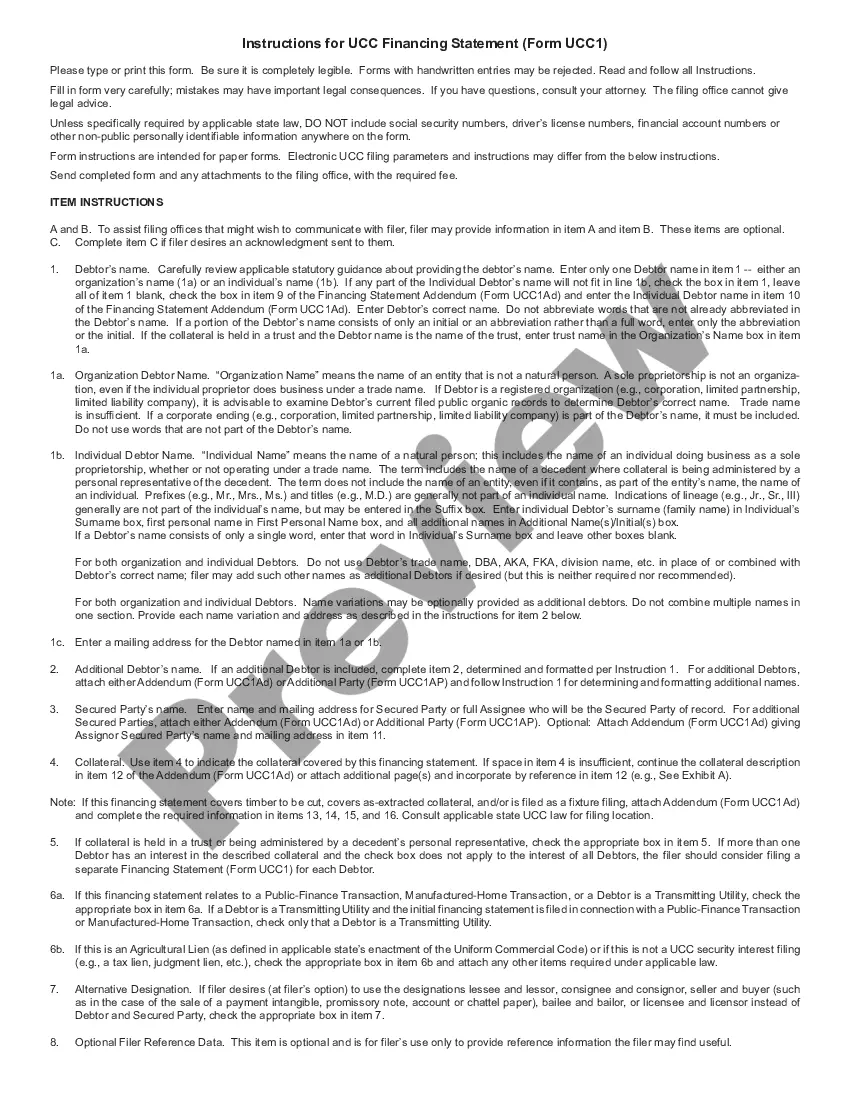

Iowa Exhibit to UCC-1 Financing Statement regarding a Fixture Filing for a Commercial Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Exhibit To UCC-1 Financing Statement Regarding A Fixture Filing For A Commercial Loan?

Choosing the best legal papers design could be a battle. Obviously, there are plenty of themes available on the Internet, but how will you get the legal form you want? Utilize the US Legal Forms website. The services offers 1000s of themes, like the Iowa Exhibit to UCC-1 Financing Statement regarding a Fixture Filing for a Commercial Loan, which you can use for organization and private needs. Each of the varieties are checked by pros and meet up with federal and state specifications.

When you are presently registered, log in to the accounts and then click the Acquire button to obtain the Iowa Exhibit to UCC-1 Financing Statement regarding a Fixture Filing for a Commercial Loan. Utilize your accounts to look from the legal varieties you have bought in the past. Visit the My Forms tab of your accounts and have another copy in the papers you want.

When you are a whole new consumer of US Legal Forms, listed here are basic directions that you can stick to:

- Initially, make certain you have selected the right form to your area/state. You are able to check out the shape making use of the Preview button and look at the shape information to ensure this is the best for you.

- In case the form will not meet up with your preferences, utilize the Seach industry to obtain the right form.

- Once you are certain that the shape would work, go through the Get now button to obtain the form.

- Opt for the prices strategy you would like and type in the required info. Create your accounts and pay for your order with your PayPal accounts or charge card.

- Choose the submit format and down load the legal papers design to the product.

- Complete, modify and print out and indicator the acquired Iowa Exhibit to UCC-1 Financing Statement regarding a Fixture Filing for a Commercial Loan.

US Legal Forms may be the most significant library of legal varieties in which you can discover various papers themes. Utilize the service to down load skillfully-manufactured files that stick to state specifications.

Form popularity

FAQ

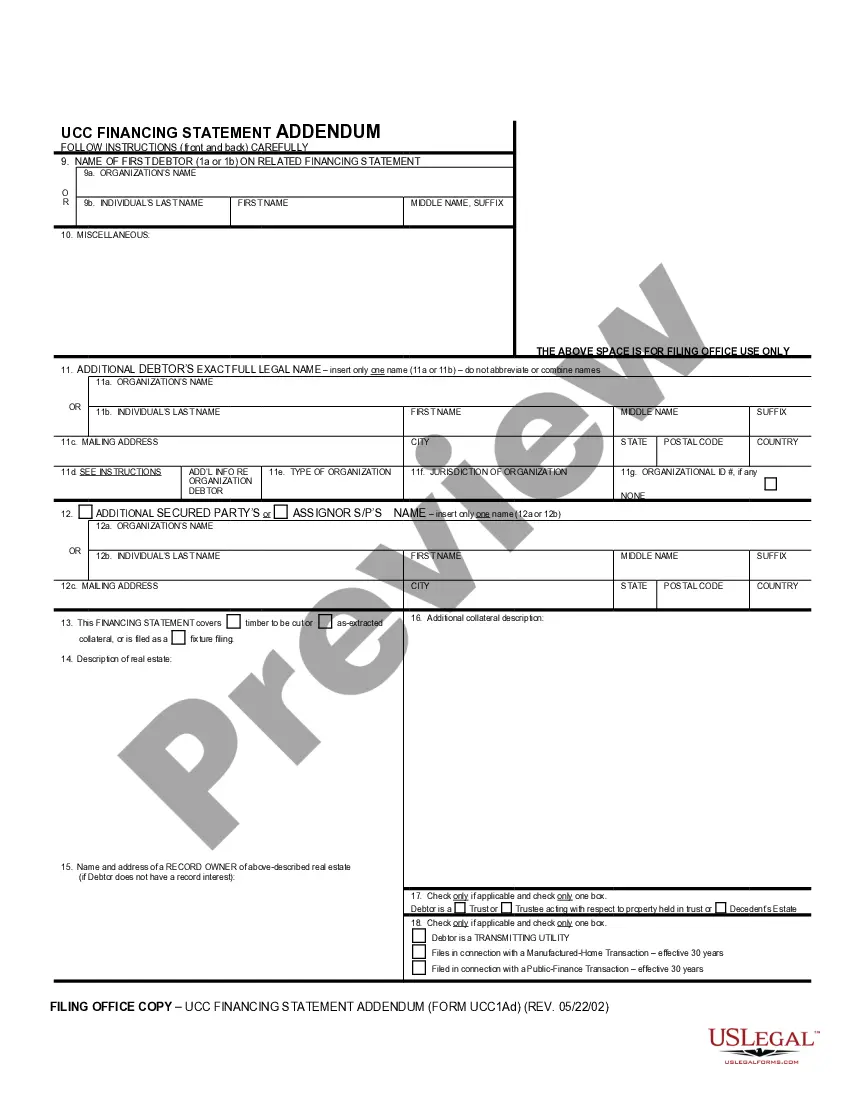

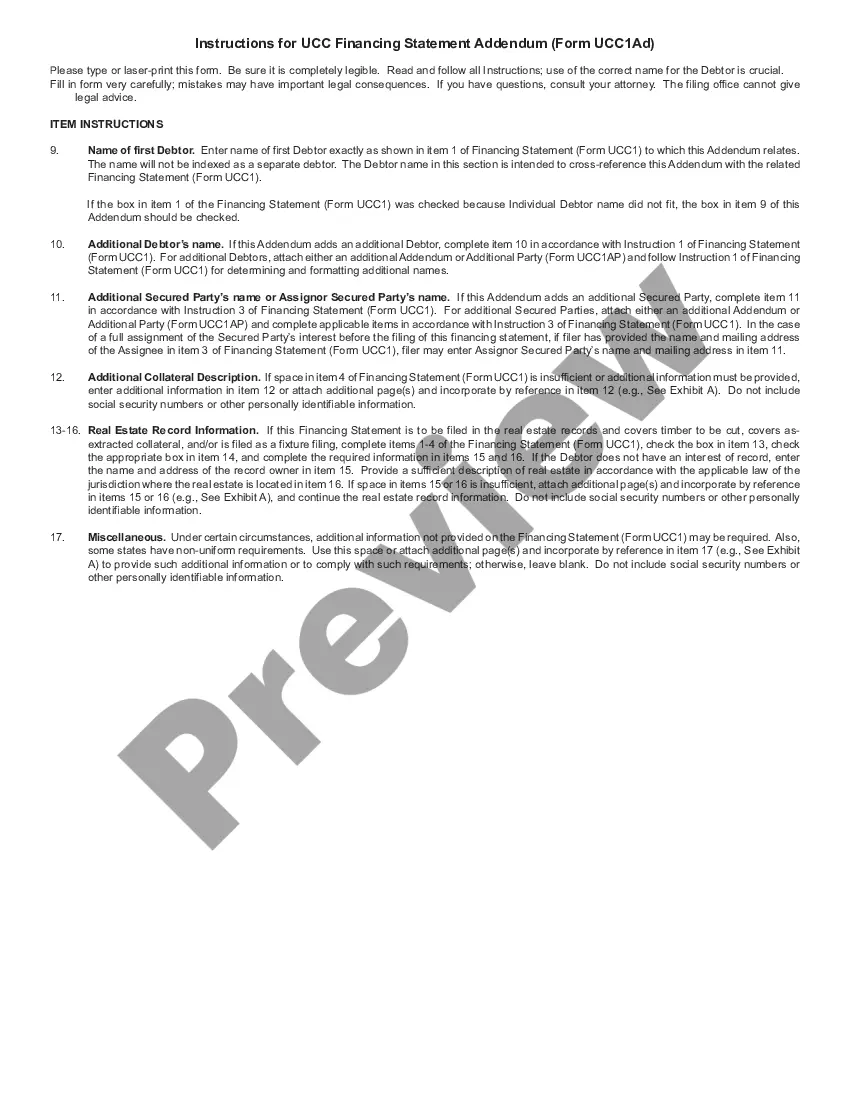

A fixture filing is a UCC-1 financing statement authorized and made in ance with the UCC adopted in the state in which the related real property is located. It covers property that is, or will be, affixed to improvements to such real property.

"Amendment" means a UCC record that amends the information contained in a financing statement. Amendments include assignments, continuations and terminations. "Assignment" is an amendment that assigns all or part of a secured party's power to authorize an amendment to a financing statement.

Remember: as long as an asset has a UCC lien filed against it, you're not allowed to transfer, sell, or use it as collateral for any other loan.

In fact, it is sometimes called a UCC financing statement. A creditor files a UCC-1 to provide notice to interested parties that he or she has a security interest in a debtor's personal property. This personal property is being used as collateral in some type of secured transaction, usually a loan or a lease.

The UCC filing establishes a lien against the collateral the borrower uses to secure the loan ? giving the lender the right to claim that collateral as repayment in the case of default. However, in many cases, the terms UCC lien and UCC filing are used interchangeably.

How do I file a UCC-1? First, go to . ... A drop-down menu will appear. ... From here, you will be redirected to the ?UCC1? page. ... Next, you will fill out the ?Debtor's Name? information. ... Next, you will fill out the ?Secured Party's Name? information.

In general, a UCC filing is not bad for your business ? it simply serves as an official notice to other creditors that your lender has a security interest in one or all of your assets. However, UCC filings can impact your business credit, risk your company's assets and/or hinder your ability to get future financing.

In fact, it is sometimes called a UCC financing statement. A creditor files a UCC-1 to provide notice to interested parties that he or she has a security interest in a debtor's personal property. This personal property is being used as collateral in some type of secured transaction, usually a loan or a lease.