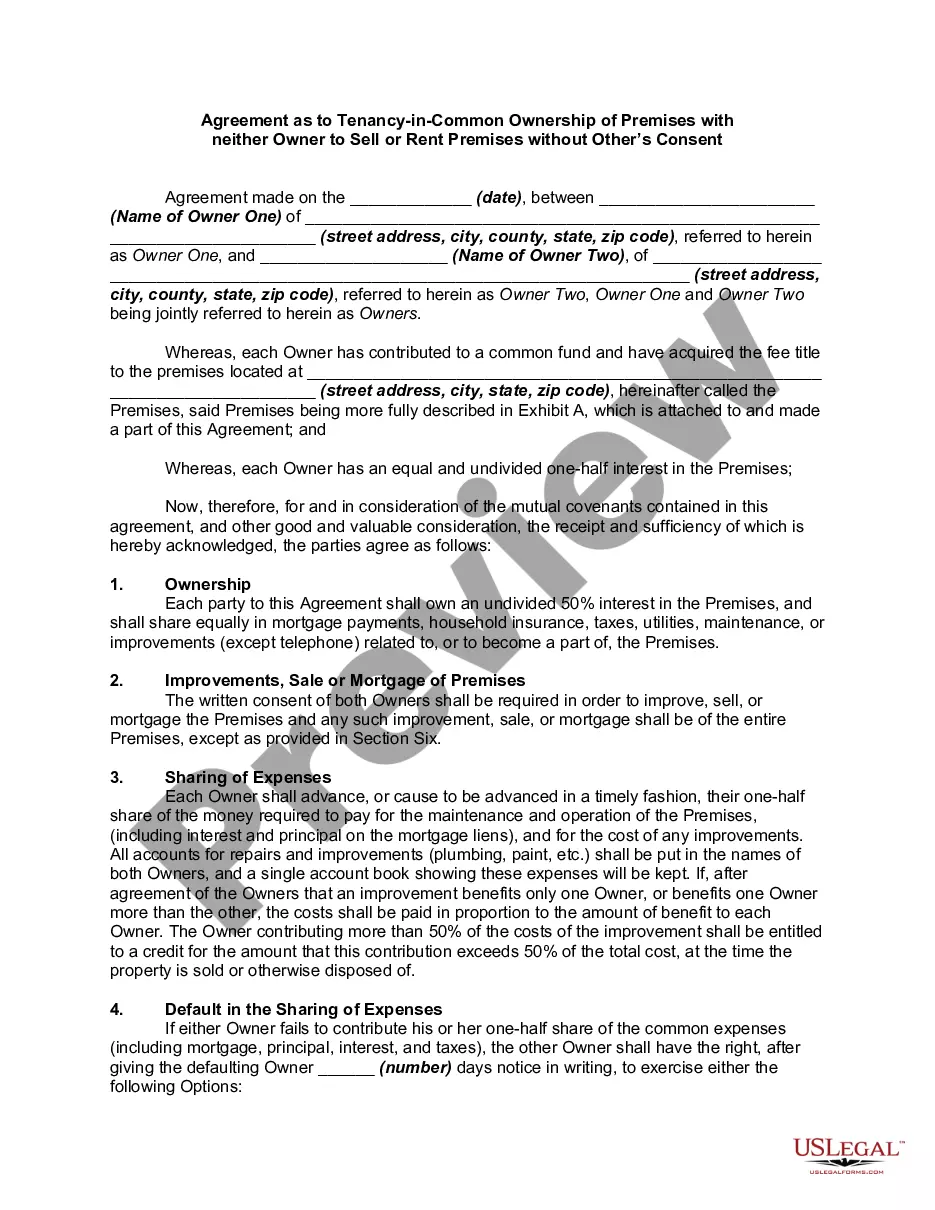

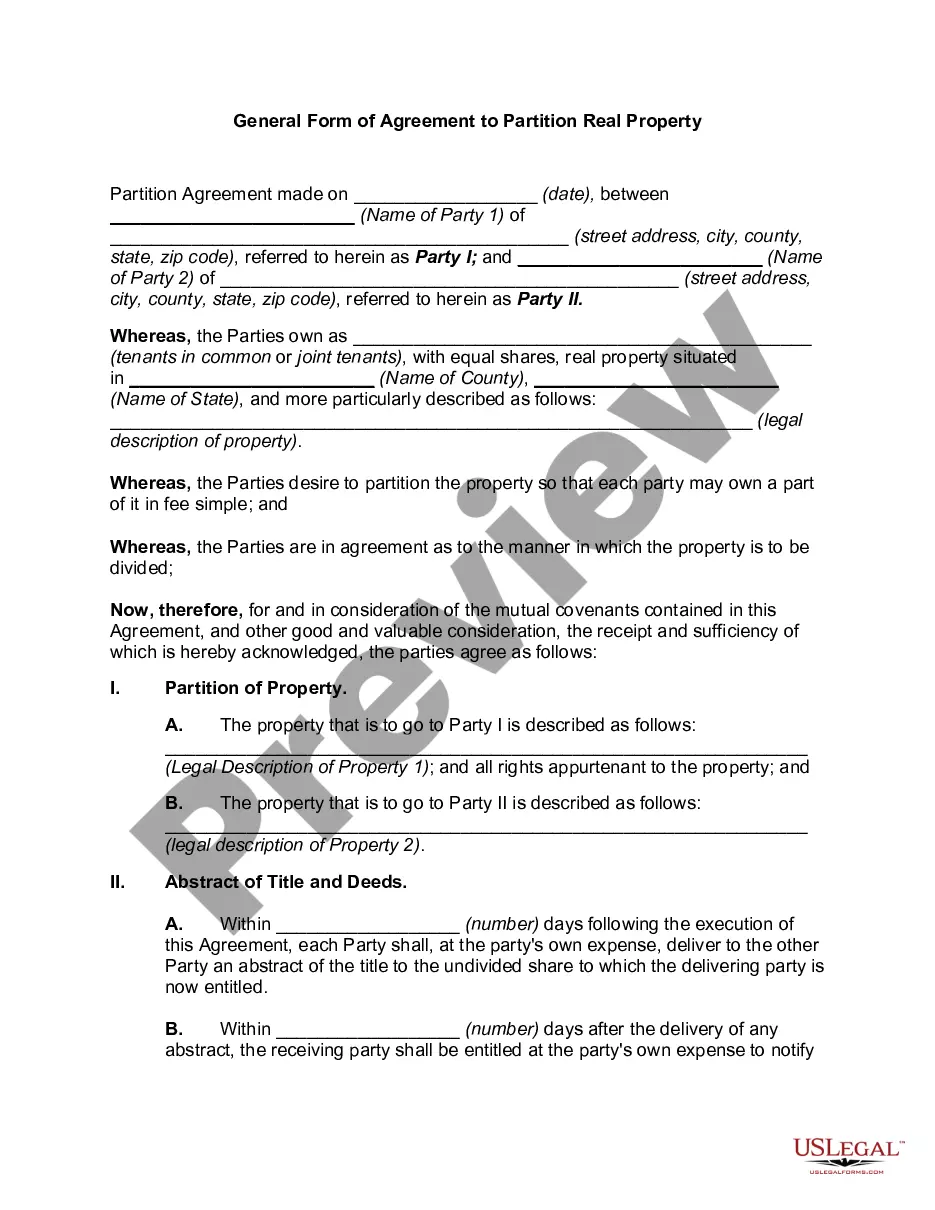

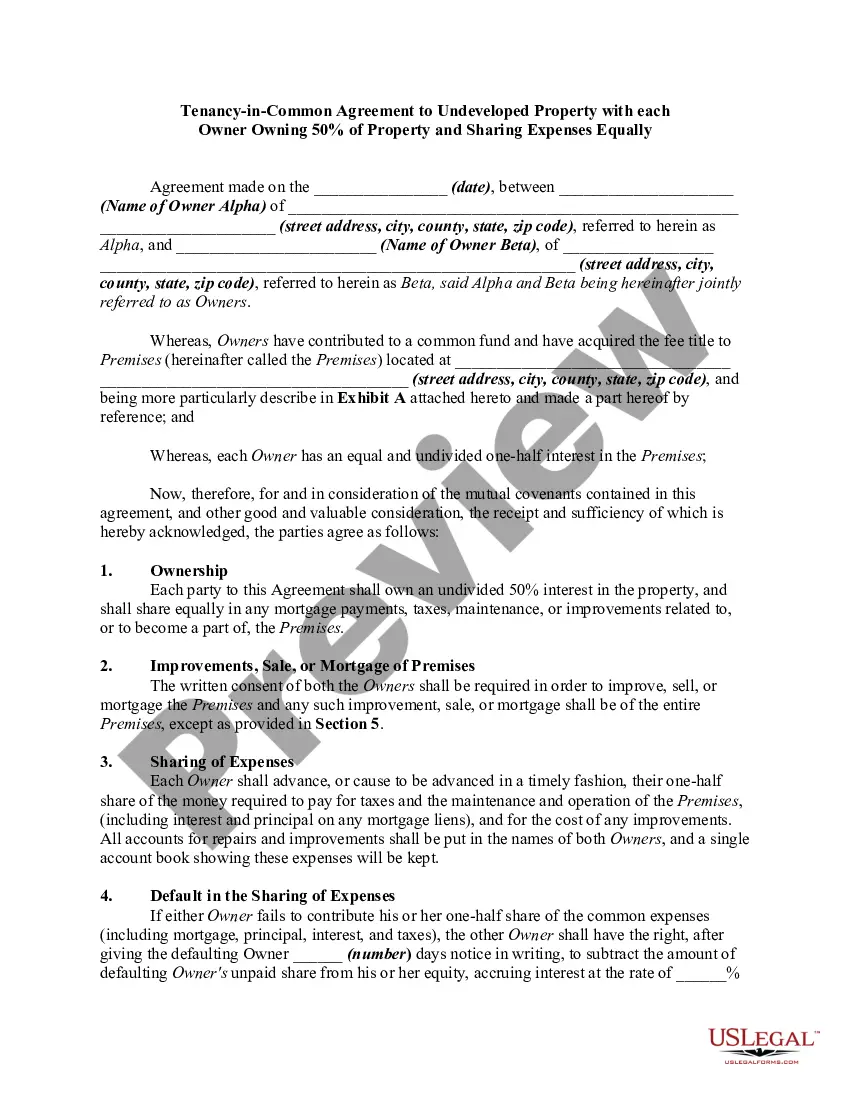

Tenants in common hold title to real or personal property so that each has an "undivided interest" in the property and all have an equal right to use the property. Tenants in common each own a portion of the property, which may be unequal, but have the right to possess the entire property.

There is no "right of survivorship" if one of the tenants in common dies, and each interest may be separately sold, mortgaged or willed to another. A tenancy in common interest is distinguished from a joint tenancy interest, which passes automatically to the survivor. Upon the death of a tenant in common there must be a court supervised administration of the estate of the deceased to transfer the interest in the tenancy in common.

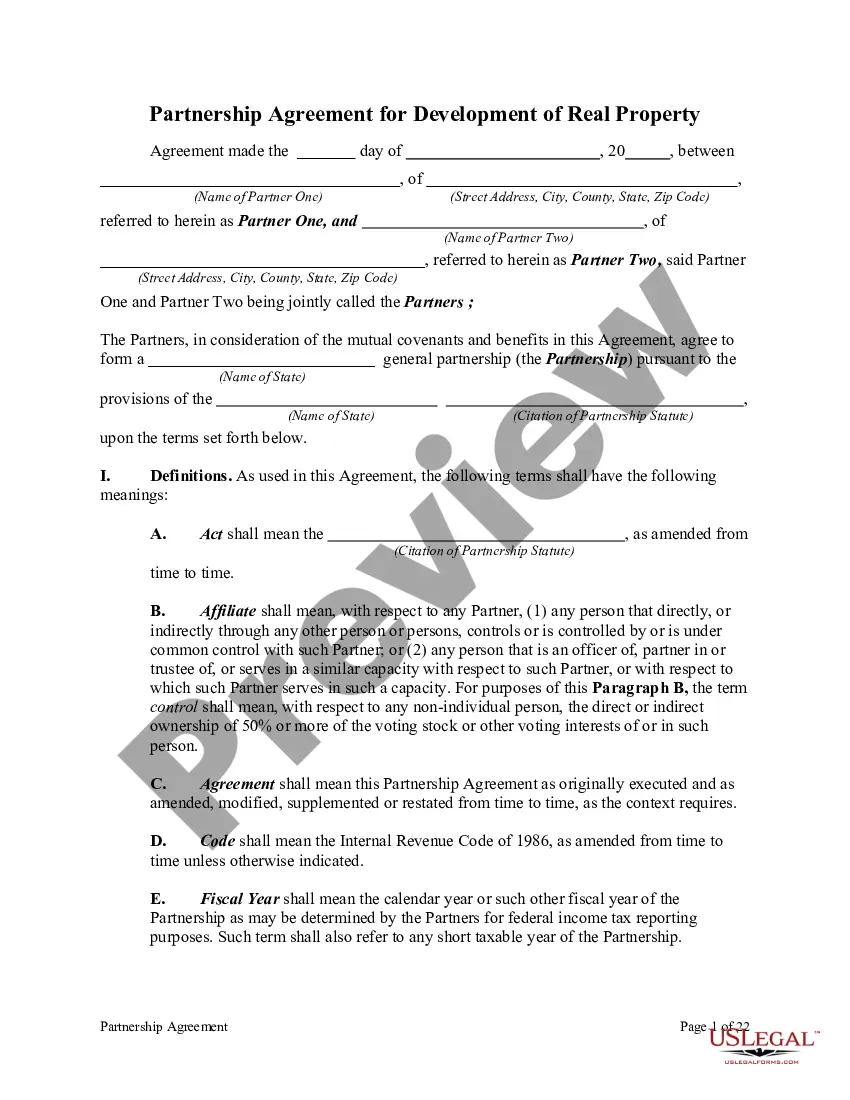

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.