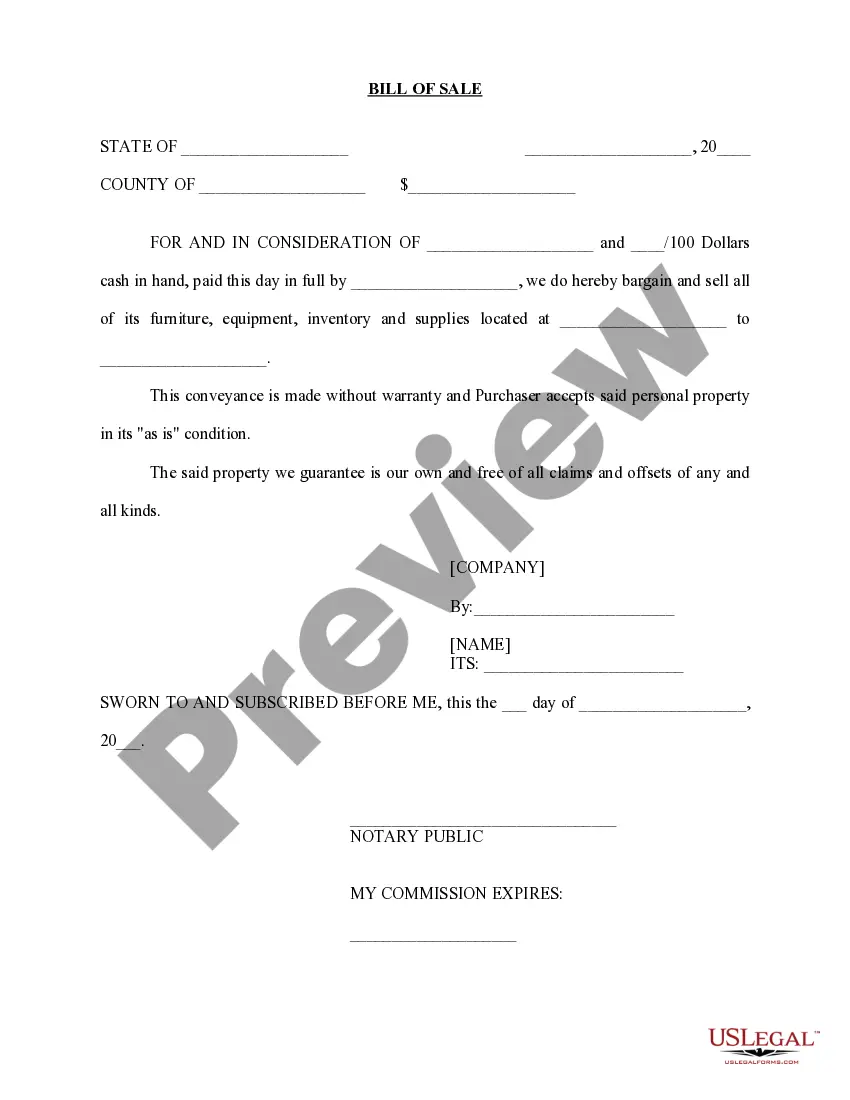

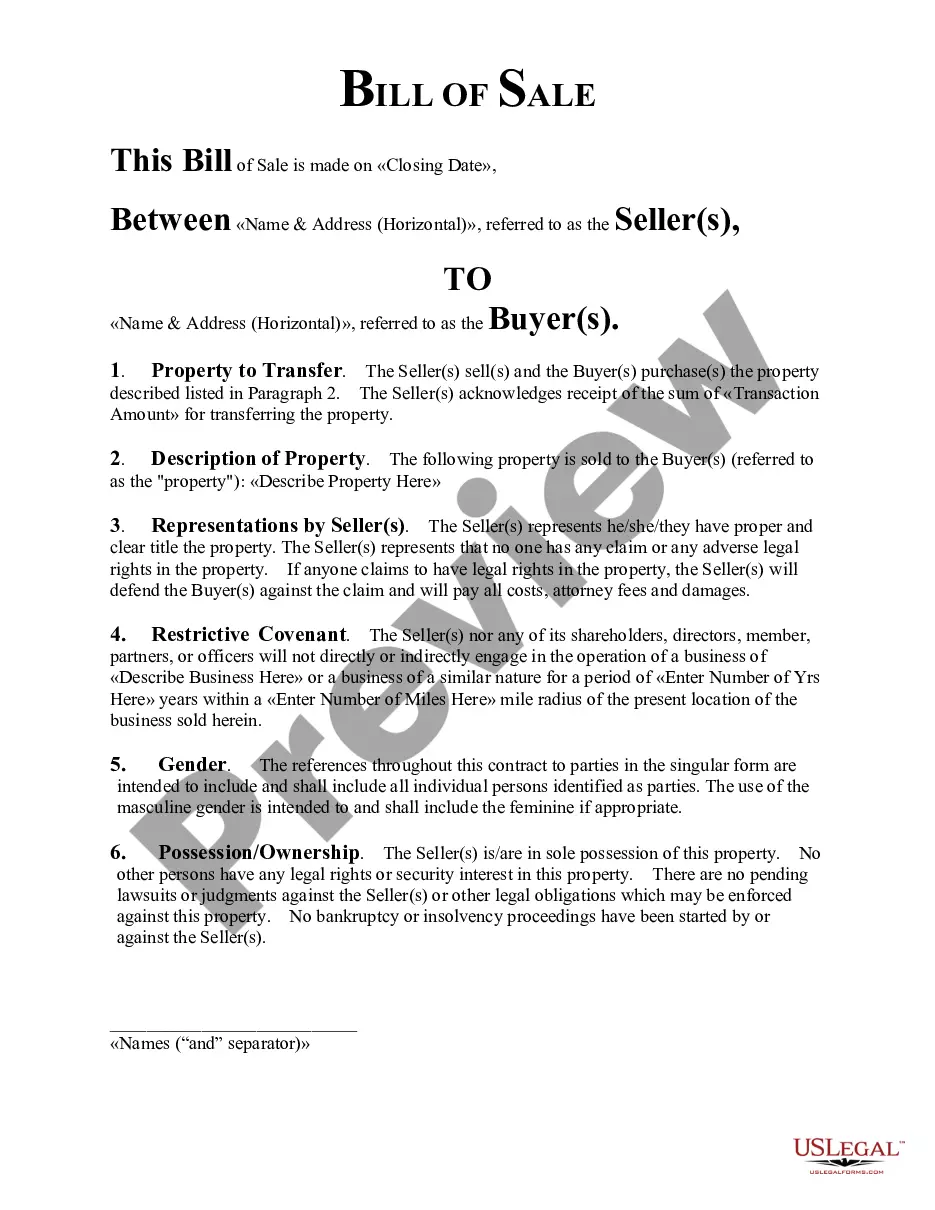

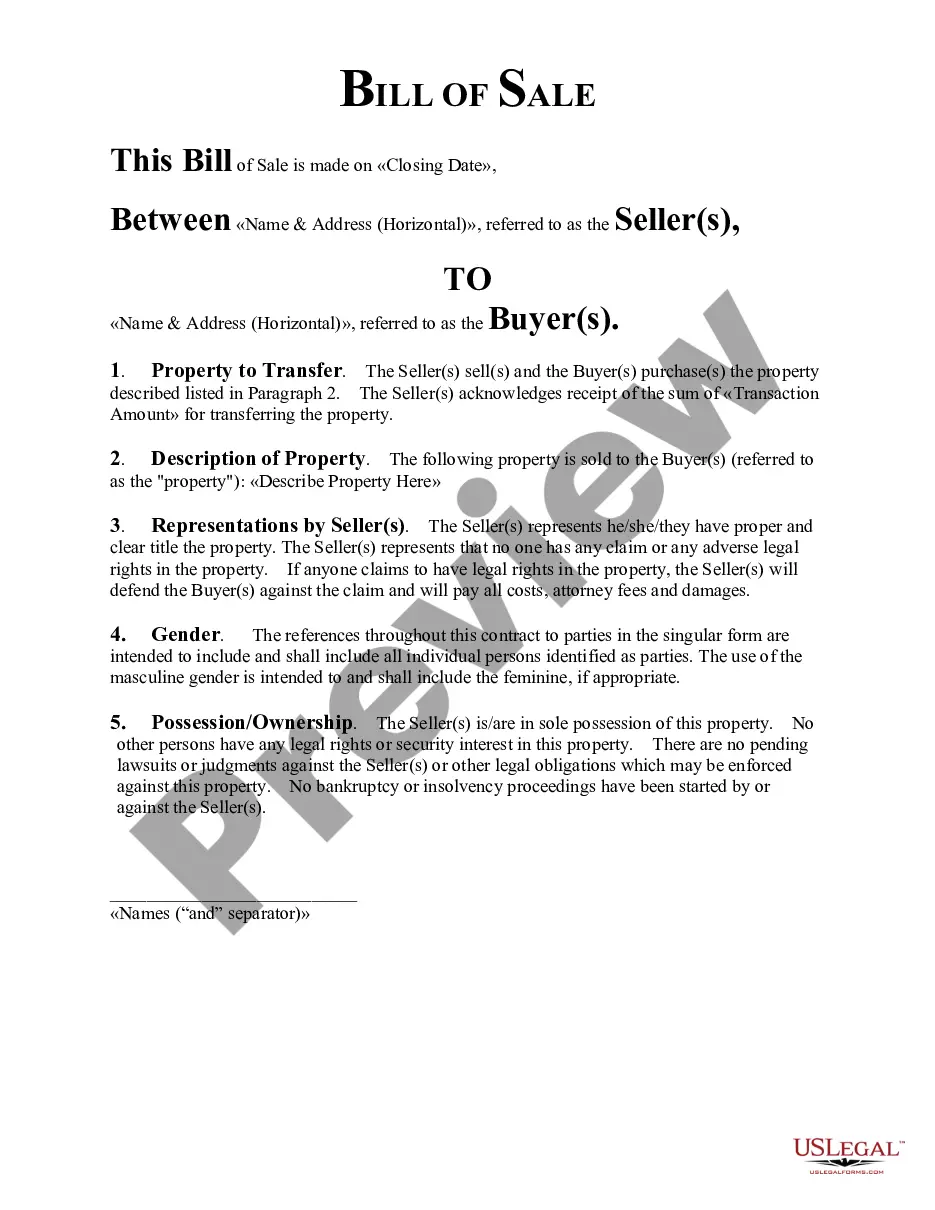

This form is a detailed Bill of Sale. It is to be used when an individual and/or a corporation wishes to sell their business in the State of Indiana.

Indiana Bill of Sale in Connection with Sale of Business by Individual or Corporate Seller

Instant download

Description

Free preview

How to fill out Indiana Bill Of Sale In Connection With Sale Of Business By Individual Or Corporate Seller?

Locating Indiana Bill of Sale related to the Sale of Business by Individual or Corporate Seller forms and completing them can be difficult.

To conserve time, expenses, and effort, utilize US Legal Forms and discover the appropriate template specifically for your state with just a few clicks.

Our attorneys prepare each document, so all you need to do is fill them out. It’s really that easy.

Select your payment method on the pricing page and create your account. Choose whether you wish to pay by card or via PayPal. Save the form in your desired format. You can either print the Indiana Bill of Sale related to the Sale of Business by Individual or Corporate Seller template or complete it using any online editor. Don’t worry about typos as your sample can be used, submitted, and printed repeatedly. Explore US Legal Forms and gain access to over 85,000 state-specific legal and tax documents.

- Log into your account and return to the form's page to download the sample.

- Your downloaded samples are saved in My documents and are readily available anytime for future use.

- If you haven’t signed up yet, you will need to register.

- Review our detailed instructions on how to obtain your Indiana Bill of Sale for Sale of Business by Individual or Corporate Seller form within minutes.

- To obtain an accurate form, verify its validity for your state.

- Examine the sample using the Preview option (if available).

- If there’s a description, review it to understand the key elements.

- Hit Buy Now if you found what you were looking for.

Form popularity

FAQ

You should not sign anything before you get your money. If the buyer says the buyer would be back later with your money and you sign the title over to the buyer, you likely will never see your money...

Both the buyer and seller should receive copies of the bill of sale form. It's important for the buyer to keep the bill of sale with the title of the vehicle for registration and licensing purposes, if necessary. However, all parties should keep them for their own personal records.

For example, many states require that a vehicle bill of sale include an odometer reading; some states require it to be notarized. Both parties can sign a bill of sale but, in many instances, only the seller needs to sign it. Things can get complicated when a bill of sale is provided as security for a loan.

A Bill of Sale is a legal document that provides proof of ownership.According Indiana laws, you as the seller must provide the document while selling your car. You will also need to fill in the information of the bill of sale in the Form 44237.

In simple terms, a bill of sale agreement is nothing more than a contract for the purchase of a vehicle between a buyer and a seller.In most cases, the contract is legally binding between buyer and seller as long as the bill of sale follows guidelines required in the state where the sale or transfer takes place.

Generally, a bill of sale does not have to be recorded but may be required as proof of ownership. Who must sign a bill of sale? The owners of the property being sold must sign. If the property is owned jointly, both owners must generally sign.

The bill of sale, as a rule, is drafted by the seller and includes the details of the transaction. It protects both the buyer and the seller, should disagreements arise in the future.

A bill of sale is a legal document that records the transfer of ownership of an asset to a second party in exchange for money.It protects both the buyer and the seller, should disagreements arise in the future.

If there are 2 owners listed on the front of a title, the majority of the time, both people will need to sign as the seller. If there is an 'or' in between the names, typically only 1 signature is required.