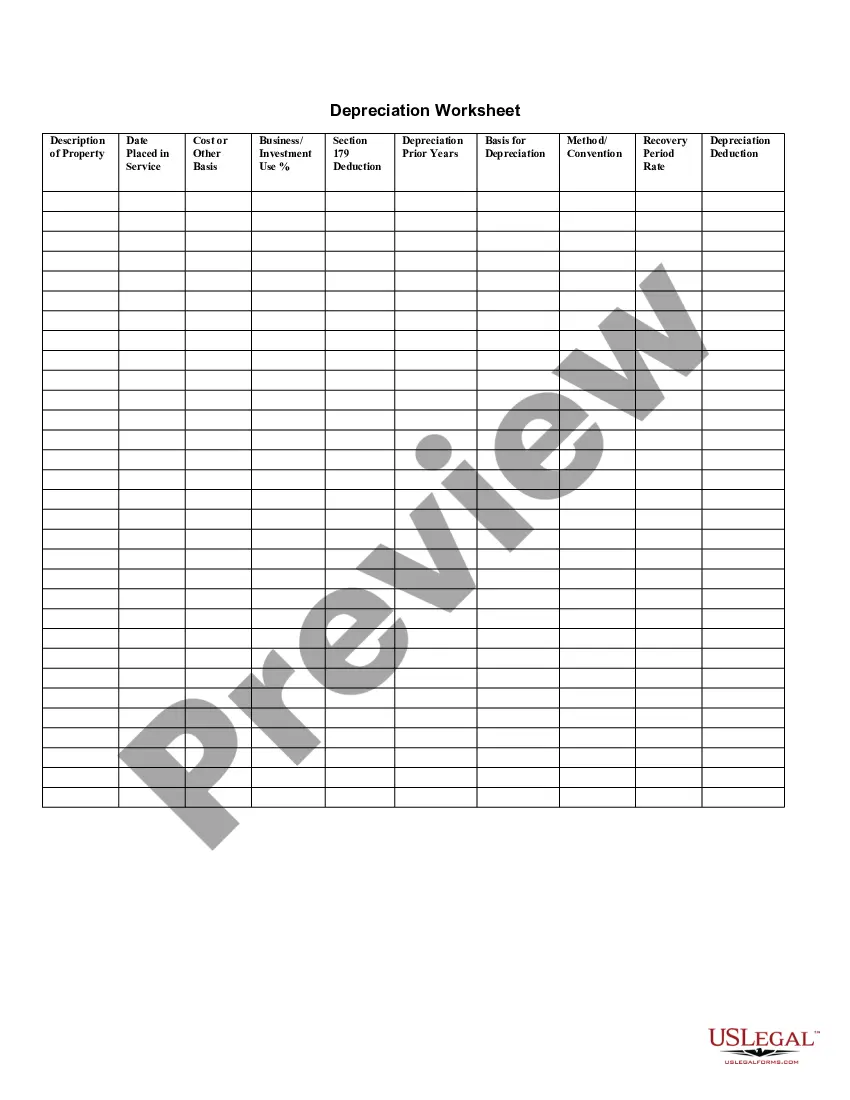

Iowa Depreciation Schedule

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Depreciation Schedule?

Locating the appropriate authentic document template can be rather challenging.

Clearly, there are numerous templates accessible online, but how do you find the genuine form you require.

Utilize the US Legal Forms website. The service offers a vast collection of templates, such as the Iowa Depreciation Schedule, suitable for business and personal needs.

You can examine the form using the Review button and read the form description to verify it is the correct one for you.

- All the forms are verified by experts and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Download button to obtain the Iowa Depreciation Schedule.

- Use your account to review the official forms you have previously purchased.

- Navigate to the My documents section of your account and get another copy of the document you need.

- If you're a new user of US Legal Forms, follow these simple steps.

- First, ensure you've selected the correct form for your locality/state.

Form popularity

FAQ

For new or used passenger automobiles eligible for bonus depreciation in 2021, the first-year limitation is increased by an additional $8,000, to $18,200.

The new law increases the bonus depreciation percentage from 50 percent to 100 percent for qualified property acquired and placed in service after Sept.

2020 IA 4562A InstructionsClaimed bonus depreciation during the tax year on federal form 4562, Depreciation and Amortization; federal form 2106, Employee Business Expenses; Schedule C, Profit or Loss from Business; Schedule F, Profit or Loss from Farming, or any other federal form where depreciation was deducted.

In addition, under Senate File 619, bonus depreciation will be allowed for Iowa purposes for property placed in service in tax years beginning on or after January 1, 2021.

In addition, under Senate File 619, bonus depreciation will be allowed for Iowa purposes for property placed in service in tax years beginning on or after January 1, 2021.

For bonus depreciation purposes, eligible property is in one of the classes described in § 168(k)(2): MACRS property with a recovery period of 20 years or less, depreciable computer software, water utility property, or qualified leasehold improvement property.

It was scheduled to go down to 40% in 2018 and 30% in 2019, and then not be available in 2020 and beyond. The Tax Cuts and Jobs Act, enacted at the end of 2018, increases first-year bonus depreciation to 100%. It goes into effect for any long-term assets placed in service after September 27, 2017.

Therefore, Iowa now conforms to bonus depreciation and remains decoupled, as it has been since 2020, from the IRC section 163(j) limitation.

The states that do not conform simply do not allow bonus depreciation and no additional deduction for bonus depreciation is allowed....States that do not conform to the new rules:Arizona.Arkansas.California.Connecticut.District of Columbia.Florida.Georgia.Hawaii.More items...