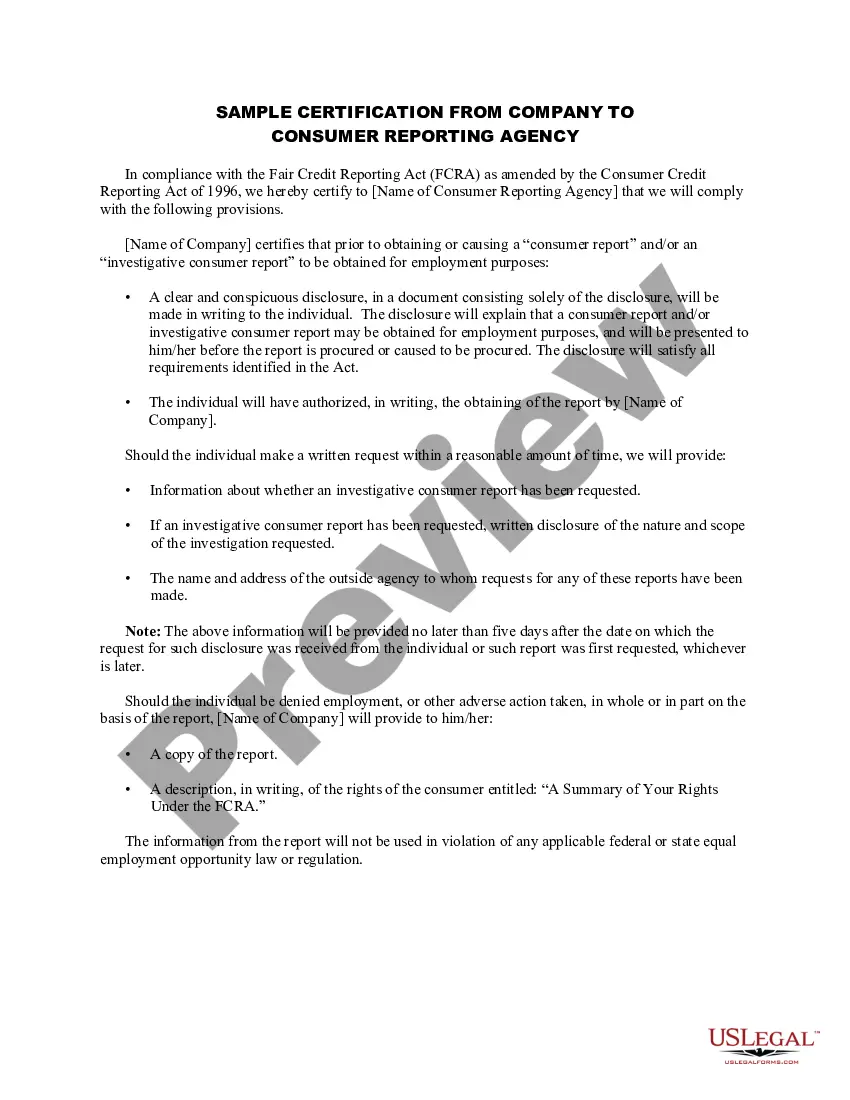

Florida FCRA Certification Letter to Consumer Reporting Agency

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out FCRA Certification Letter To Consumer Reporting Agency?

Finding the appropriate legal document template can be rather challenging.

Clearly, there are many designs accessible online, but how can you obtain the correct document you require.

Utilize the US Legal Forms website.

If you are a new customer of US Legal Forms, here are simple steps you should follow: First, ensure you have selected the correct document for your city/county. You can view the form using the Review button and check the form details to confirm that it is the right one for you.

- The service offers a vast array of templates, such as the Florida FCRA Certification Letter to Consumer Reporting Agency, which can be used for business and personal purposes.

- All of the forms are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Obtain button to receive the Florida FCRA Certification Letter to Consumer Reporting Agency.

- Use your account to view the legal forms you have purchased in the past.

- Go to the My documents tab in your account to retrieve another copy of the document you require.

Form popularity

FAQ

When your credit report states that account information disputed by the consumer meets FCRA requirements, it indicates that you have officially challenged certain entries. The credit reporting agency must then investigate the dispute and ensure the information complies with FCRA standards. This process is designed to protect consumers from potentially damaging inaccuracies. Utilizing a Florida FCRA Certification Letter to Consumer Reporting Agency may assist you in documenting your dispute effectively.

The importance of a FCRA letter lies in its role in protecting consumer rights. These letters help facilitate communication between consumers and reporting agencies, especially when challenging errors or requesting clarification. By using a Florida FCRA Certification Letter to Consumer Reporting Agency, you demonstrate your commitment to maintaining accurate financial records. This proactive approach can greatly benefit your credit standing.

If a credit bureau, creditor, or someone else violates the Fair Credit Reporting Act, you can sue. Under the Fair Credit Reporting Act (FCRA), you have a right to the fair and accurate reporting of your credit information.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete, or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer reporting agency may continue to report information it has verified as accurate.

The Fair Credit Reporting Act in Florida Florida has a protection law that provides for the rights to place a security freeze on a consumer report (501.005). Florida also has Section 626.9741 which applies to the use of credit reports and scores by insurers.

The Fair Credit Reporting Act is a law, passed in 1970, that regulates how credit reporting agencies and other businesses can use information regarding your credit history.

The FCRA requires agencies to remove most negative credit information after seven years and bankruptcies after seven to 10 years, depending on the kind of bankruptcy. Restrictions around who can access your reports.

Disclosures to consumers. (a) Every consumer reporting agency shall, upon request and proper identification of any consumer, clearly and accurately disclose to the consumer: (1) The nature and substance of all information (except medical information) in its files on the consumer at the time of the request.

A statement indicating that the account "meets FCRA requirements" may be added if a consumer disputes information on their credit report, but the credit bureau determines that the information is accurate. Additionally, it can be concluded that all information is accurate and under federal regulations.

Who Has to Follow the FCRA? The FCRA applies to any company that collects and sells data about you to third parties. Such companies, known as consumer reporting agencies, must follow the stipulations of the FCRA. The three most well-known consumer reporting agencies in the U.S. are Equifax, TransUnion and Experian.