Connecticut Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

If you wish to complete, download, or printing authorized papers themes, use US Legal Forms, the largest assortment of authorized kinds, that can be found online. Make use of the site`s basic and practical lookup to discover the paperwork you need. A variety of themes for enterprise and person functions are sorted by groups and suggests, or key phrases. Use US Legal Forms to discover the Connecticut Assignment of Life Insurance as Collateral in a handful of mouse clicks.

When you are currently a US Legal Forms customer, log in in your accounts and click on the Obtain button to get the Connecticut Assignment of Life Insurance as Collateral. Also you can entry kinds you earlier acquired within the My Forms tab of your respective accounts.

If you use US Legal Forms for the first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the form to the correct metropolis/land.

- Step 2. Utilize the Review method to look over the form`s articles. Never forget about to see the description.

- Step 3. When you are unhappy using the develop, use the Look for discipline near the top of the display to locate other types of your authorized develop design.

- Step 4. Upon having identified the form you need, click on the Acquire now button. Pick the rates plan you prefer and add your credentials to sign up on an accounts.

- Step 5. Procedure the financial transaction. You can use your credit card or PayPal accounts to finish the financial transaction.

- Step 6. Choose the structure of your authorized develop and download it on your gadget.

- Step 7. Full, revise and printing or indication the Connecticut Assignment of Life Insurance as Collateral.

Every authorized papers design you get is your own for a long time. You may have acces to each develop you acquired within your acccount. Click on the My Forms segment and choose a develop to printing or download once more.

Be competitive and download, and printing the Connecticut Assignment of Life Insurance as Collateral with US Legal Forms. There are millions of professional and express-specific kinds you can use for your enterprise or person requires.

Form popularity

FAQ

If you have permanent life insurance, you may be able to use your policy's cash value as collateral to take out a loan. You can request a loan from your life insurance company for any reason, and there isn't an approval process.

Plus, life insurance proceeds are rarely taxable. Cash value policies also offer benefits while you are alive. You can use the cash value to reduce your premium payments, supplement your retirement income, pay for long-term care or cover other expenses.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

If your policy has adequate cash value, you can borrow against it with flexible repayment terms and low interest rates. Keep in mind that if you do not pay back the loan in full before you die, your death benefit will be reduced.

Using your life insurance policy as collateral is one way of securing a loan without the risk of using your home or car. Most loans are either secured or unsecured, and while an unsecured loan does not require collateral, they are not always the most affordable or available option to many loan seekers.

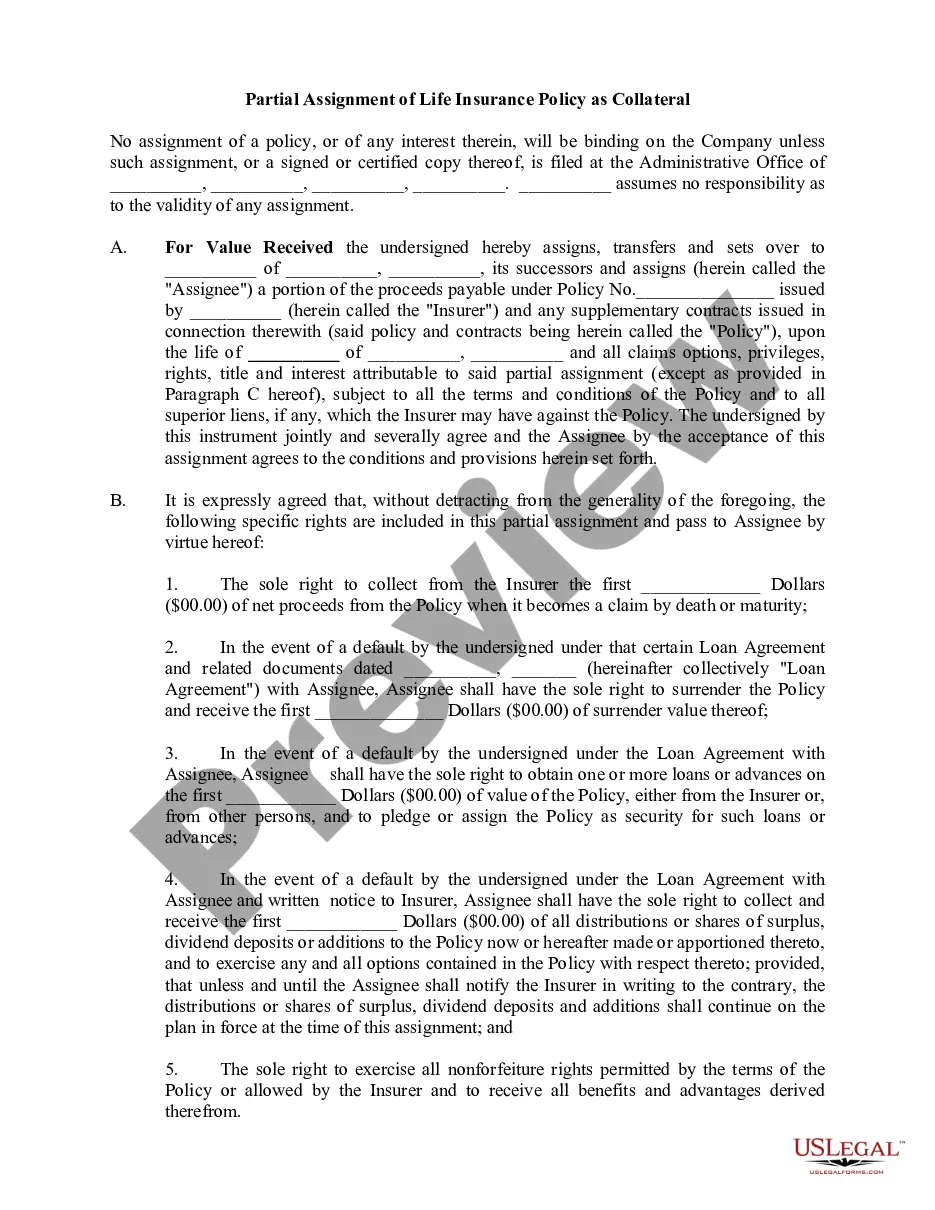

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.