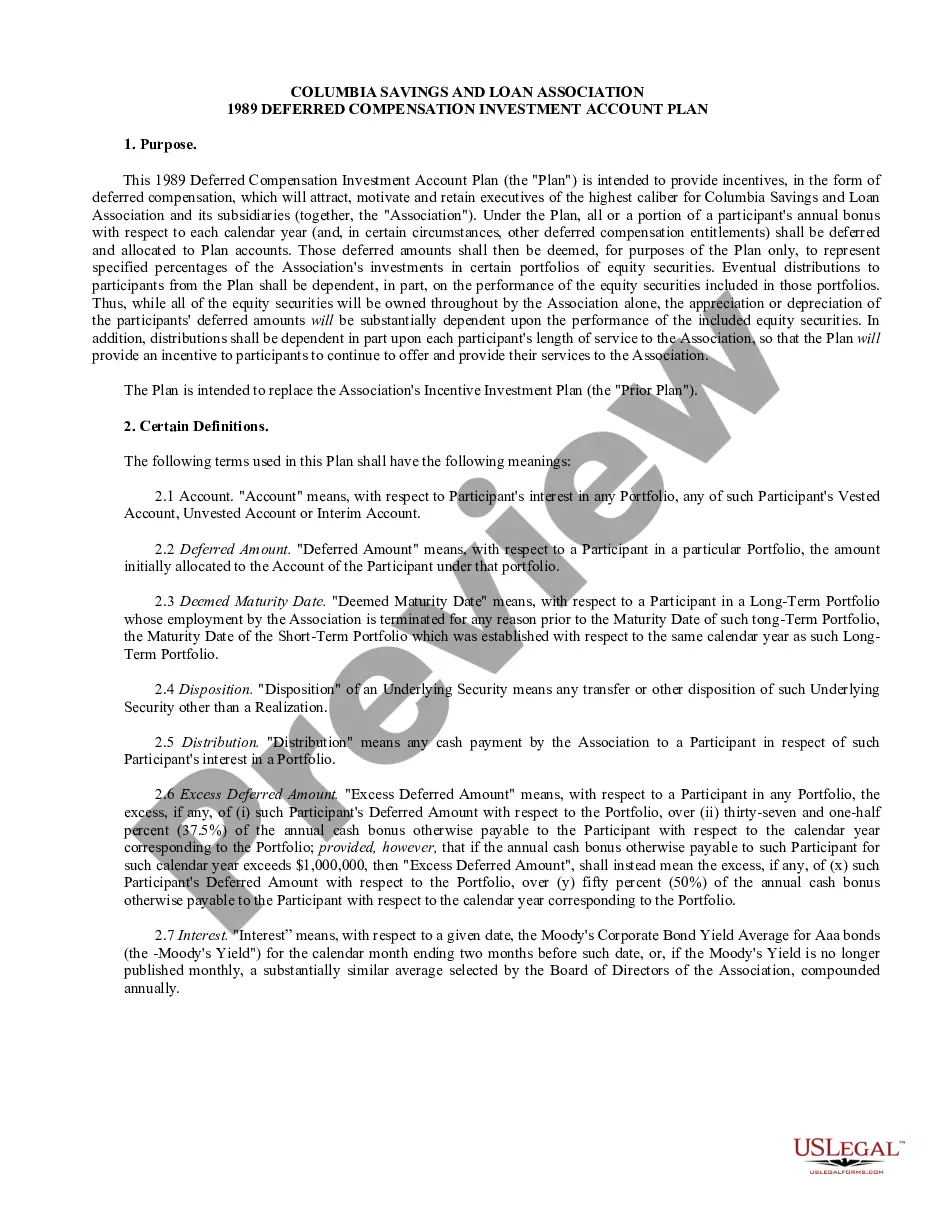

Georgia Approval of deferred compensation investment account plan

Description

How to fill out Approval Of Deferred Compensation Investment Account Plan?

It is possible to spend hrs on-line attempting to find the legal record web template which fits the federal and state needs you need. US Legal Forms provides 1000s of legal forms that are analyzed by experts. It is possible to down load or print the Georgia Approval of deferred compensation investment account plan from the support.

If you already possess a US Legal Forms profile, it is possible to log in and then click the Download button. Afterward, it is possible to total, modify, print, or indication the Georgia Approval of deferred compensation investment account plan. Every legal record web template you purchase is your own property eternally. To obtain an additional duplicate of the obtained type, visit the My Forms tab and then click the corresponding button.

If you use the US Legal Forms website the very first time, adhere to the simple directions listed below:

- Very first, make certain you have chosen the right record web template for your state/city of your choice. Read the type outline to ensure you have picked out the correct type. If readily available, utilize the Review button to search throughout the record web template at the same time.

- If you want to locate an additional model in the type, utilize the Search discipline to get the web template that suits you and needs.

- When you have found the web template you desire, simply click Acquire now to continue.

- Select the costs prepare you desire, key in your credentials, and sign up for a merchant account on US Legal Forms.

- Full the financial transaction. You can use your credit card or PayPal profile to purchase the legal type.

- Select the structure in the record and down load it to your system.

- Make changes to your record if required. It is possible to total, modify and indication and print Georgia Approval of deferred compensation investment account plan.

Download and print 1000s of record themes making use of the US Legal Forms site, that offers the most important assortment of legal forms. Use expert and state-distinct themes to deal with your company or individual requirements.

Form popularity

FAQ

457(b) Assets can be withdrawn without penalty at any age upon separation from service from the plan sponsor, or age 70½ if still working.

Just like a 401(k) or 403(b) retirement savings plan, a 457 plan allows you to invest a portion of your salary on a pretax basis. The money grows, tax-deferred, waiting for you to decide what to do with it when you retire. You're about to retire.

Cons of 457(b) plans: Fewer investing options than 401(k)s (Not as common today) Only available to certain employees employed by state or local governments or qualifying nonprofits. Employer contributions count toward the annual limit. Non-governmental 457(b) plans are riskier.

Typically, you can't roll funds over from your 457(b) plan if you're still employed by, or ?in-service? with the company offering the plan. Some plans may allow an in-service withdrawal once you've reached a certain age. Once you leave that employment, you can roll over funds into an account of your choosing.

Key Differences Deferred compensation plans tend to offer better investment options than most 401(k) plans, but are at a disadvantage regarding liquidity. Typically, deferred compensation funds cannot be accessed, for any reason, before the specified distribution date.

All distributions are taxed as ordinary income. Roth contributions ? Contributions are made on an after-tax basis. Earnings accumulate on a tax-deferred basis, and distributions are tax-free if made five years after the initial contribution to the plan and the employee is over 59½.

While you are employed, your employer may permit you to take a withdrawal from your 457(b) plan due to an unforeseeable emergency. All unforeseeable emergency withdrawal requests will be reviewed in ance with the plan's procedures for a determination as to whether the withdrawal is permitted.

The plan is offered only to public service employees and employees at tax-exempt organizations. Participants are allowed to contribute up to 100% of their salaries up to a dollar limit for the year. The interest and earnings in the account are not taxed until the funds are withdrawn.