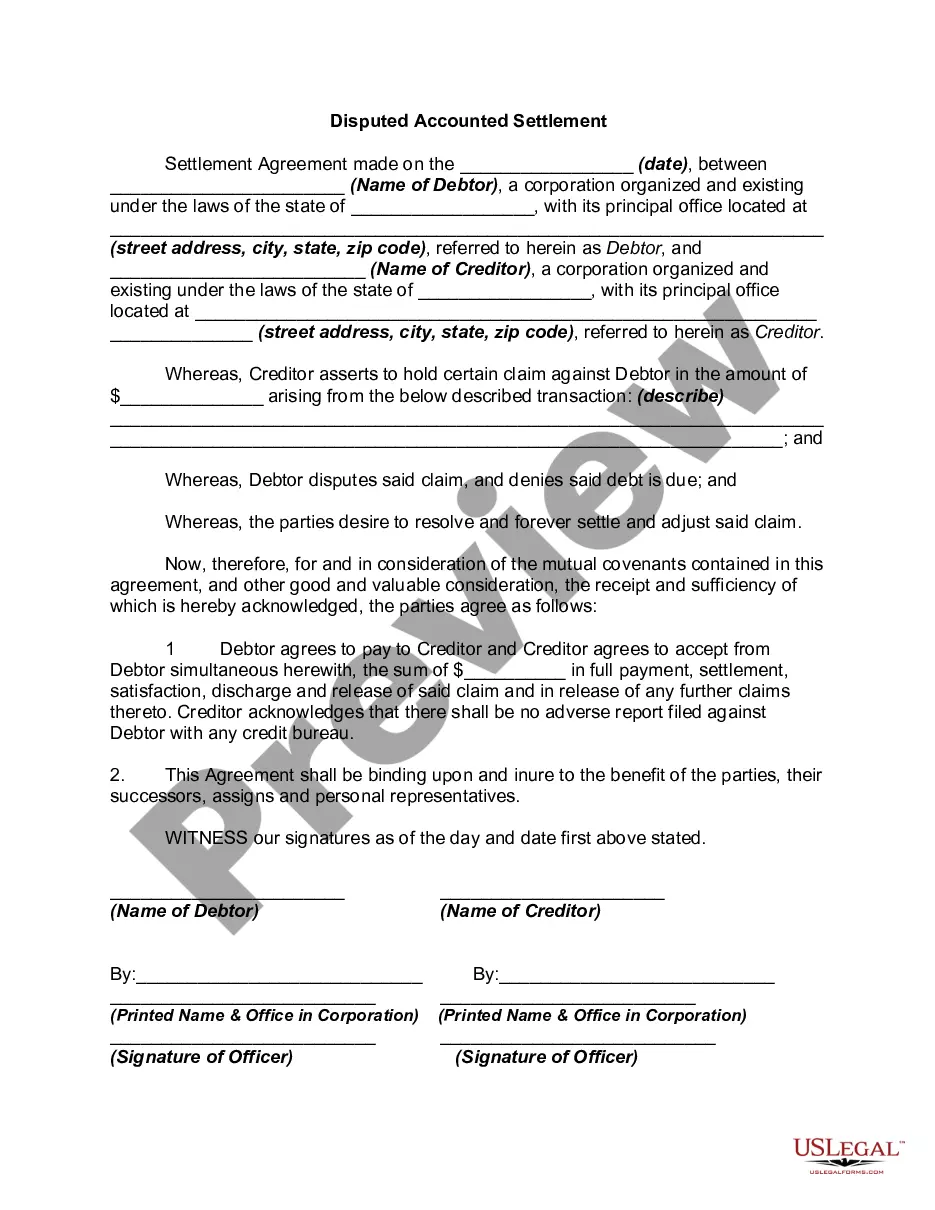

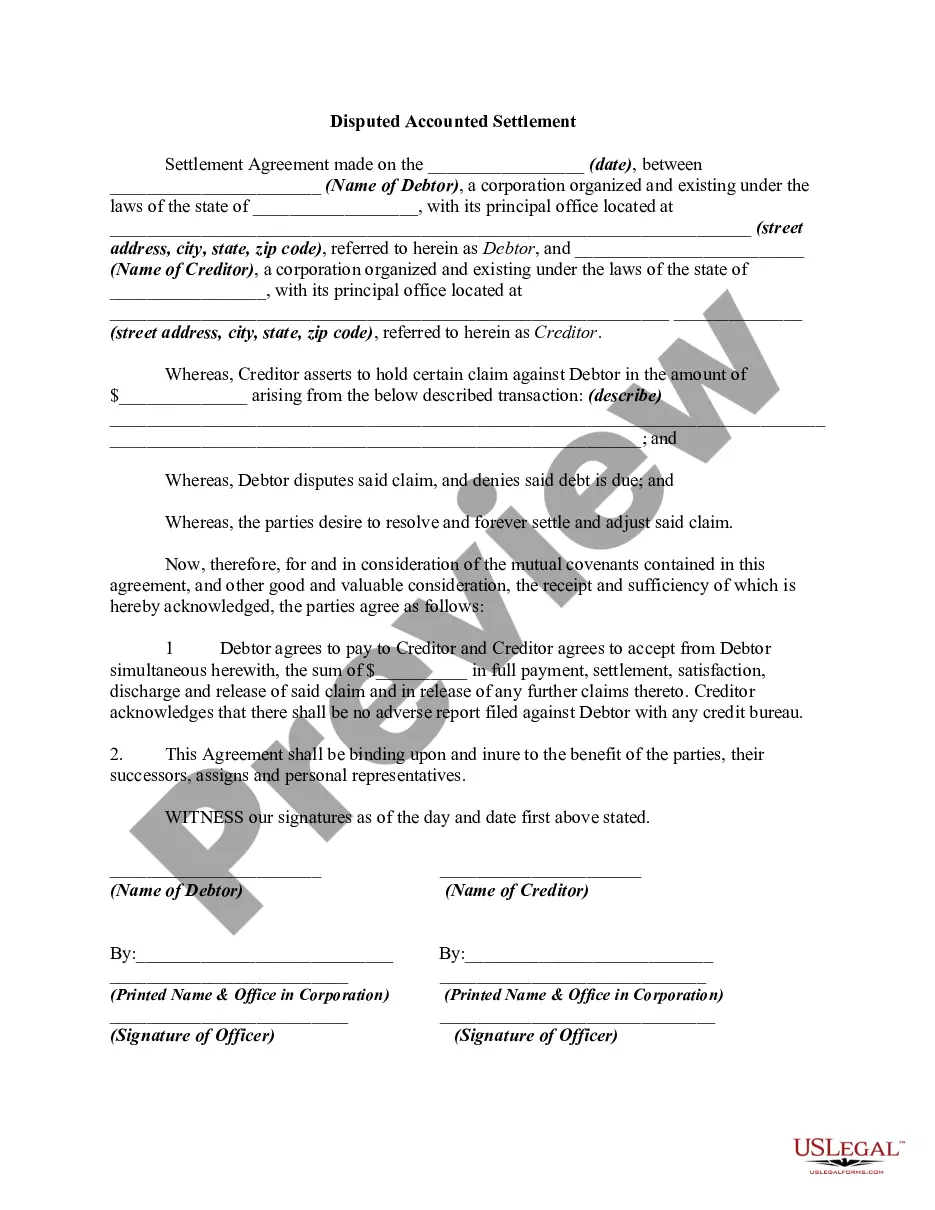

Illinois Disputed Open Account Settlement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Disputed Open Account Settlement?

Finding the appropriate legitimate document format can be a challenge.

Certainly, there are numerous templates accessible online, but how can you locate the correct one you need.

Utilize the US Legal Forms website. This service provides thousands of templates, including the Illinois Disputed Open Account Settlement, which can be utilized for both business and personal purposes.

You can preview the form using the Preview button and review the form details to confirm it is the right one for you.

- All of the forms are reviewed by professionals and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Obtain button to locate the Illinois Disputed Open Account Settlement.

- Use your account to search for the legal forms you have previously ordered.

- Visit the My documents section of your account to retrieve another copy of the document you require.

- If you are a new user of US Legal Forms, here are simple steps to follow.

- First, ensure you have selected the correct form for your city/state.

Form popularity

FAQ

If old debt has not fallen off your credit report after seven years, contact the three major credit bureaus (Equifax, Experian and TransUnion) and request that they remove the delinquent debt from your credit report. You may also have a delinquent debt on your credit report that is not actually yours.

Both the credit bureau and the business that supplied the information to a credit bureau have to correct information that's wrong or incomplete in your report. And they have to do it for free. To correct mistakes in your report, contact the credit bureau and the business that reported the inaccurate information.

If the company finds they erroneously reported the late payment, they can contact the credit bureaus to remove the incorrect information. You can submit a dispute with the three major credit reporting agencies?Experian, Equifax and TransUnion?online, by phone or by mail.

Here are two of your most viable options to remove late payments from your credit report: Call Your Credit Card Issuer and Ask Them to Take the Late Payments Off Your Credit Report. ... Write a Goodwill Letter to the Creditor Explaining Why You Haven't Made Timely Payments.

Under section 609, you have the right to request: All of the information in your consumer credit files. The source of that information. Each entity that has accessed your credit report within the past two years (unless it was to complete an investigation) Businesses that have made soft inquiries within the past year.

Credit bureaus receive information from lenders and creditors, businesses, and government agencies.

Send a letter to the credit bureau. ... Determine if you should contact the furnisher as well. ... Wait up to 45 days for the credit bureau or furnisher to investigate and respond. ... Review the results of the investigation. ... Check for updates to your credit report.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.