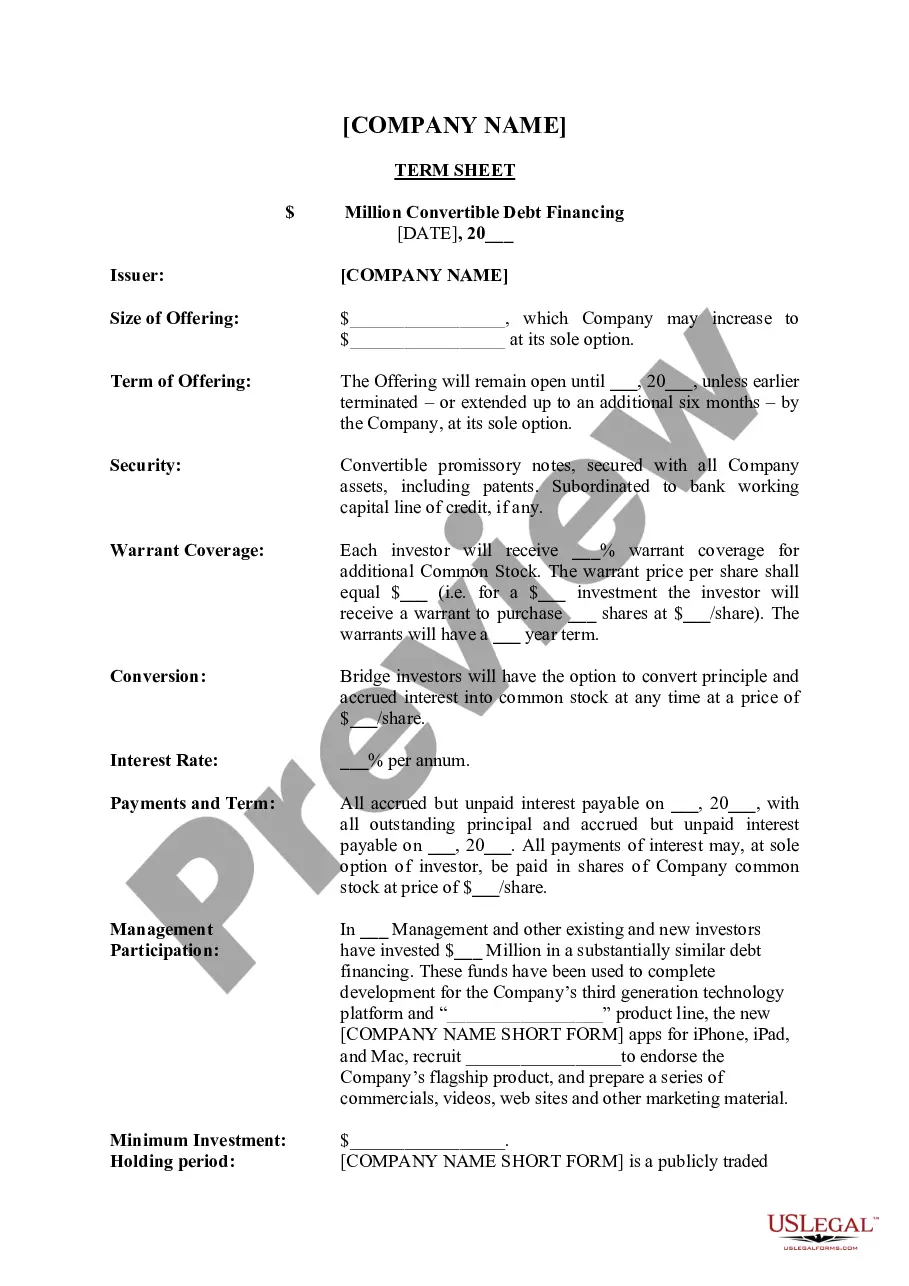

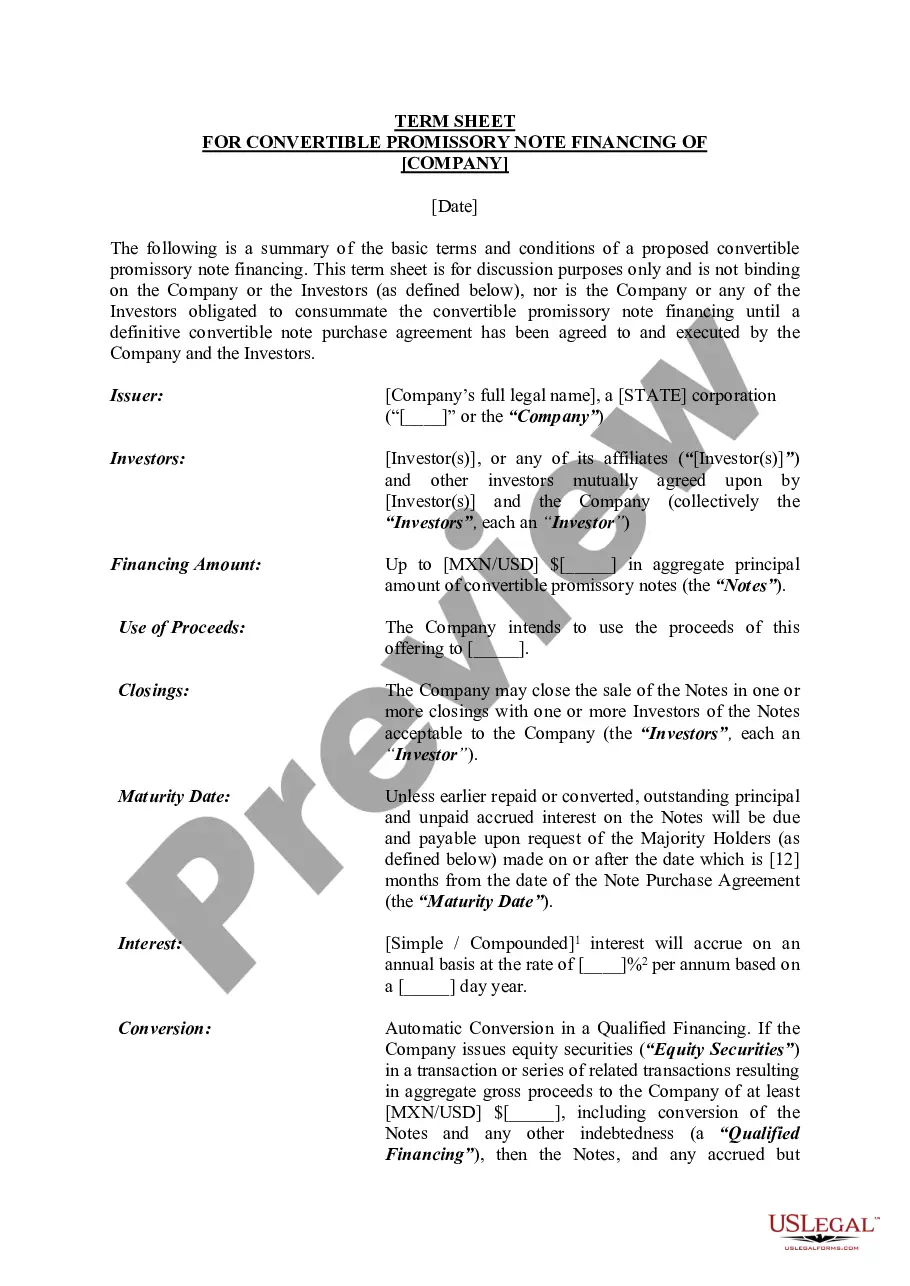

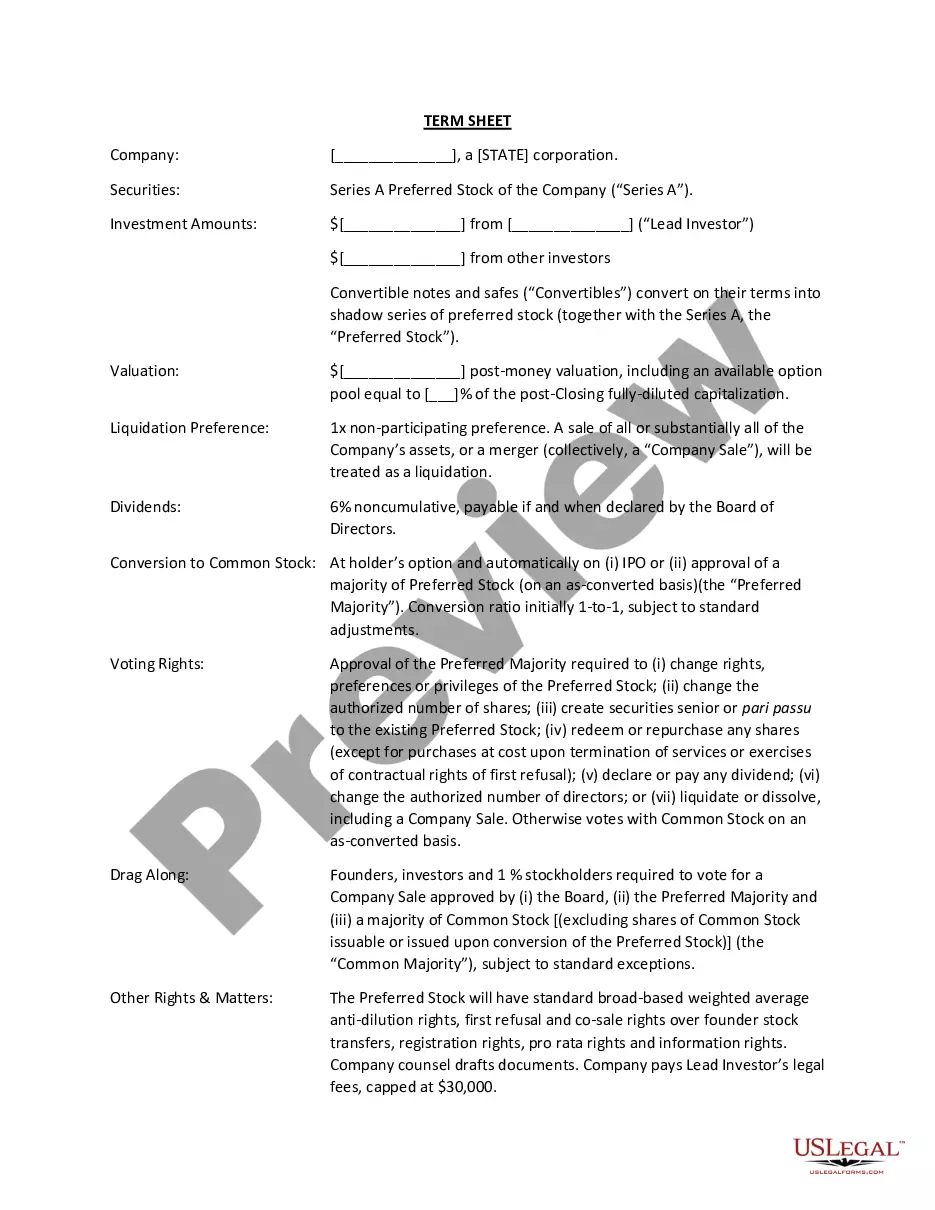

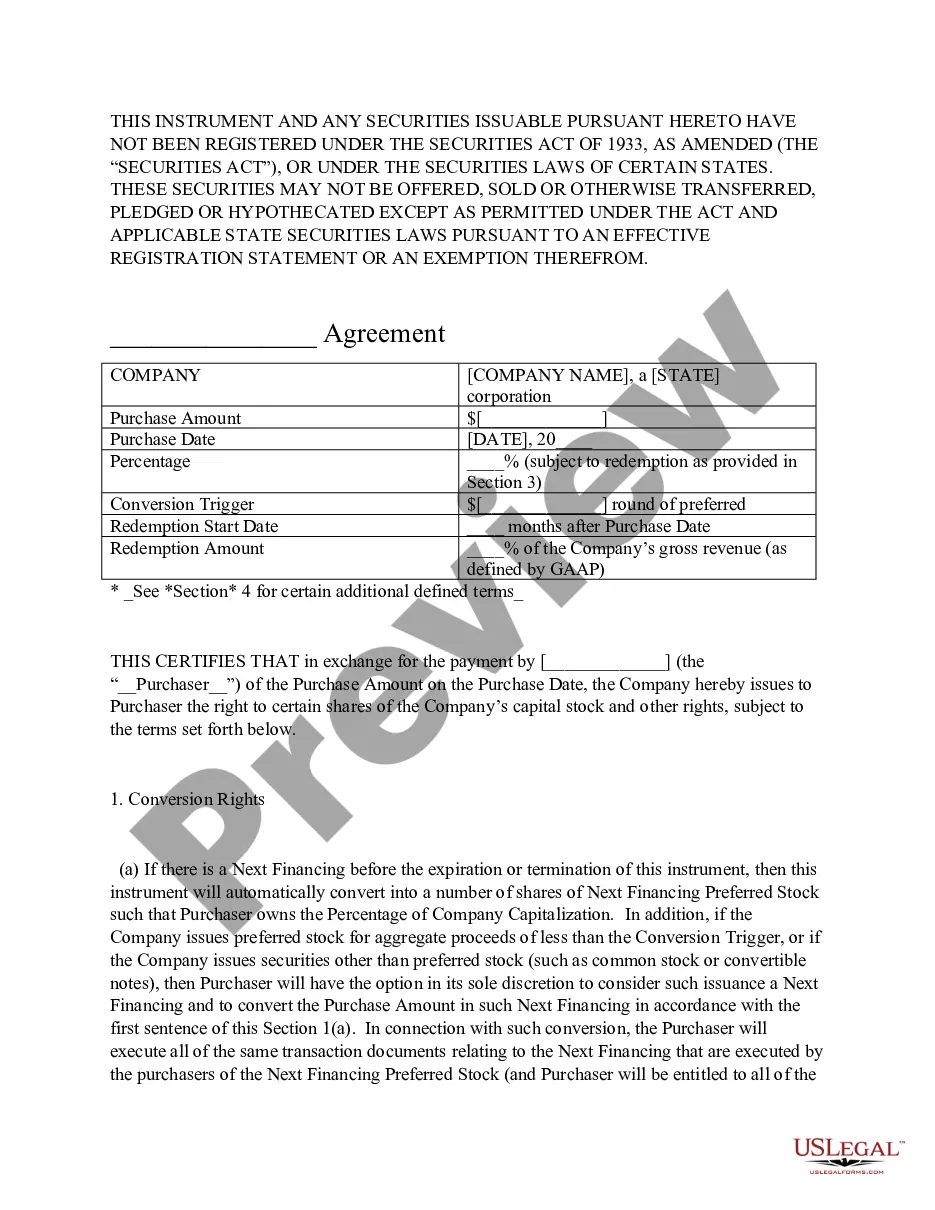

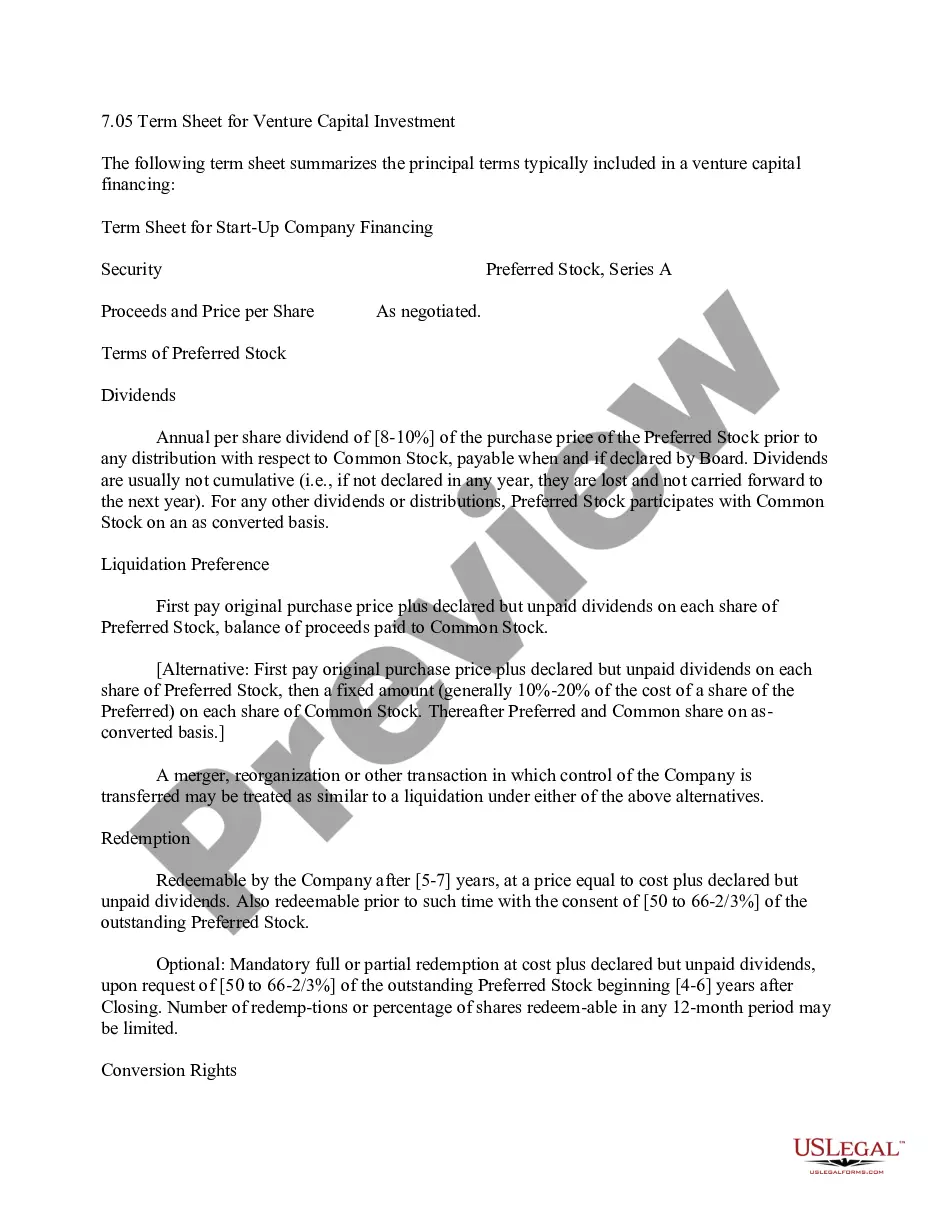

Connecticut Term Sheet - Royalty Payment Convertible Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Term Sheet - Royalty Payment Convertible Note?

You may devote several hours on the web attempting to find the lawful document format that fits the federal and state needs you require. US Legal Forms supplies 1000s of lawful varieties which can be reviewed by pros. You can actually download or printing the Connecticut Term Sheet - Royalty Payment Convertible Note from our services.

If you currently have a US Legal Forms accounts, you are able to log in and click on the Acquire option. After that, you are able to complete, edit, printing, or indicator the Connecticut Term Sheet - Royalty Payment Convertible Note. Every single lawful document format you purchase is your own property forever. To have another version for any purchased kind, proceed to the My Forms tab and click on the related option.

If you are using the US Legal Forms site the very first time, follow the basic recommendations below:

- Initially, make certain you have selected the proper document format for the county/city that you pick. Look at the kind information to ensure you have picked the correct kind. If available, take advantage of the Preview option to appear throughout the document format too.

- In order to find another edition of the kind, take advantage of the Research industry to discover the format that meets your requirements and needs.

- Once you have identified the format you need, just click Acquire now to proceed.

- Pick the prices program you need, key in your references, and register for an account on US Legal Forms.

- Full the purchase. You may use your bank card or PayPal accounts to cover the lawful kind.

- Pick the formatting of the document and download it in your system.

- Make modifications in your document if required. You may complete, edit and indicator and printing Connecticut Term Sheet - Royalty Payment Convertible Note.

Acquire and printing 1000s of document themes utilizing the US Legal Forms Internet site, which provides the biggest assortment of lawful varieties. Use specialist and status-specific themes to deal with your company or person requires.

Form popularity

FAQ

Calculating post-money valuation Post-money valuation = Pre-money valuation + Size of investment. ... Share price = New investment amount / # of new shares received. ... Post-money valuation / total # of shares post-investment = New investment amount / # of new shares received.

Although it is customary to forego a term sheet, in some cases it may be required if the parties need to negotiate certain terms. It can be advantageous to use a term sheet for the company to easily summarize the terms of the notes for potential other investors purchasing a convertible note.

A valuation cap is applied during the pre-money valuation period of an investment which is when the convertible debt becomes equity. Is a Valuation Cap Pre or Post-Money? - Westchester Angels westchesterangels.com ? is-a-valuation-cap-pre-or... westchesterangels.com ? is-a-valuation-cap-pre-or...

Convertible Notes are loans ? so they are recorded on the Balance Sheet of a company as a liability when they are made. Depending on the debt's maturity date, they can either be shown as a current liability (loans maturing within 12 months) or as a Long-term liability (loans maturing over 12 months).

Common provisions of a convertible debt financing include: The interest rate. Usually somewhere between 4% and 8%. The maturity date. Usually 12?24 months. A mandatory conversion paragraph. ... An optional conversion paragraph. ... A change of control provision. ... A conversion discount. ... A valuation cap. ... An amendment provision.

The simplest approach is to strip the equity component from the convertible note and treat the value as a sum-of-the-parts. The equity is most commonly valued in straight Black-Scholes option pricing model, and this value is deducted from the convertible note's notional amount to imply the ?value? of the straight-debt. Convertible Notes Valuation valuationresearch.com ? pure-perspectives valuationresearch.com ? pure-perspectives

The basic concept for valuing a convertible note is the same in theory as the valuation of any other financial asset. The value of the note is equal to the present value of the future income that the convertible note will receive, discounted to the present value based on its associated risk. Valuation of Convertible Notes - Eqvista eqvista.com ? resources ? valuation-of-convertible... eqvista.com ? resources ? valuation-of-convertible...

It's very easy to determine the post-money valuation. To do so, use this formula: Post-money valuation = Investment dollar amount ÷ percent investor receives. Pre-Money vs. Post-Money: What's the Difference? - Investopedia investopedia.com ? ask ? answers ? differen... investopedia.com ? ask ? answers ? differen...