The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

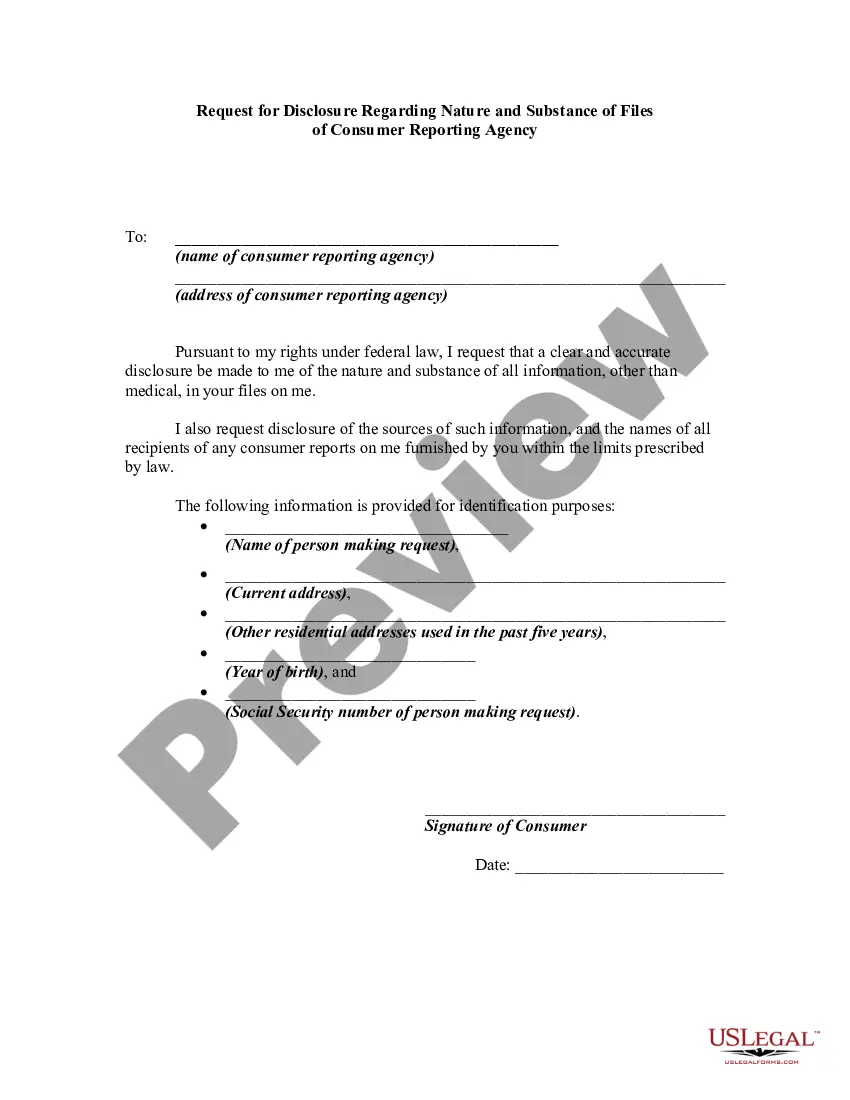

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

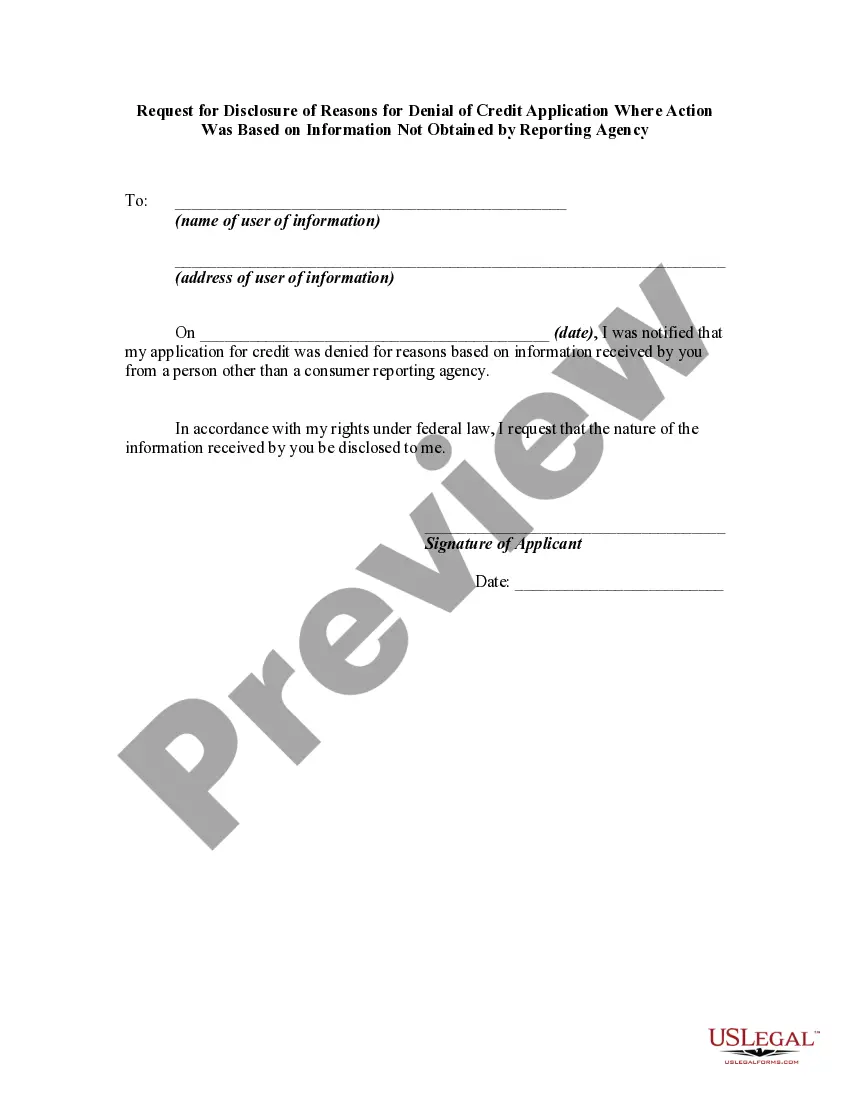

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

California Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Increasing Charge For Credit Regarding Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

Are you presently in the position the place you require paperwork for possibly organization or specific uses almost every time? There are a variety of authorized record web templates available online, but discovering types you can trust is not straightforward. US Legal Forms offers a huge number of develop web templates, much like the California Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency, which are written to satisfy federal and state needs.

When you are previously informed about US Legal Forms internet site and get a merchant account, merely log in. Following that, you are able to down load the California Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency design.

Should you not have an accounts and would like to start using US Legal Forms, abide by these steps:

- Get the develop you want and ensure it is for your appropriate area/region.

- Use the Preview key to analyze the form.

- See the information to actually have chosen the proper develop.

- If the develop is not what you`re trying to find, utilize the Research area to obtain the develop that meets your needs and needs.

- Once you find the appropriate develop, click on Purchase now.

- Select the prices program you need, submit the necessary details to create your bank account, and purchase the order using your PayPal or bank card.

- Choose a convenient file formatting and down load your duplicate.

Find all the record web templates you may have bought in the My Forms menu. You can aquire a further duplicate of California Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency any time, if necessary. Just click the needed develop to down load or print the record design.

Use US Legal Forms, one of the most considerable selection of authorized types, to save lots of time and avoid faults. The support offers expertly created authorized record web templates which you can use for an array of uses. Produce a merchant account on US Legal Forms and begin generating your lifestyle a little easier.

Form popularity

FAQ

Under the Fair Credit Reporting Act (FCRA), creditors, lenders, and other businesses must send you an adverse action notice in these scenarios: Your credit application is denied. You are not extended credit in the amount or terms you wanted.

If you deny a consumer credit based on information in a consumer report, you must provide an ?adverse action? notice to the consumer.

The Fair Credit Reporting Act (FCRA) mandates that when a business pulls a credit report on someone, they must specify the reason, such as: In conjunction with a loan request. For employment purposes.

A furlough of 30 days or less (which typically occurs for budgetary reasons) is also conducted under the rules for adverse actions. However, a longer furlough, removal due to a reduction in force (RIF), or demotion due to a RIF is not an ?adverse action? and is conducted under the rules set forth in 5 C.F.R. part 351.

The Consumer Credit Reporting Agencies Act (?CCRAA?) (California Civil Code § 1785.1 et seq.) allows a credit reporting agency to provide an employer with a consumer credit report, which is a report containing information about ?a consumer's credit worthiness, credit standing, or credit capacity.?

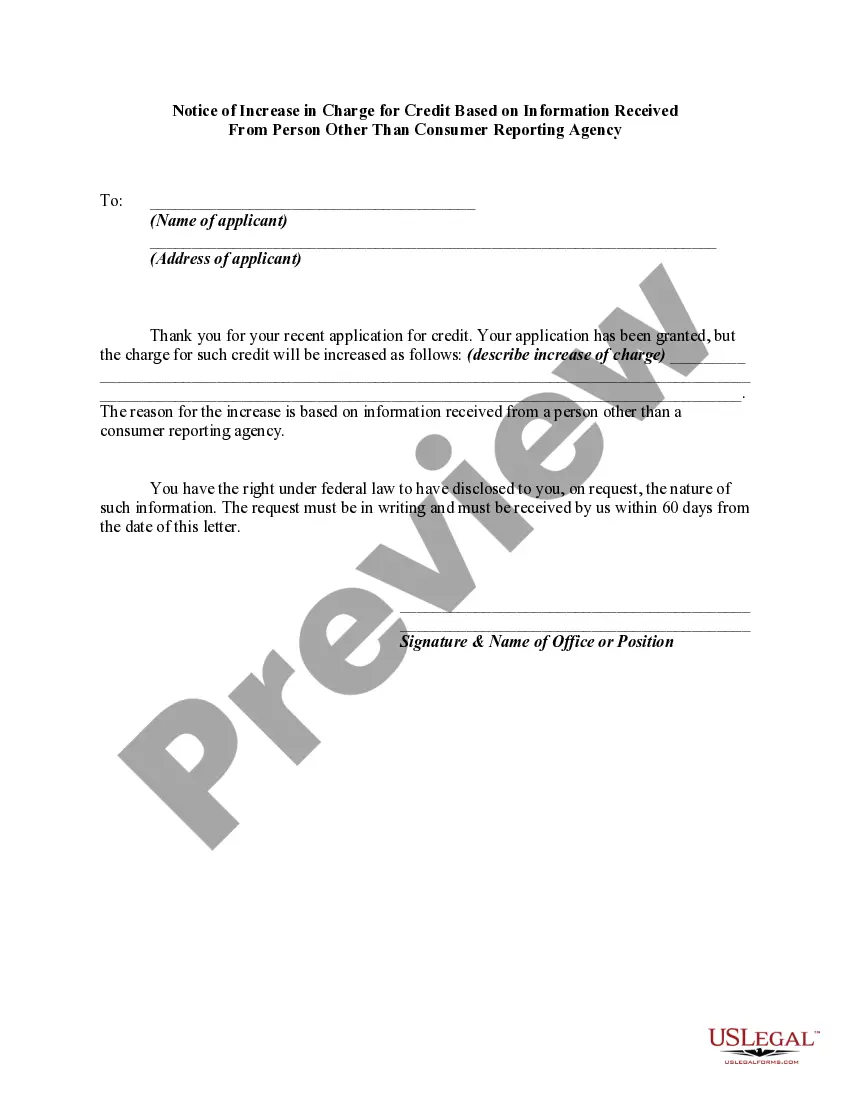

The credit score exception notice (model forms H-3, H-4, H-5) is a disclosure that is provided in lieu of the risk-based-pricing notice (RBPN, which are H-1, H-2, H-6 & H-7). The RBPN is required any time a financial institution provides different rates based on the credit score of the applicant.

If your customer accepts any credit offer and you're able to seal the deal, an adverse action notice is not needed. And don't count on the lender to send an adverse action notice?they have their own set of rules, and a notice from them does not eliminate any obligations your dealership has to the consumer.

Notice is not required if: The transaction does not involve credit; A credit applicant accepts a counteroffer; A credit applicant expressly withdraws an application; or.