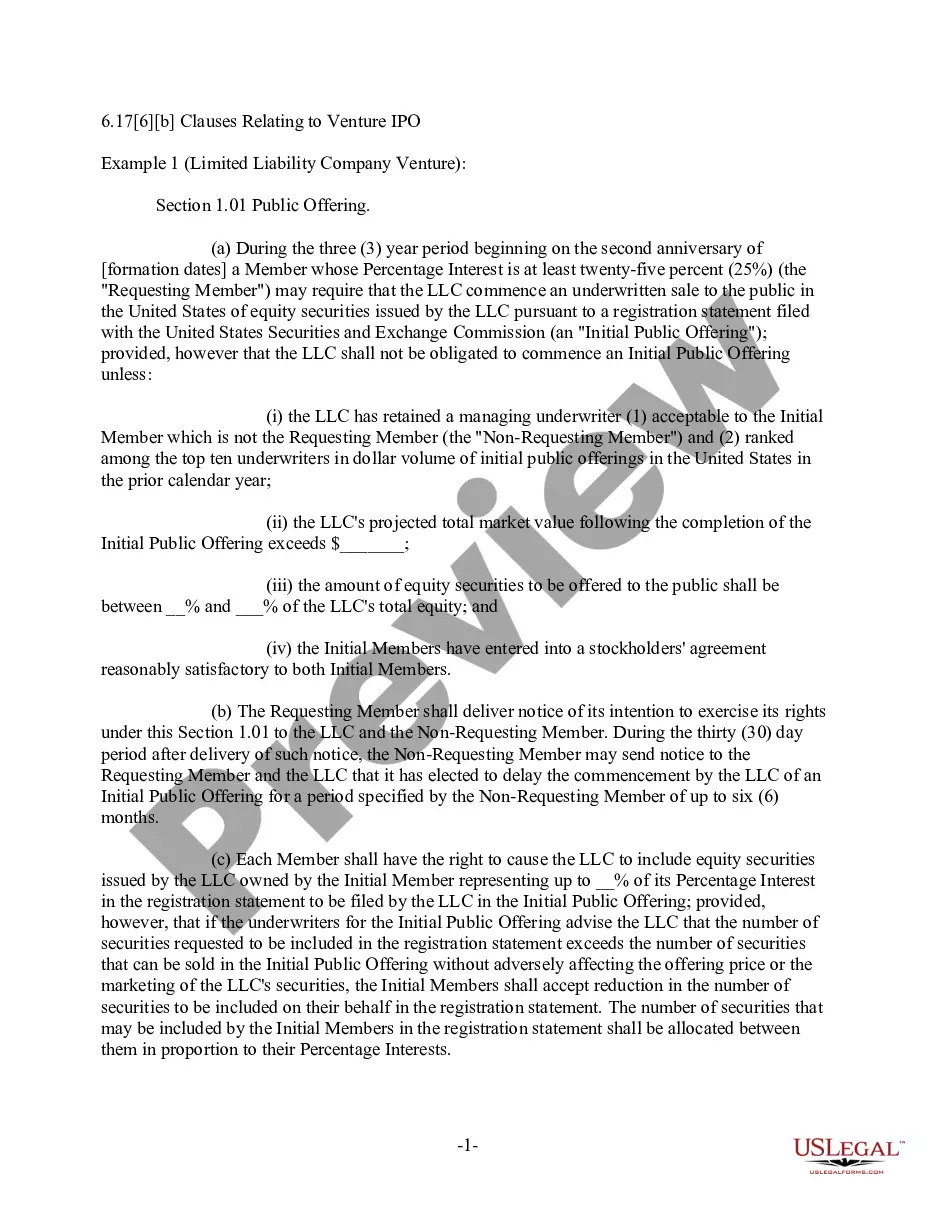

Guam Clauses Relating to Initial Capital contributions

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Clauses Relating To Initial Capital Contributions?

You may commit time online searching for the lawful file web template that fits the federal and state requirements you will need. US Legal Forms gives thousands of lawful kinds that happen to be evaluated by experts. It is simple to obtain or produce the Guam Clauses Relating to Initial Capital contributions from my services.

If you already possess a US Legal Forms profile, it is possible to log in and click the Acquire button. After that, it is possible to full, revise, produce, or indication the Guam Clauses Relating to Initial Capital contributions. Each and every lawful file web template you get is yours permanently. To acquire one more duplicate for any purchased form, proceed to the My Forms tab and click the corresponding button.

Should you use the US Legal Forms website the very first time, keep to the simple directions listed below:

- Very first, make certain you have selected the right file web template to the county/town of your choosing. See the form explanation to ensure you have picked the appropriate form. If readily available, make use of the Review button to appear throughout the file web template at the same time.

- In order to discover one more model of your form, make use of the Look for field to discover the web template that suits you and requirements.

- When you have found the web template you would like, click on Buy now to continue.

- Pick the prices strategy you would like, type your credentials, and register for a free account on US Legal Forms.

- Comprehensive the deal. You should use your charge card or PayPal profile to purchase the lawful form.

- Pick the formatting of your file and obtain it to the device.

- Make alterations to the file if necessary. You may full, revise and indication and produce Guam Clauses Relating to Initial Capital contributions.

Acquire and produce thousands of file templates using the US Legal Forms website, which offers the most important assortment of lawful kinds. Use expert and condition-specific templates to take on your small business or person requirements.

Form popularity

FAQ

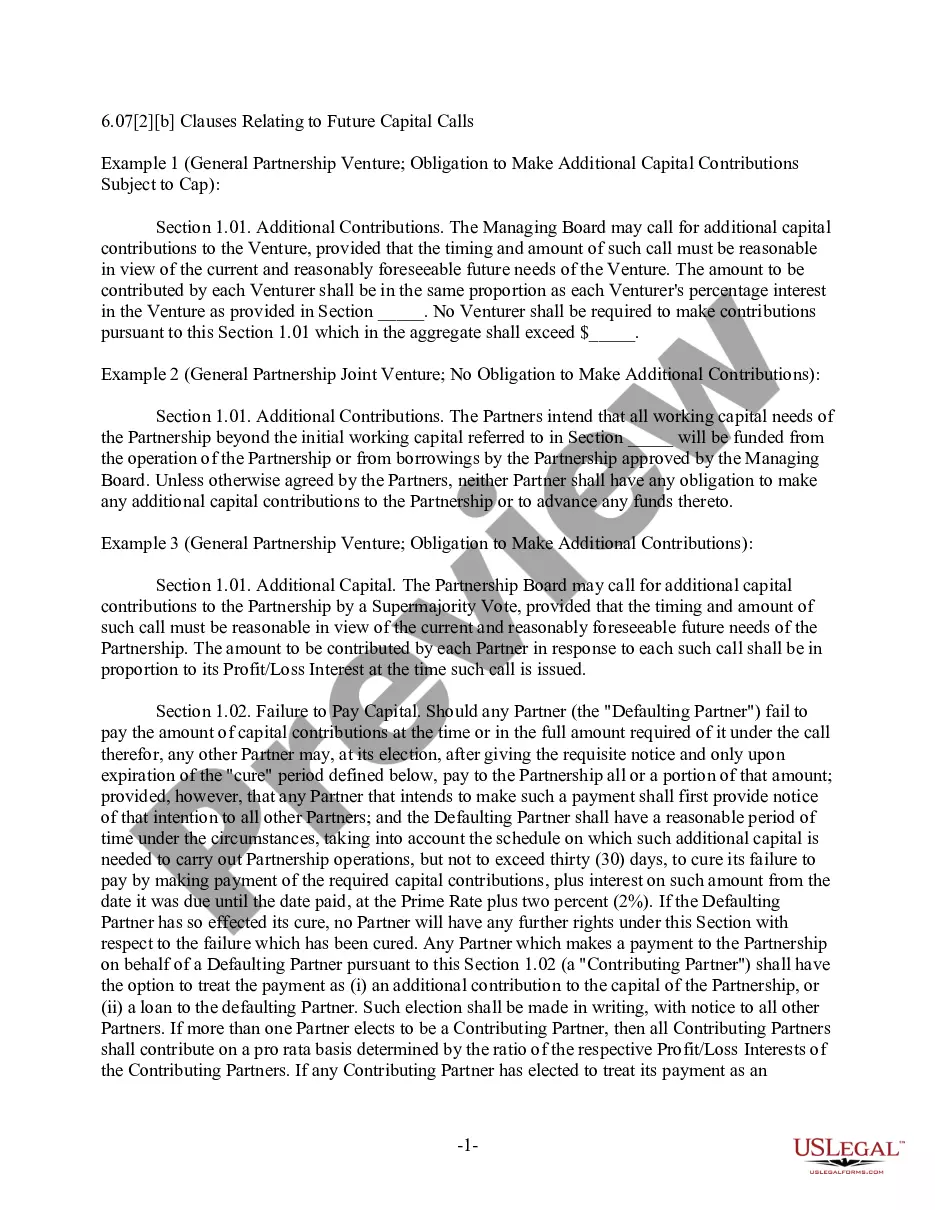

What is a Capital Contribution? A capital contribution refers to the cash or property that owners provide to their business. LLC members typically make initial capital contributions when opening the business and may contribute more throughout the company's lifetime.

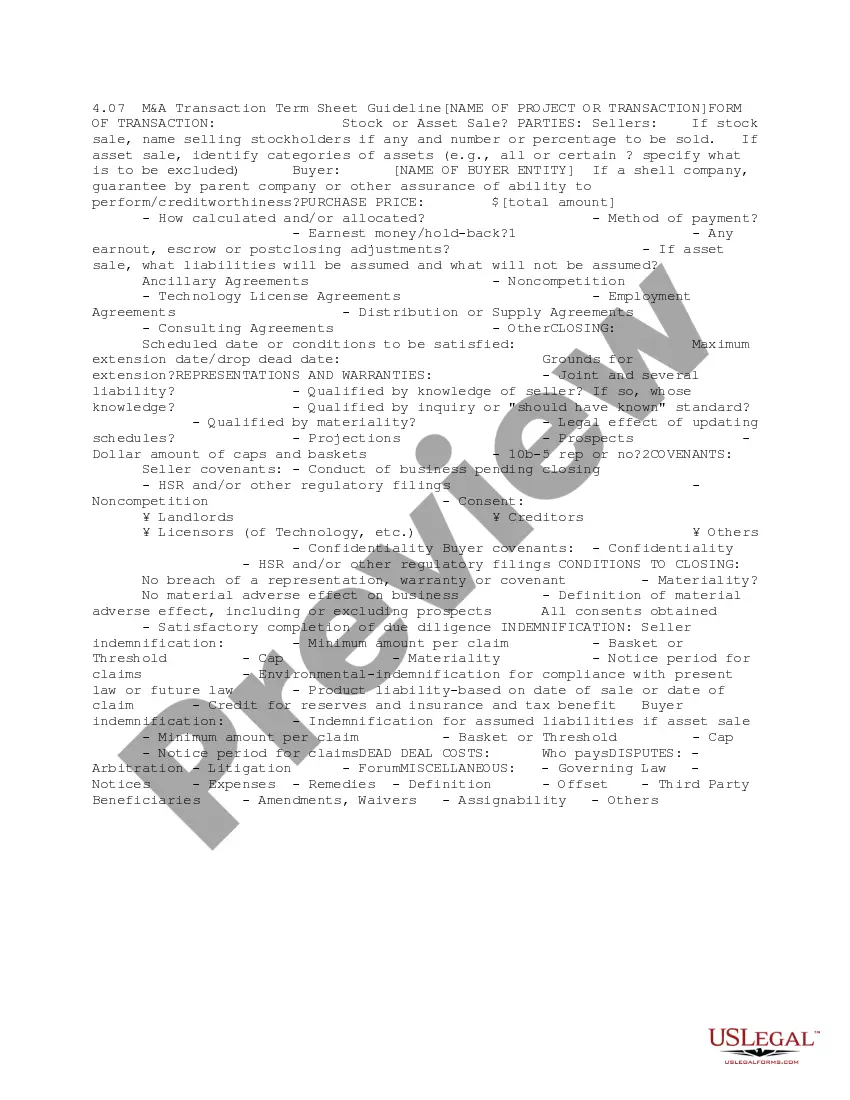

Contents Define the parties involved in the agreement and their respective roles. Identify the purpose of the agreement, including the capital contribution amount and any related terms and conditions. Detail any applicable taxes, fees, or charges related to the agreement.

An initial capital contribution is commonly seen as being given in exchange for membership in an LLC. However, while not typical, a person could contribute something to a company without being given membership, and a person could also be given membership without making any contribution.

An Initial Capital Stock Contribution is a specific amount of money you noted on your Operating Agreement that you as a shareholder in your LLC with S Corp tax formation would 'contribute' to get the business up and running.

This clause should be used when one member contributed real property to the joint venture in exchange for membership interests and another member has contributed capital. The capitalized terms and section references used in this clause should be conformed to the relevant joint venture operating agreement.