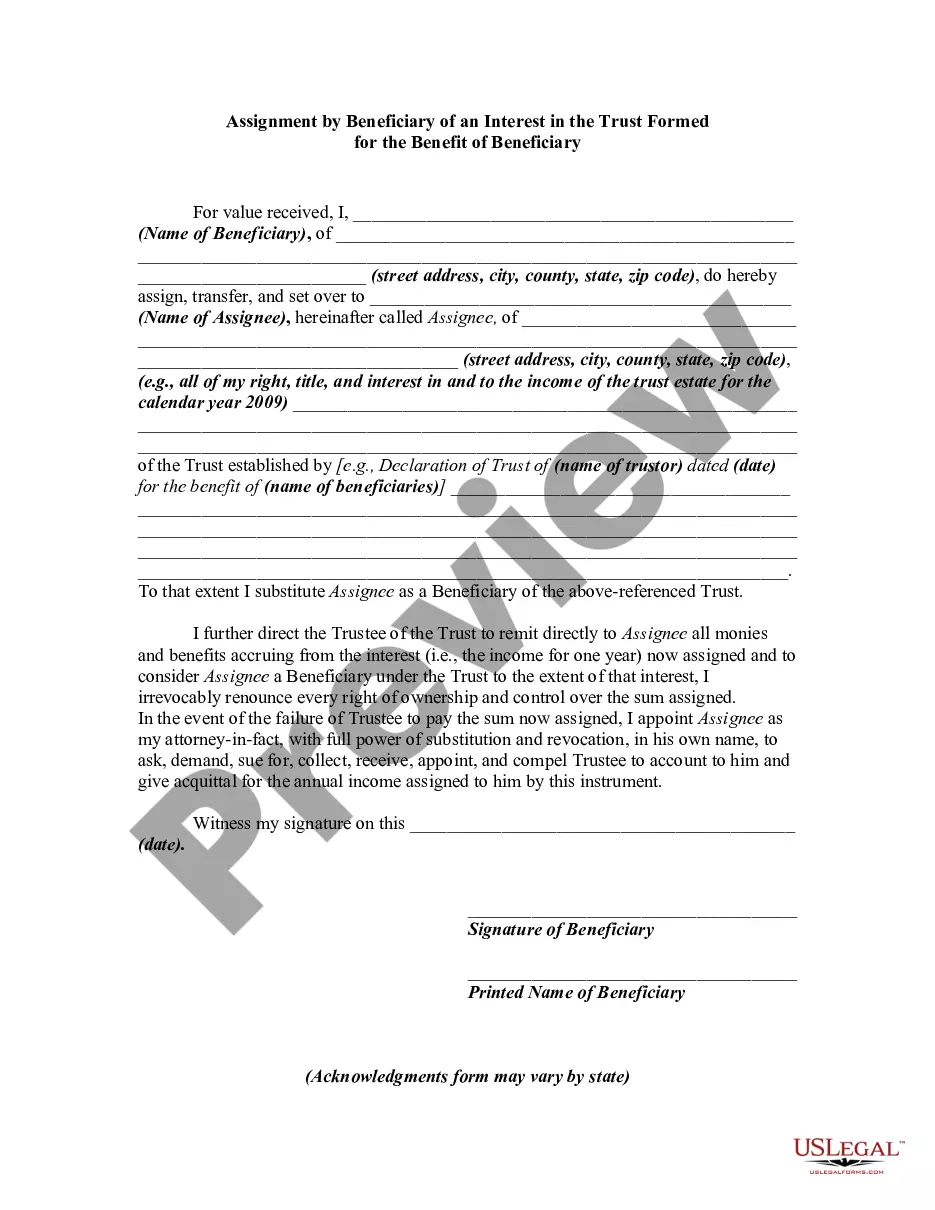

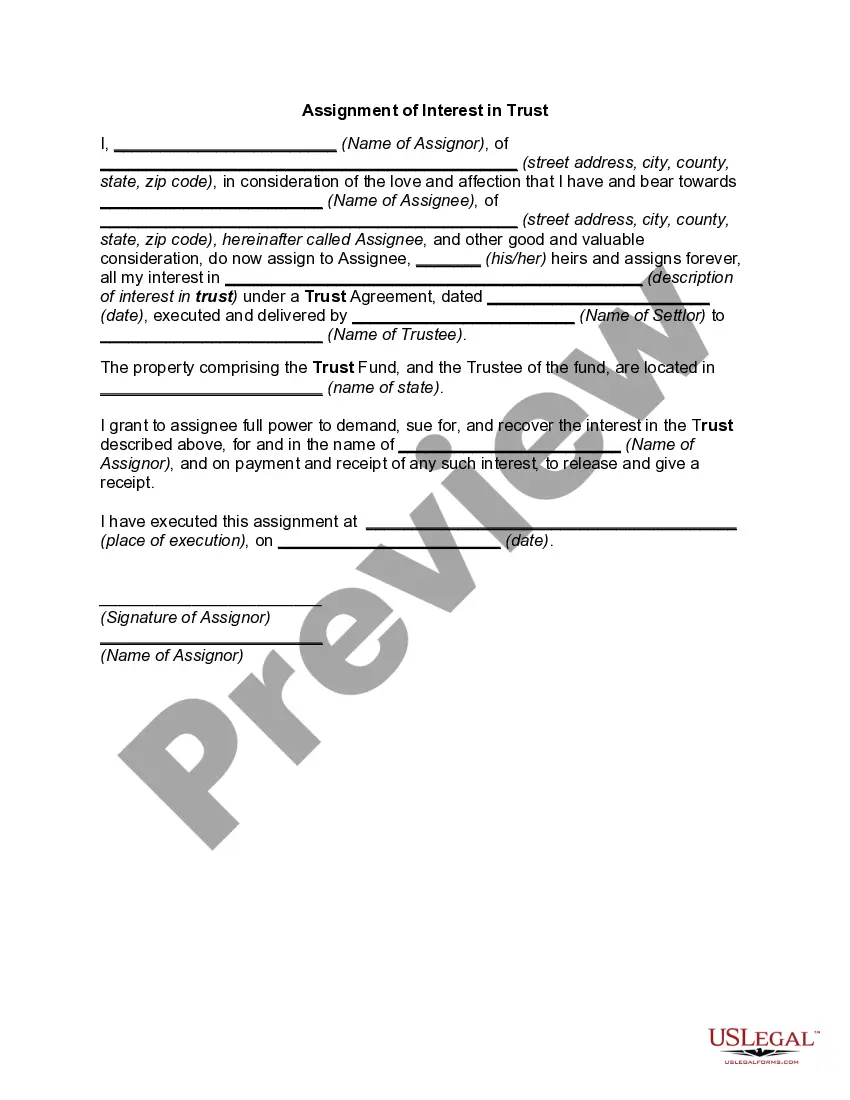

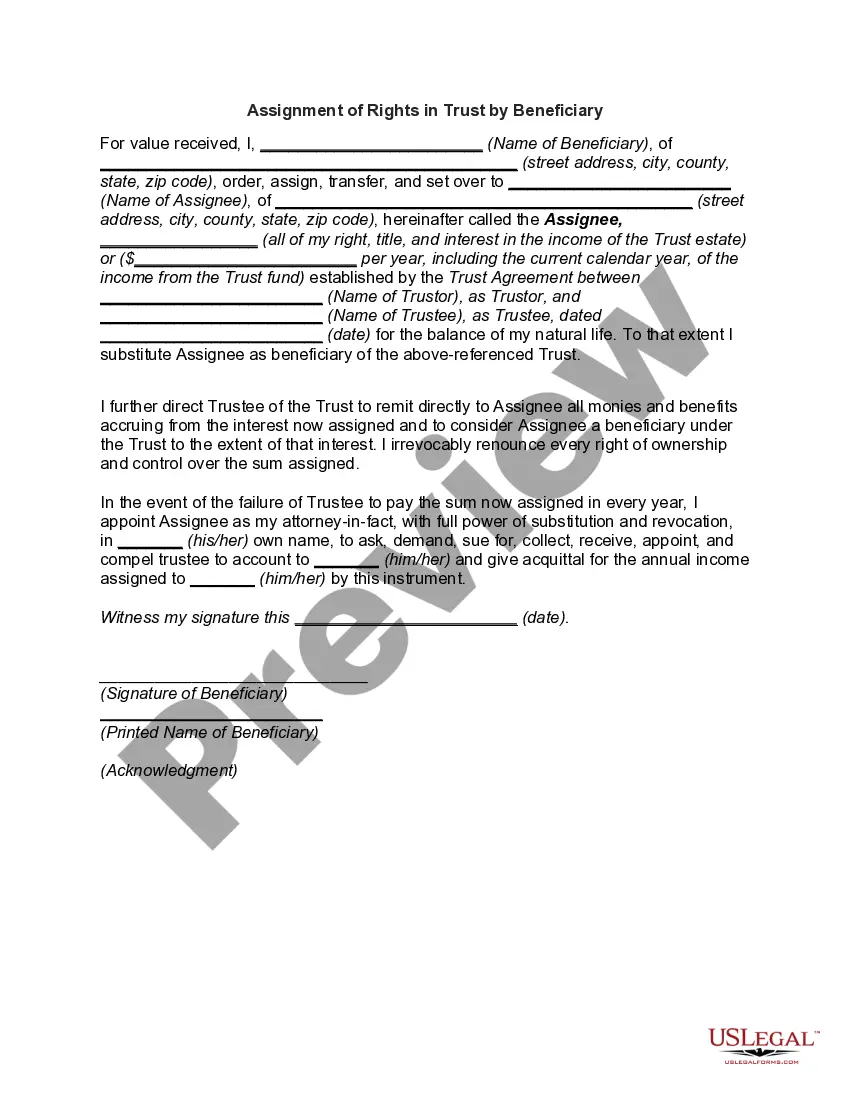

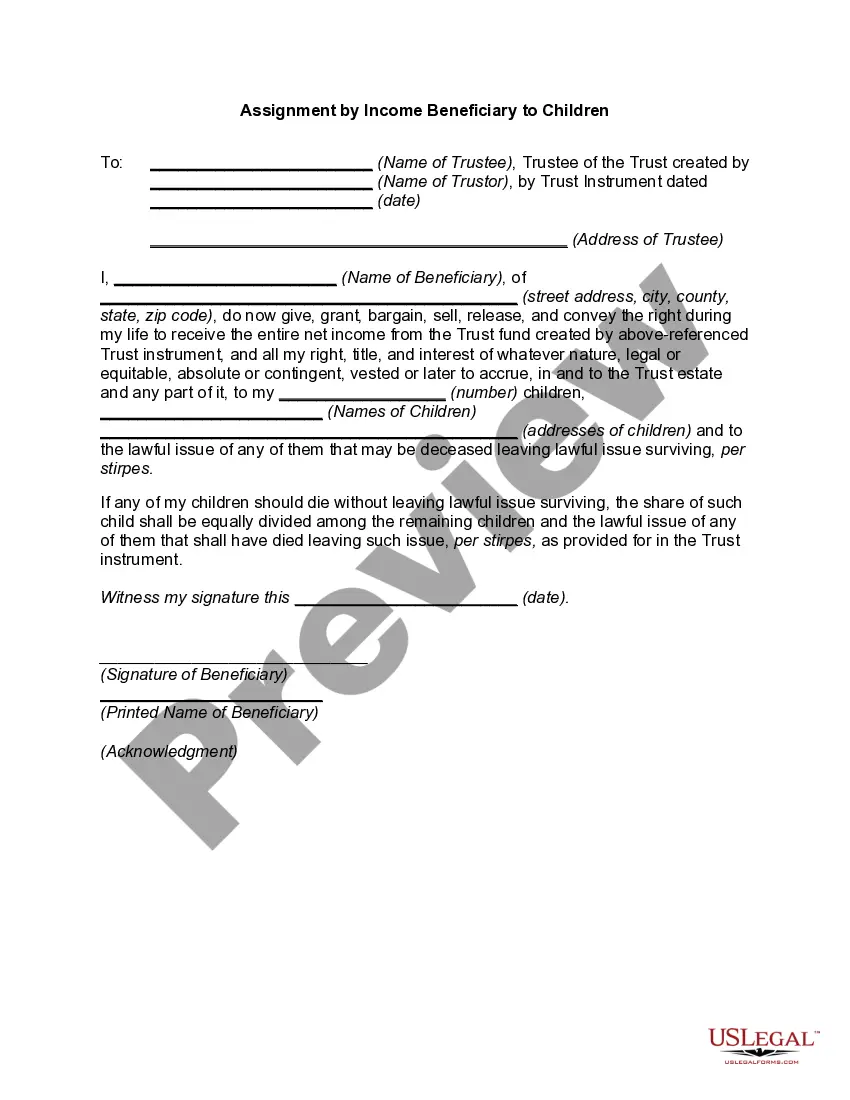

An assignment by a beneficiary of a portion of his or her interest in a trust is usually regarded as a transfer of a right, title, or estate in property rather than a chose in action (like an account receivable). As a general rule, the essentials of such an assignment or transfer are the same as those for any transfer of real or personal property. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Guam Assignment by Beneficiary of a Percentage of the Income of a Trust

Instant download

Description

Free preview

How to fill out Assignment By Beneficiary Of A Percentage Of The Income Of A Trust?

Locating the appropriate authentic document template can be a challenge. Of course, there are numerous templates available online, but how do you find the authentic form you require? Utilize the US Legal Forms website. The platform provides thousands of templates, including the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust, that can be utilized for business and personal needs. All of the forms are vetted by professionals and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Acquire button to obtain the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust. Use your account to browse the legal forms you have previously purchased. Navigate to the My documents section of your account to retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple steps you can follow: First, ensure you have selected the correct form for your city/region. You can review the form using the Review option and read the form description to verify it is suitable for you. If the form does not meet your needs, utilize the Search area to find the right form. Once you are confident that the form is appropriate, click the Acquire now button to get the form. Choose the pricing plan you want and enter the required information. Create your account and pay for the order using your PayPal account or credit card. Select the file format and download the legal document template to your device. Complete, edit, print, and sign the received Guam Assignment by Beneficiary of a Percentage of the Income of a Trust.

US Legal Forms is the largest repository of legal forms, allowing you to access a wide range of document templates.

- Use the service to download professionally crafted documents that meet state requirements.

- Access a vast library of legal forms to find numerous document templates.

- Ensure compliance with federal and state regulations.

- Receive expert-verified forms catered to both business and personal use.

- Log In easily to retrieve previously purchased documents.

- Navigate effortlessly through various templates available on the platform.

Form popularity

FAQ

Reporting beneficiary income involves including that income on the tax return of the beneficiary who receives it. You should report this income on Form 1040, indicating the income derived from the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust. Proper reporting ensures compliance with tax regulations and helps beneficiaries understand their financial obligations.

Income in respect of a decedent refers to earnings that the deceased has not received yet, but that belong to them. Common examples include wages, interest, dividends, rental income, and business profits that are due but unpaid at the time of death. Understanding these aspects is crucial when dealing with a Guam Assignment by Beneficiary of a Percentage of the Income of a Trust, as these incomes affect the distribution to beneficiaries.

Reporting income from a trust involves filing the appropriate tax forms, which usually include Form 1041 for the trust itself and Schedule K-1 for beneficiaries. Each beneficiary should also report their share of income on their individual tax returns. Utilizing tools and resources from platforms like US Legal Forms can streamline this process, ensuring that you accurately account for your Guam Assignment by Beneficiary of a Percentage of the Income of a Trust.

To allocate trust income to beneficiaries, you start by determining the trust income for the period in question. Afterward, utilize the instructions in the trust agreement, which may specify allocations based on percentages, such as the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust. This clear guidance allows for fair distributions according to the beneficiaries' interests.

Yes, the beneficiary of a foreign non-grantor trust is typically subject to U.S. taxation on income that is distributed to them. This includes income derived from the trust, even if it is based on the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust. Understanding global tax implications can help beneficiaries manage their liabilities effectively.

To allocate trust income, first identify the total income generated by the trust. Next, apply the specific terms outlined in the trust document regarding distributions. This often includes considering the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust, which allows beneficiaries to receive a predetermined share of trust income, simplifying the process of allocation.

Income distribution from a unit trust typically occurs based on the number of units held by each beneficiary. The trustee calculates the total income generated by the trust and distributes it proportionately to the beneficiaries according to their unit holdings. With mechanisms like Guam Assignment by Beneficiary of a Percentage of the Income of a Trust, beneficiaries can effectively manage their share of the income while ensuring the trust operates as intended. Familiarizing yourself with these processes can help maximize the benefits of your trust.

While trusts offer various benefits, they can also present disadvantages for beneficiaries. One key concern is that assets held in trust may not be easily accessible, which can create financial strain in emergencies. The Guam Assignment by Beneficiary of a Percentage of the Income of a Trust provisions can help alleviate some of these issues by allowing beneficiaries a structured way to receive income. Understanding the specific terms of the trust is essential to navigate these potential drawbacks.

When beneficiaries receive trust distributions, they may face tax implications depending on the trust type and the income generated. For example, if the trust distributes income, it is generally taxable to the beneficiaries who receive it. The Guam Assignment by Beneficiary of a Percentage of the Income of a Trust allows beneficiaries to manage how they receive their share, potentially affecting their tax situation. Consulting with a tax advisor can help clarify what distributions mean for your tax obligations.

Yes, you can assign income to a trust, and doing so can optimize income distribution through the Guam Assignment by Beneficiary of a Percentage of the Income of a Trust. This process involves specifying how much of your income will be directed into the trust for various purposes, including supporting beneficiaries. Engaging with a legal expert can provide the necessary guidance for making these assignments correctly. Uslegalforms can assist with documentation to ensure this process is handled smoothly.