Employer's form to determine between employee and 1099 contractor.

Idaho IRS 20 Quiz to Determine 1099 vs Employee Status

Instant download

Description

How to fill out IRS 20 Quiz To Determine 1099 Vs Employee Status?

Finding the right lawful file template might be a struggle. Needless to say, there are a variety of web templates accessible on the Internet, but how do you get the lawful type you need? Use the US Legal Forms site. The services offers a huge number of web templates, including the Idaho IRS 20 Quiz to Determine 1099 vs Employee Status, that can be used for organization and personal needs. All of the kinds are examined by professionals and meet federal and state needs.

Should you be already registered, log in to the bank account and then click the Download key to find the Idaho IRS 20 Quiz to Determine 1099 vs Employee Status. Utilize your bank account to search from the lawful kinds you might have purchased formerly. Go to the My Forms tab of your own bank account and acquire an additional version of your file you need.

Should you be a whole new customer of US Legal Forms, allow me to share basic directions that you can stick to:

- Initially, be sure you have chosen the right type for your town/area. It is possible to examine the shape while using Preview key and study the shape information to make certain this is basically the best for you.

- If the type is not going to meet your requirements, take advantage of the Seach industry to obtain the appropriate type.

- When you are sure that the shape would work, select the Purchase now key to find the type.

- Select the rates program you desire and enter the required information and facts. Make your bank account and buy the transaction using your PayPal bank account or credit card.

- Select the file file format and download the lawful file template to the product.

- Total, modify and print out and signal the acquired Idaho IRS 20 Quiz to Determine 1099 vs Employee Status.

US Legal Forms is the biggest local library of lawful kinds in which you can discover different file web templates. Use the service to download appropriately-manufactured documents that stick to status needs.

Form popularity

FAQ

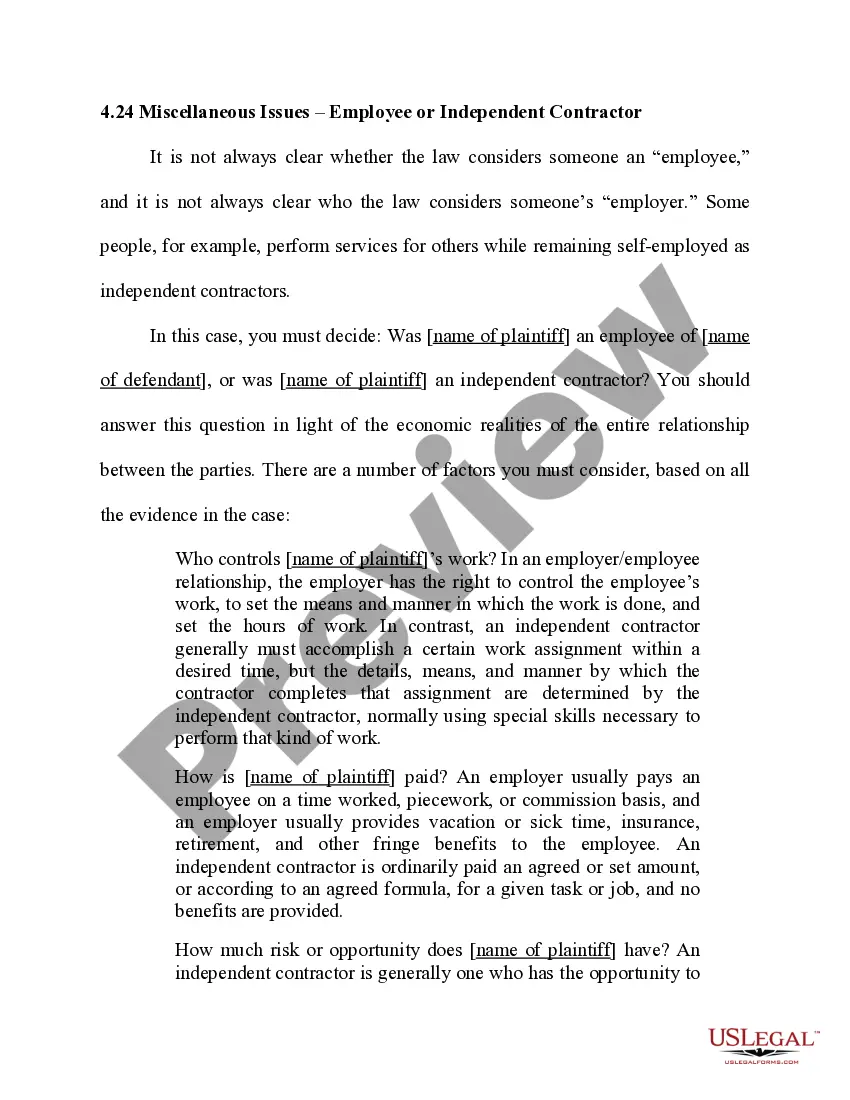

In Idaho, the difference between an employee and a contractor mainly lies in the nature of the working relationship. Employees usually work under direct supervision, receive benefits, and have taxes withheld, whereas contractors operate independently, often assigned specific tasks without ongoing control. The Idaho IRS 20 Quiz to Determine 1099 vs Employee Status explores these distinctions, ensuring you understand the implications. Familiarity with these definitions will empower you in making the right choices regarding employment classification.

Identifying whether someone is a W-2 employee or a 1099 independent contractor revolves around control, benefits, and tax responsibilities. A W-2 employee typically receives benefits and has taxes withheld from their paycheck, while a 1099 contractor is usually responsible for their own taxes, lacking additional benefits. The Idaho IRS 20 Quiz to Determine 1099 vs Employee Status can help clarify this distinction. Understanding these differences aids in proper classification.

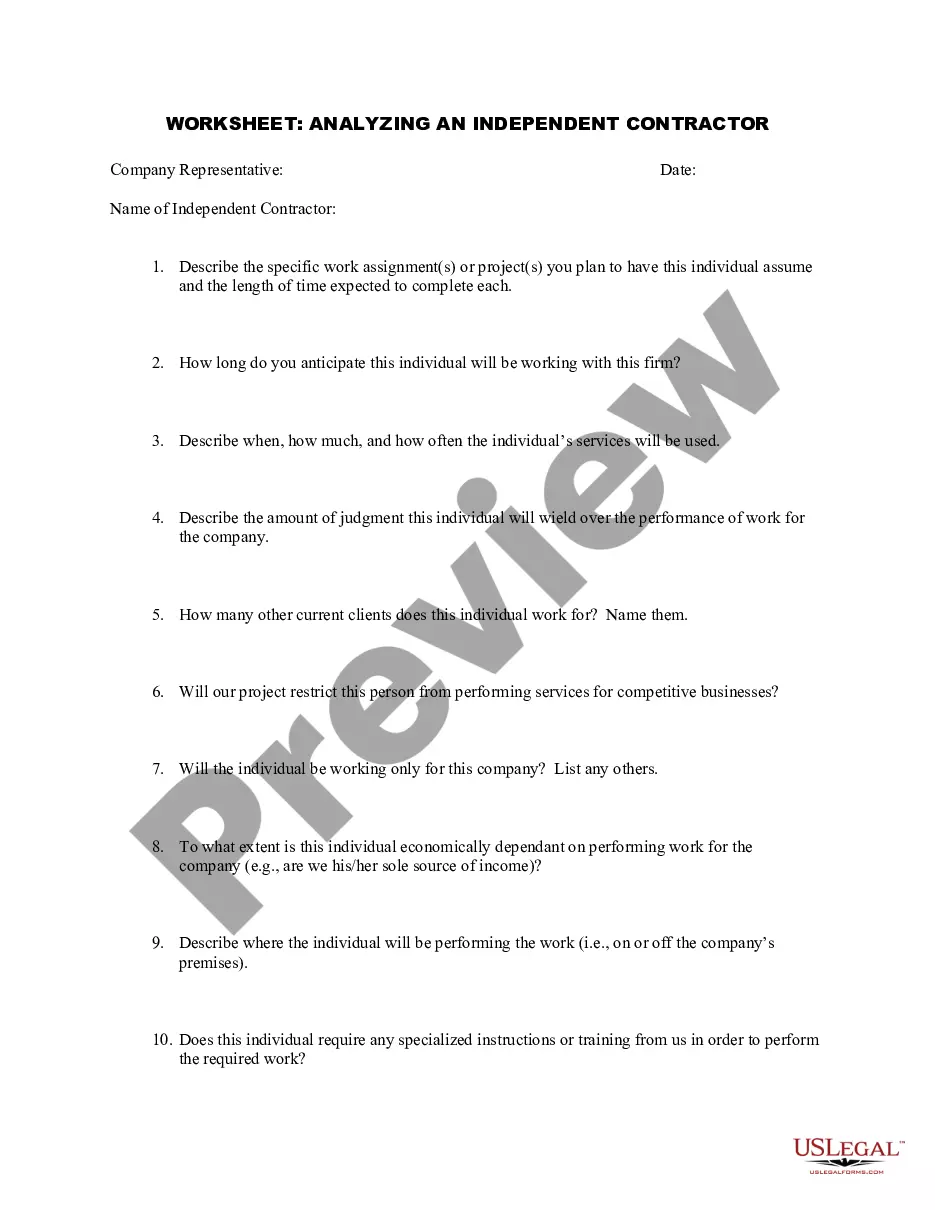

Several determining factors exist when classifying someone as an employee or an independent contractor. Primarily, the level of control exerted by the employer plays a significant role. In addition, the nature of the work relationship, including benefits and tax responsibilities, is also critical. Utilizing resources like the Idaho IRS 20 Quiz to Determine 1099 vs Employee Status can simplify this decision-making process.

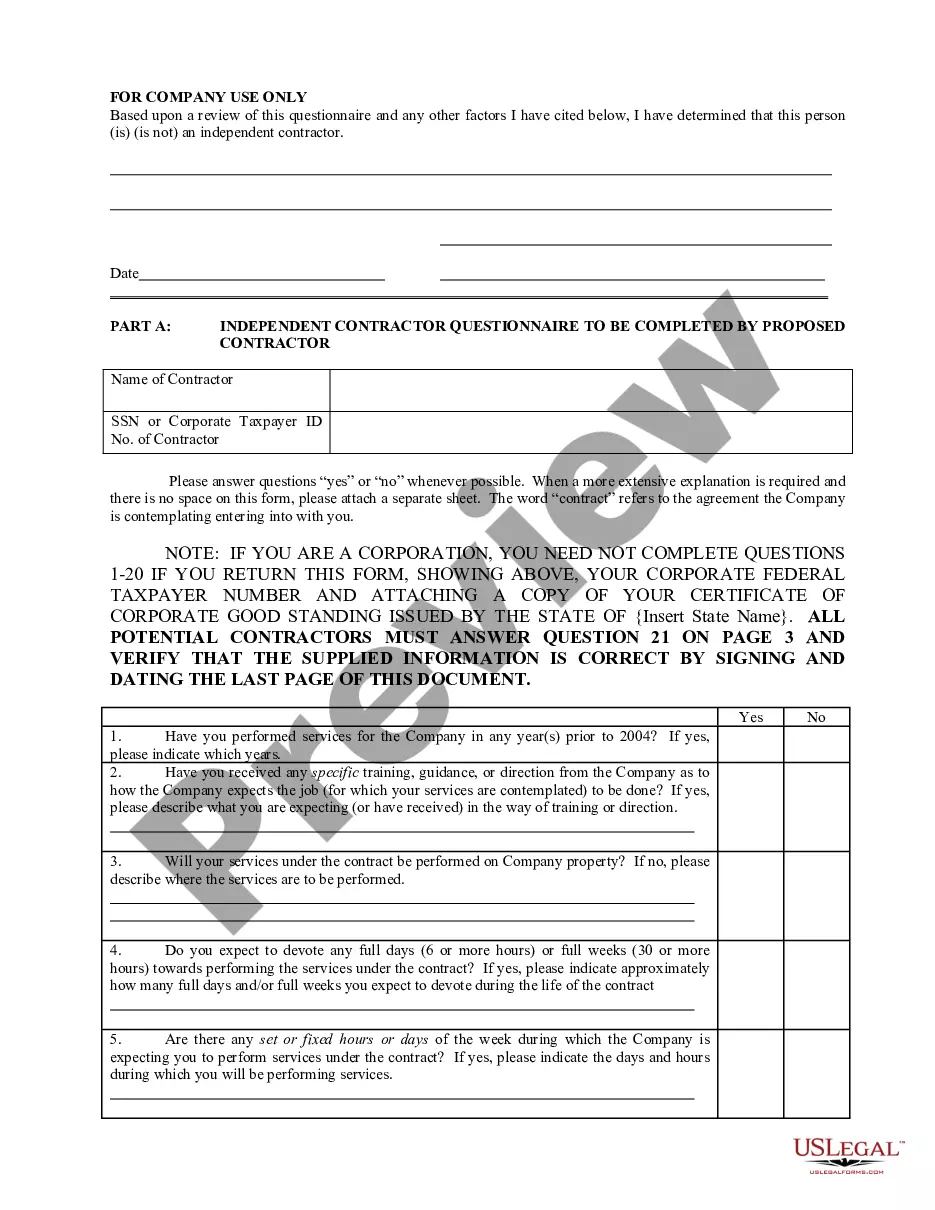

When assessing independent contractor status, ask questions that reveal control and independence. For instance, inquire about how the work is performed, who sets work hours, and whether the individual can work for other clients. The Idaho IRS 20 Quiz to Determine 1099 vs Employee Status can serve as a guide to understanding these key questions. Properly articulating these factors will bring clarity to your classification process.

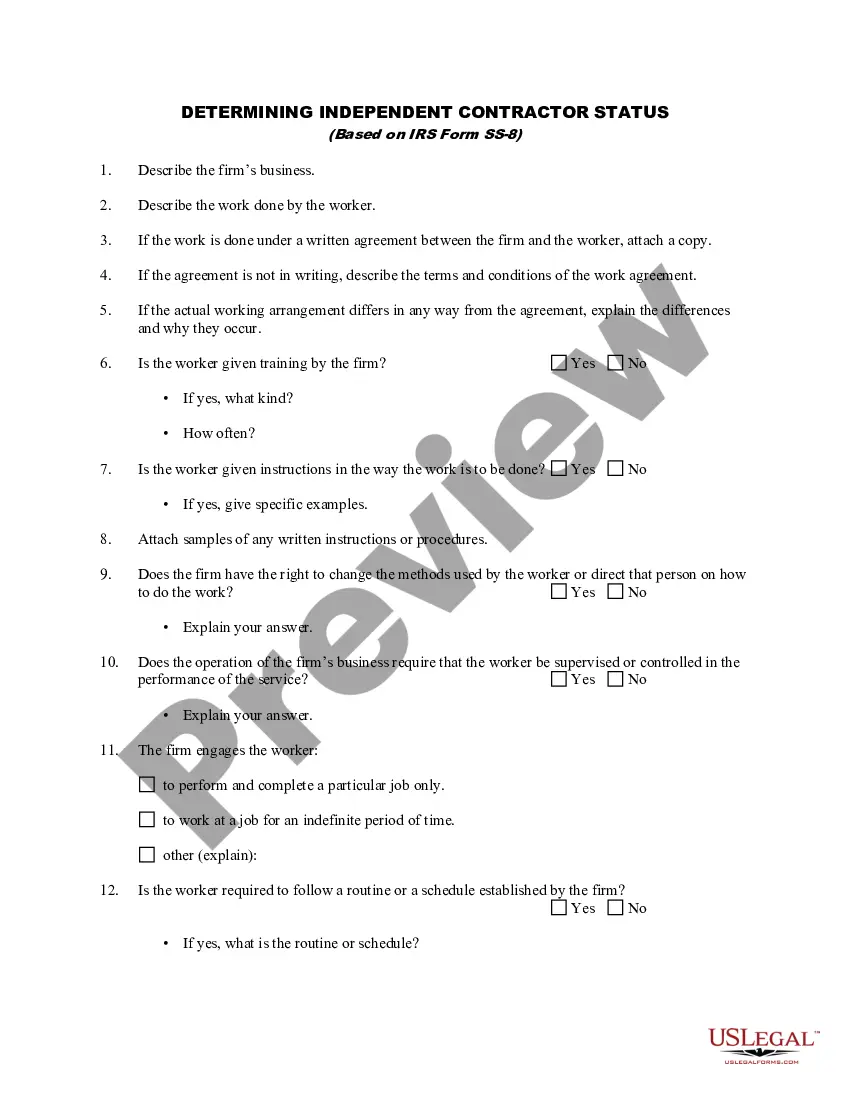

There are three primary tests that help determine employee status: the behavioral test, the financial test, and the relationship test. Each of these examines different aspects of the work arrangement and underscores the importance of stability and control. The Idaho IRS 20 Quiz to Determine 1099 vs Employee Status provides insights into these tests, clarifying what makes an employee distinct from a contractor. Knowing these tests is essential for accurate classification.

The IRS utilizes several criteria to distinguish an independent contractor from an employee, focusing mainly on the degree of control. The Idaho IRS 20 Quiz to Determine 1099 vs Employee Status emphasizes looking at the relationship between the worker and the employer. Key factors include the behavioral control, financial control, and the type of relationship established. By understanding these criteria, you can better navigate employment classifications.

AB 5 requires the application of the ABC test to determine if workers in California are employees or independent contractors for purposes of the Labor Code, the Unemployment Insurance Code, and the Industrial Welfare Commission (IWC) wage orders.

Pay basis: If you pay a worker on an hourly, weekly, or monthly basis, the IRS will consider it a sign the worker is your employee. An independent is generally paid by the job, project, assignment, etc., or receives a commission or similar fee.

A 1099 refers to the tax form companies must provide to independent contractors for work performed throughout the year. Business taxpayers must report nonemployee compensation of $600 or more to the IRS using a Form 1099-NEC, Nonemployee Compensation.

If you have a written contract to complete a specific task or project for a predetermined sum of money, you are probably a 1099 worker. However, if your employment is open-ended, without a contract and subject to a job description, you will typically be considered an employee.