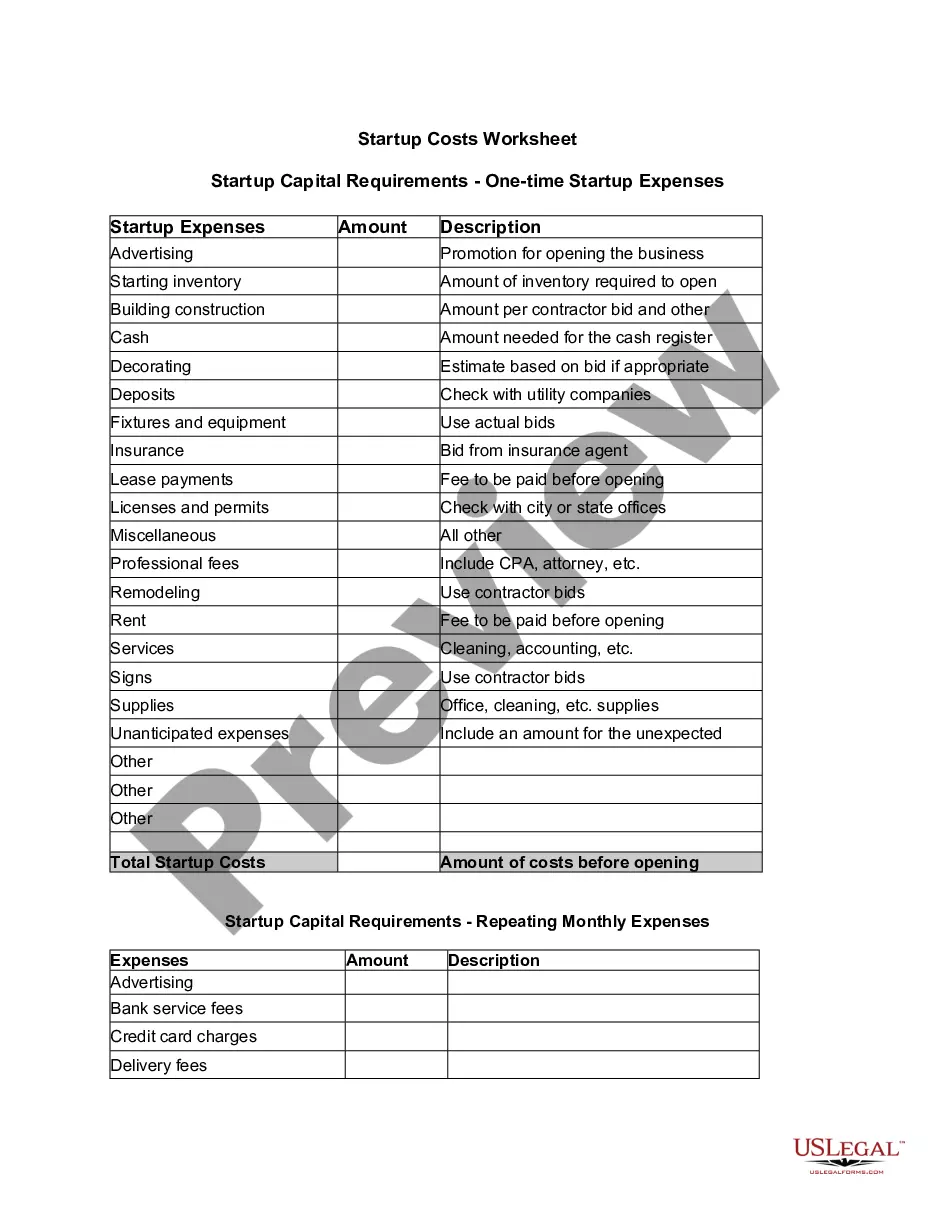

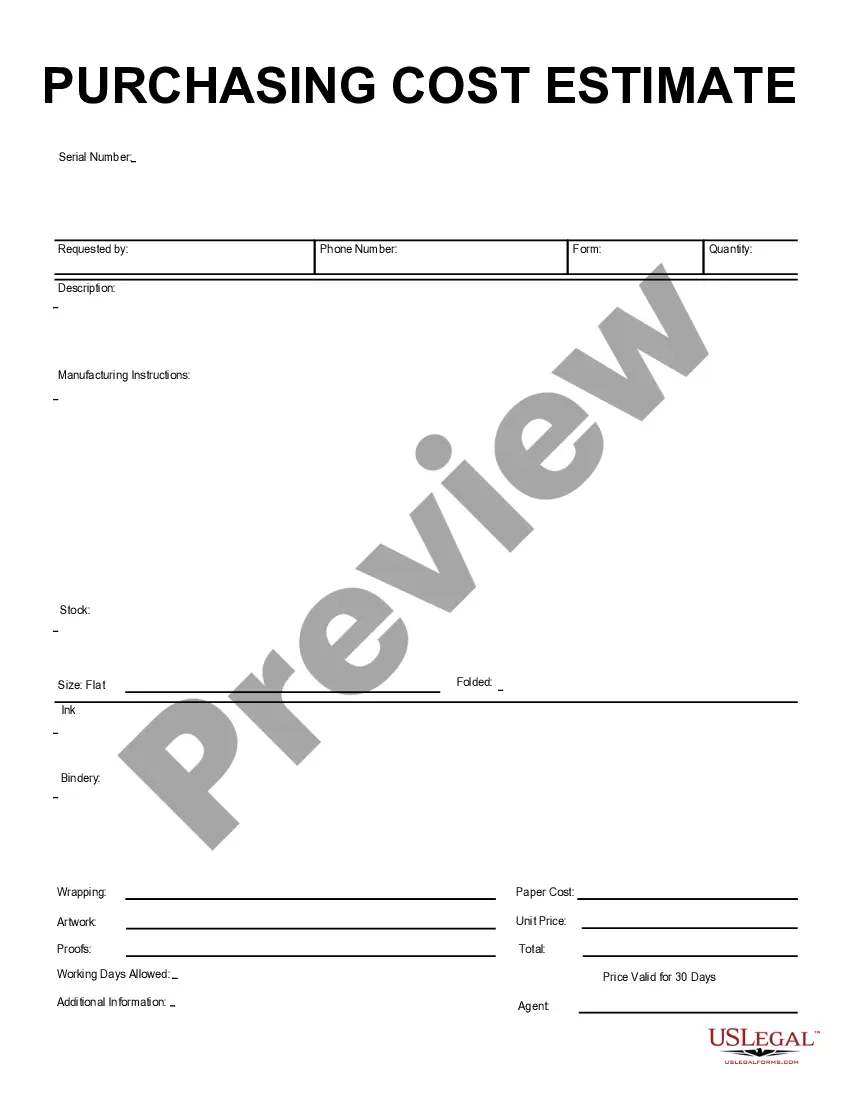

Illinois Price Setting Worksheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Price Setting Worksheet?

Selecting the finest authentic document template can be a challenge.

Certainly, there are numerous templates accessible online, but how do you locate the authentic version you require.

Utilize the US Legal Forms website.

First, ensure that you have selected the correct form for your area/region.

- The service offers thousands of templates, including the Illinois Pricing Worksheet, which you can use for business and personal purposes.

- All templates are verified by professionals and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Download button to obtain the Illinois Pricing Worksheet.

- Use your account to review the legal documents you have obtained previously.

- Visit the My documents section of your account to download another copy of the document you need.

- If you're a new user of US Legal Forms, here are simple steps for you to follow.

Form popularity

FAQ

Schedule IL-WIT, Illinois Income Tax Withheld, allows you to enter your withholding information in one place and calculate total Illinois withholding.

All trade or businesses, except those that derive more than 50% of their gross receipts from qualified business activities (QBA), must apportion their business income to California using a single-sales factor.

The Illinois Use Tax rate is 6.25 percent of the selling price of purchases of general merchandise, including automobiles and other items that must be titled or registered.

In Illinois (see IITA Section 304), this apportionment of business income is accomplished by multiplying the corporation's income by a percentage that is derived from comparing its sales in Illinois to its total sales.

Your Illinois income includes the adjusted gross income (AGI) amount figured on your federal return, plus any additional income that must be added to your AGI. Some of your income may be subtracted when figuring your Illinois base income.

The Illinois Use Tax rate is 6.25 percent of the selling price of purchases of general merchandise, including automobiles and other items that must be titled or registered. The use tax rate is 1 percent on purchases of qualifying food, drugs, and medical appliances.

The apportionment percentage is determined by adding the taxpayer's receipts factor (as described in Section 3 of this article), property factor (as described in Section 4 of this article), and payroll factor (as described in Section 5 of this article) together and dividing the sum by three.

Apportionment is the assignment of a portion of a corporation's income to a particular state for the purposes of determining the corporation's income tax in that state. The state determines how much of your earnings are a result of business done in that state so it can charge you the right amount of income tax.

Illinois Use Tax rates are 6.25 percent of the purchase price of general merchandise and 1.00 percent of the purchase price of qualifying food, drugs, and medical appliances.

Illinois has a statewide sales tax rate of 6.25%, which has been in place since 1933. Municipal governments in Illinois are also allowed to collect a local-option sales tax that ranges from 0% to 5.25% across the state, with an average local tax of 1.904% (for a total of 8.154% when combined with the state sales tax).