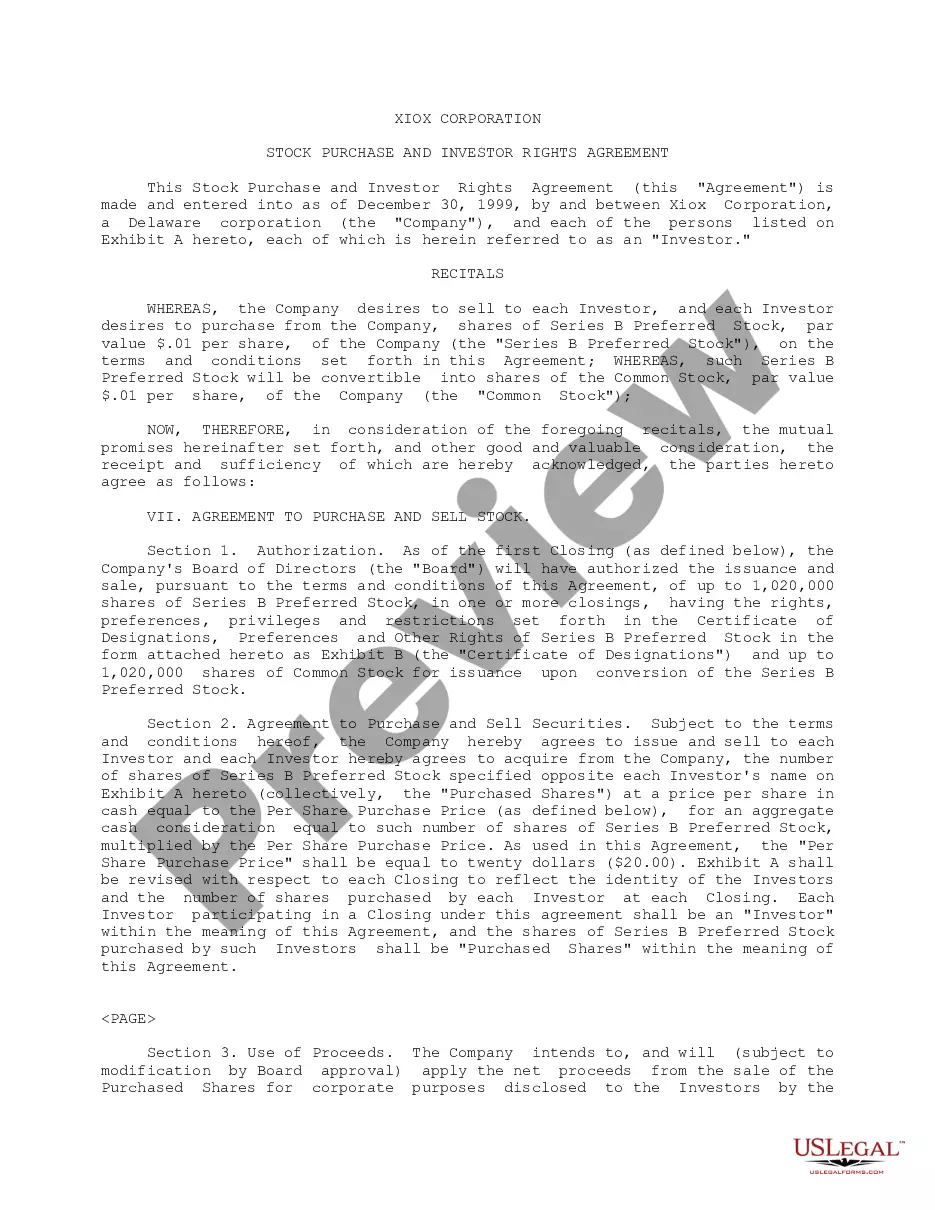

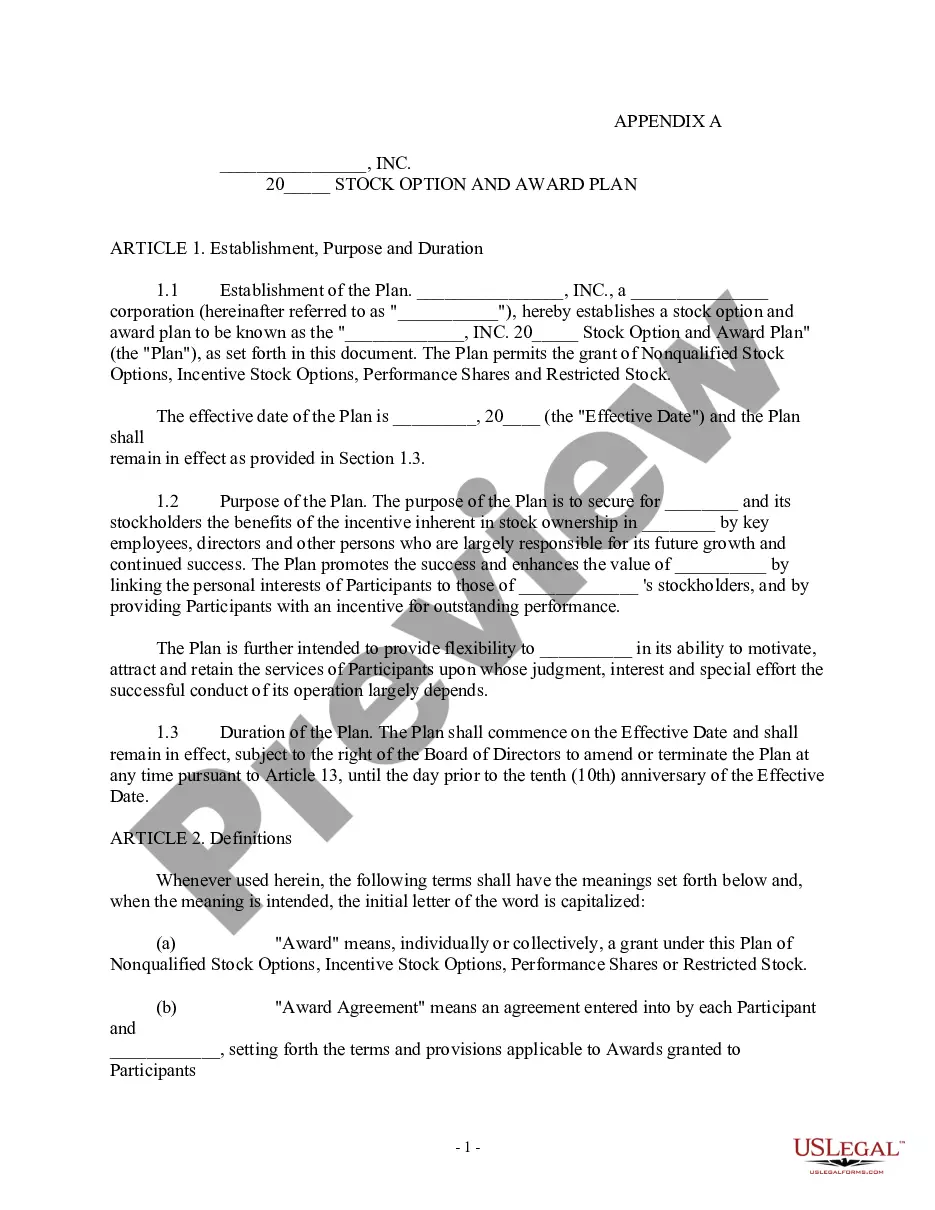

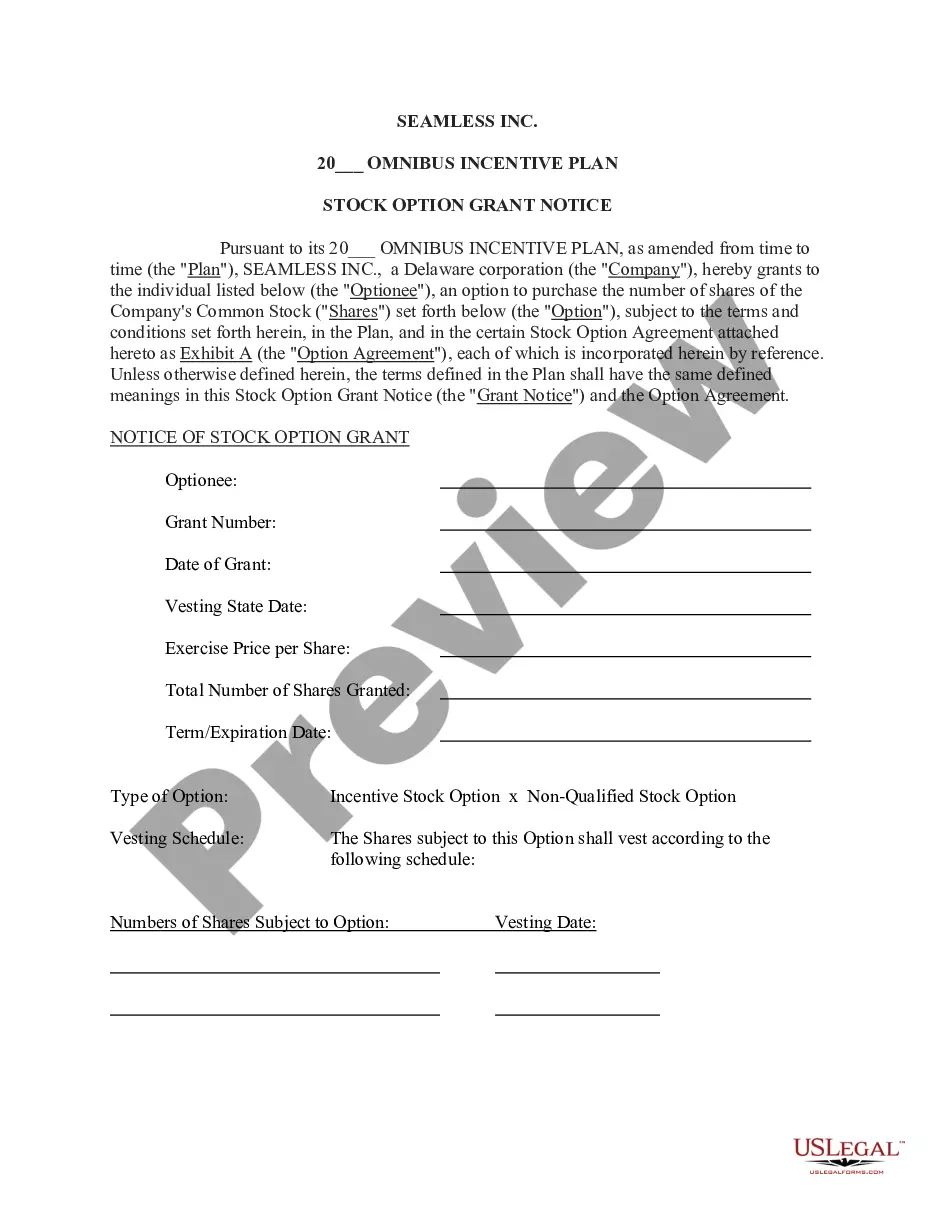

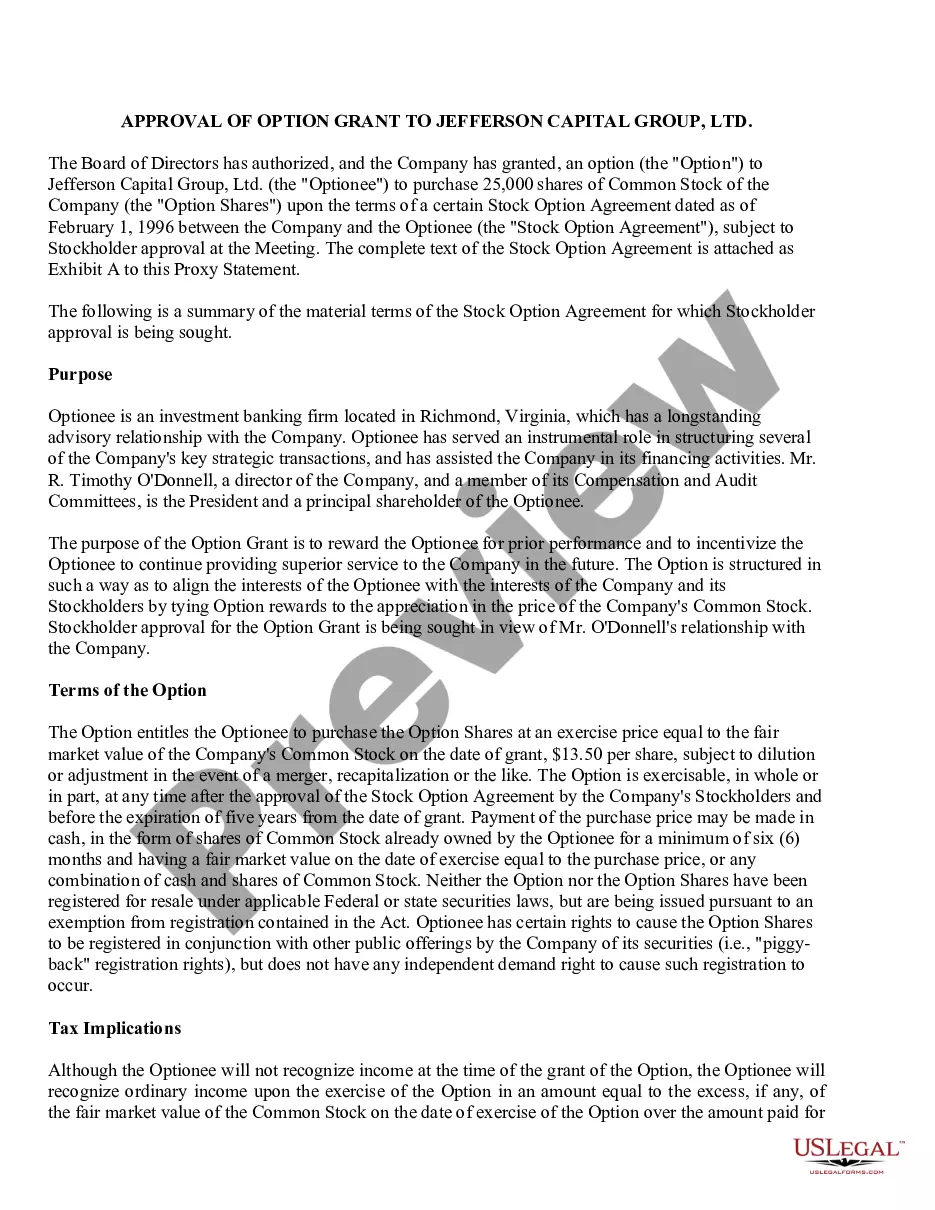

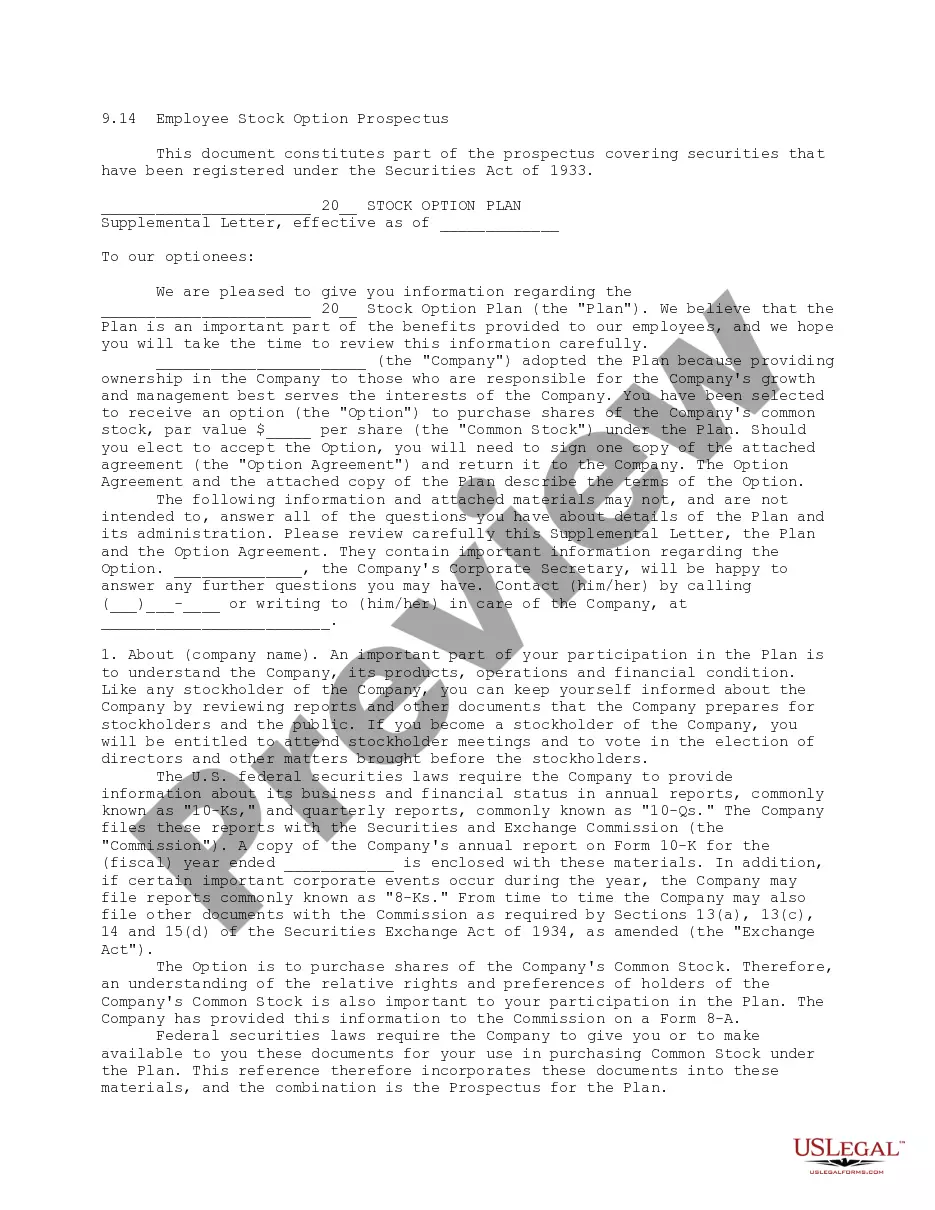

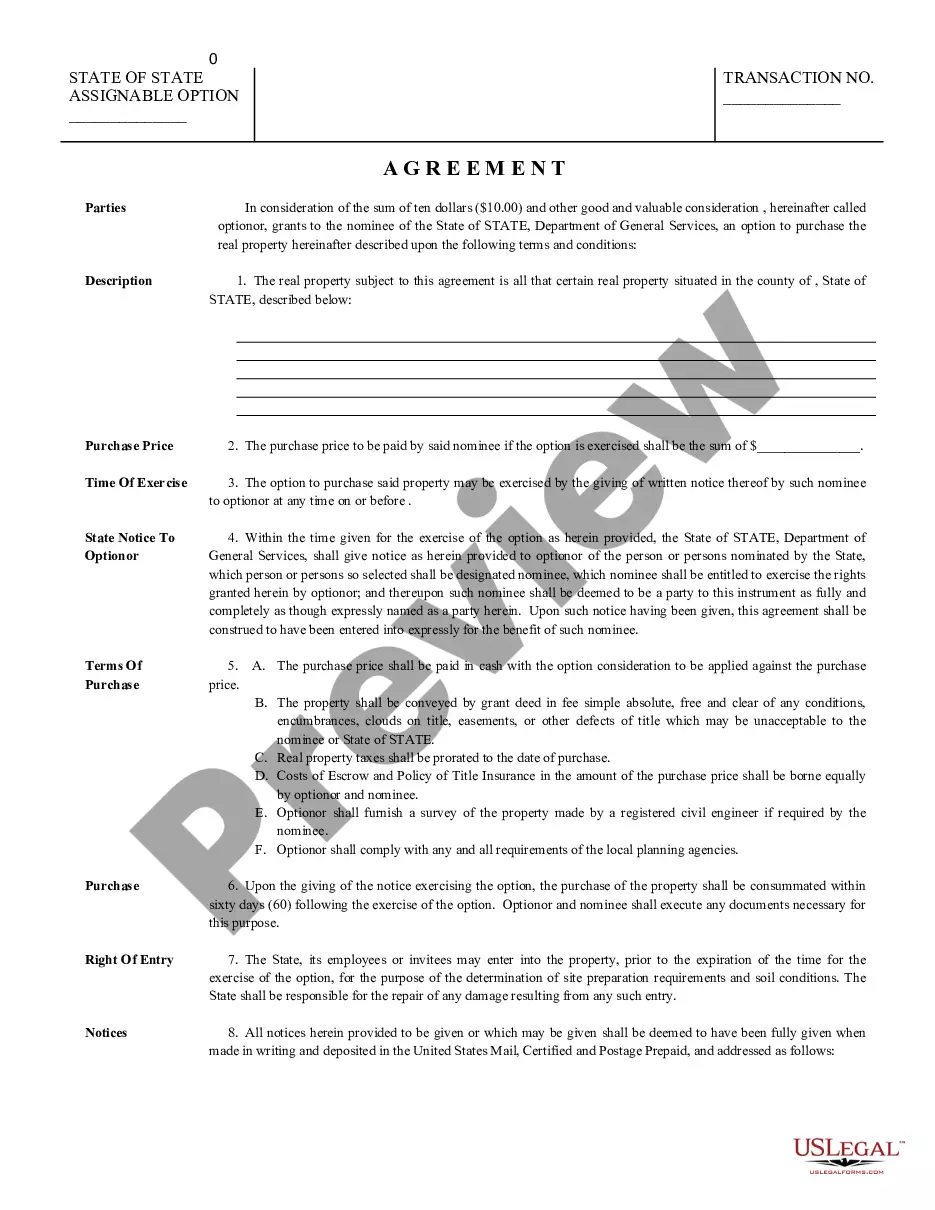

Connecticut Stock Option Grants and Exercises and Fiscal Year-End Values

Description

How to fill out Stock Option Grants And Exercises And Fiscal Year-End Values?

US Legal Forms - one of several greatest libraries of authorized kinds in America - gives a wide array of authorized record web templates it is possible to obtain or produce. Utilizing the web site, you may get thousands of kinds for business and individual functions, sorted by categories, says, or keywords.You will discover the latest models of kinds such as the Connecticut Stock Option Grants and Exercises and Fiscal Year-End Values in seconds.

If you have a subscription, log in and obtain Connecticut Stock Option Grants and Exercises and Fiscal Year-End Values in the US Legal Forms catalogue. The Down load switch will appear on each and every develop you look at. You have access to all earlier acquired kinds inside the My Forms tab of your own account.

If you want to use US Legal Forms for the first time, listed here are straightforward recommendations to get you started off:

- Be sure you have picked out the best develop for the metropolis/region. Go through the Preview switch to analyze the form`s content. Look at the develop information to actually have selected the appropriate develop.

- When the develop doesn`t match your needs, utilize the Research field on top of the display screen to get the the one that does.

- In case you are happy with the form, verify your option by simply clicking the Get now switch. Then, opt for the pricing program you prefer and give your references to sign up for the account.

- Process the financial transaction. Utilize your bank card or PayPal account to perform the financial transaction.

- Choose the file format and obtain the form on your product.

- Make adjustments. Fill out, revise and produce and indicator the acquired Connecticut Stock Option Grants and Exercises and Fiscal Year-End Values.

Each web template you put into your bank account lacks an expiration particular date and is yours permanently. So, if you would like obtain or produce one more duplicate, just go to the My Forms portion and click on on the develop you require.

Obtain access to the Connecticut Stock Option Grants and Exercises and Fiscal Year-End Values with US Legal Forms, one of the most substantial catalogue of authorized record web templates. Use thousands of skilled and state-specific web templates that meet up with your business or individual requirements and needs.

Form popularity

FAQ

You can calculate the aggregate exercise price by taking the strike price of the option and multiplying it by its contract size. In the case of a bond option, the exercise price is multiplied by the face value of the underlying bond.

Every stock option has an exercise price, also called the strike price, which is the price at which a share can be bought. In the US, the exercise price is typically set at the fair market value of the underlying stock as of the date the option is granted, in order to comply with certain requirements under US tax law.

Exercise Price ? Also known as the strike price, the grant price is the price at which you can buy the shares of stock. Regardless of the future value of that particular stock, the option holder will have the right to buy the shares at the grant price rather than the current, actual price.

You have taxable income or deductible loss when you sell the stock you bought by exercising the option. You generally treat this amount as a capital gain or loss. However, if you don't meet special holding period requirements, you'll have to treat income from the sale as ordinary income.

If this amount is not included in Box 1 of Form W-2, you still must add it to the amount of compensation income that you report on your 2023 Form 1040, line 7. You also must report the sale of the stock on your 2023 Schedule D, Part II as a long-term sale.

Both call and put options have an exercise price. Investors also refer to the exercise price as the strike price. The difference between the exercise price and the underlying security's price determines if an option is ?in the money? or ?out of the money."

Exercising a stock option means purchasing the issuer's common stock at the price set by the option (grant price), regardless of the stock's price at the time you exercise the option.

A strike price, also known as a grant price or exercise price, is the fixed cost that you'll pay per share in order to exercise your stock options so you can own them.