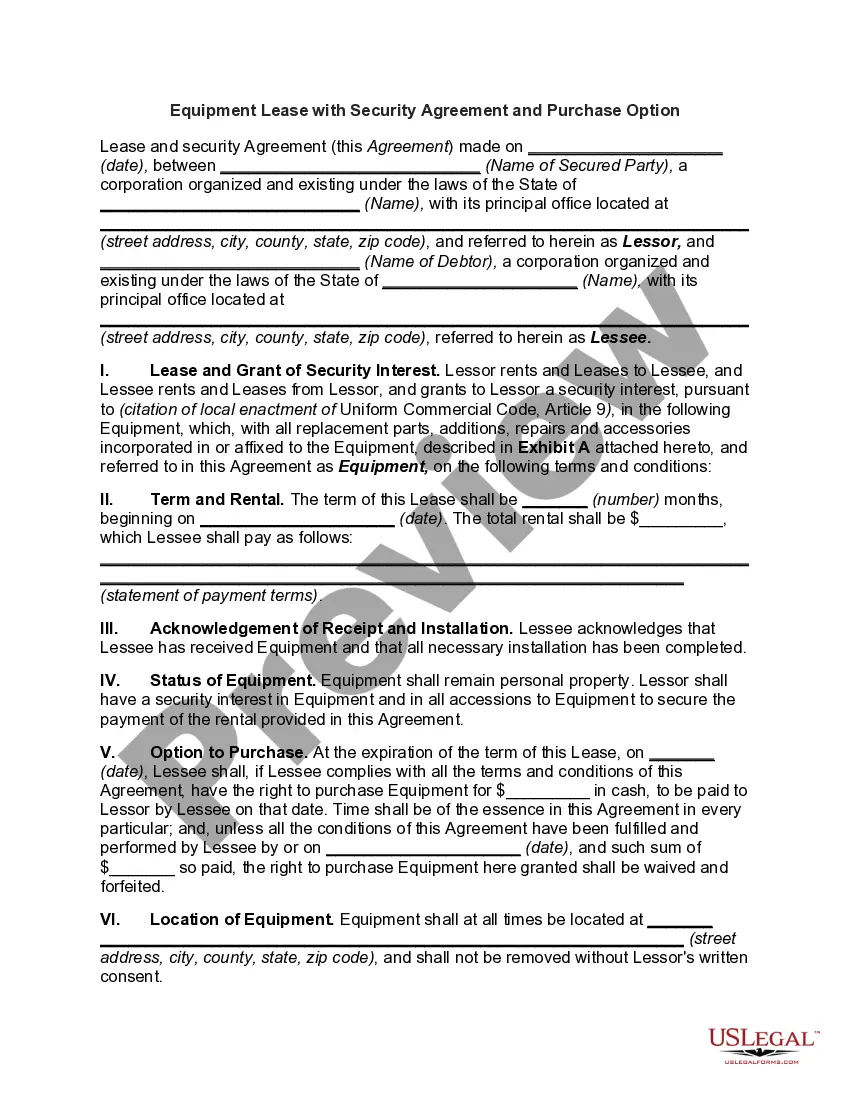

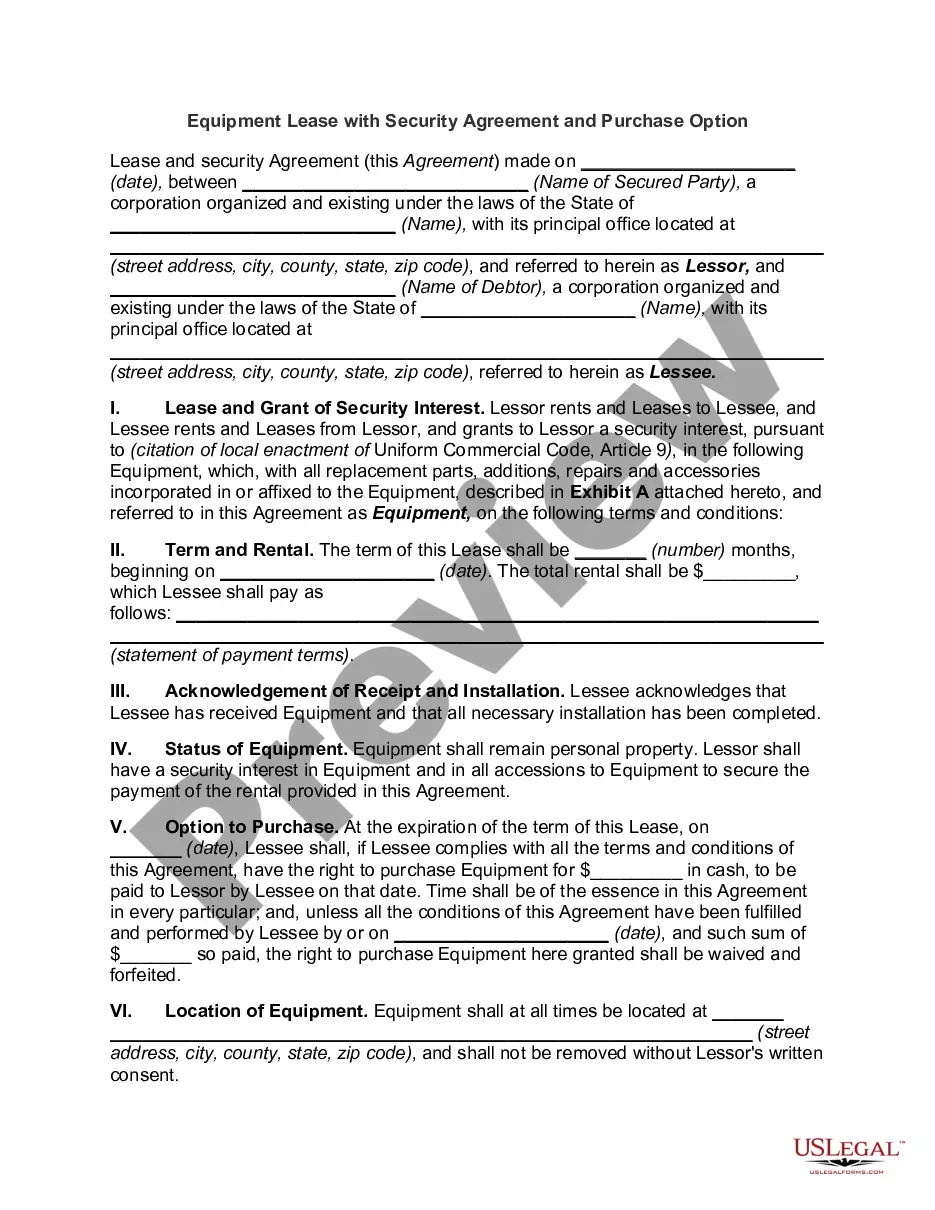

Florida Lease Purchase Agreement for Equipment

Description

How to fill out Lease Purchase Agreement For Equipment?

Have you found yourself in a situation where you need documents for potential organization or particular objectives almost every workday.

There are numerous official document templates available online, but finding trustworthy ones can be challenging.

US Legal Forms offers thousands of form templates, including the Florida Lease Purchase Agreement for Equipment, designed to meet federal and state requirements.

Once you locate the right form, click Buy now.

Select the pricing plan you want, fill in the necessary information to create your account, and complete the transaction using your PayPal or credit card.

- If you are already familiar with the US Legal Forms site and have an account, simply Log In.

- After that, you can obtain the Florida Lease Purchase Agreement for Equipment template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Retrieve the form you need and ensure it is for the correct city/state.

- Utilize the Preview button to examine the document.

- Check the summary to confirm you have selected the appropriate form.

- If the form isn't what you're looking for, employ the Search field to find the document that fits your requirements.

Form popularity

FAQ

Leasing works like a rental agreement. You pay the equipment's owner a set fee every agreed period and you can use the asset as though it was your own. Under a lease, nobody else can use the equipment without your permission and for all intents and purposes, it's as though you own the piece of equipment.

A lease will always have at least two parties: the lessor and the lessee. The lessor is the person or business that owns the equipment. The lessee is the person or business renting the equipment. The lessee will make payments to the lessor throughout the contract.

What is equipment leasing? Equipment leasing is a type of financing in which you rent equipment rather than purchase it outright. You can lease expensive equipment for your business, such as machinery, vehicles or computers.

Learn more about Equipment Leasing!Sale/Leaseback: (allows you to use your equipment to get working capital)True Lease or Operating Equipment Leases: (Also known as fair market value leases)The P.U.T. Option Lease (Purchase upon Termination)TRAC Equipment Leases.More items...

The IRS rule is that you claim depreciation on leased equipment if your contract is a lease-to-own arrangement. If it's a not-to-own lease, you deduct the payments as a regular business expense, even if the lease meets GAAP's five-fold test for a finance lease.

A $1 Buyout Lease, also called a capital lease, is similar to purchasing equipment with a loan. With this type of lease, there is a higher monthly payment compared with an FMV lease, but at the end of the lease term, the lessee purchases the equipment for $1.

It is retained by the lessor during and after the lease term and cannot contain a bargain purchase option. The term is less than 75% of the asset's estimated economic life and the present value (PV) of lease payments is less than 90% of the asset's fair market value.

A capital lease is where the company or lessee wants the equipment to appear on the balance sheet as an asset, but also wants to spread out the payments over the life of a term. The equipment leased is considered part of the company's assets (i.e., capital, hence the name).

Because they are both a form of lease, they have one thing in common. That is, the owner of the equipment (the lessor) provides to the user (the lessee) the authority to use the equipment and then returns it at the end of a set period.

A Capital Lease is treated like a purchase for tax and depreciation purposes. The leased equipment is shown as an asset and/or a liability on the lessee's balance sheet, and the tax benefits of ownership may be realized, including Section 179 deductions.