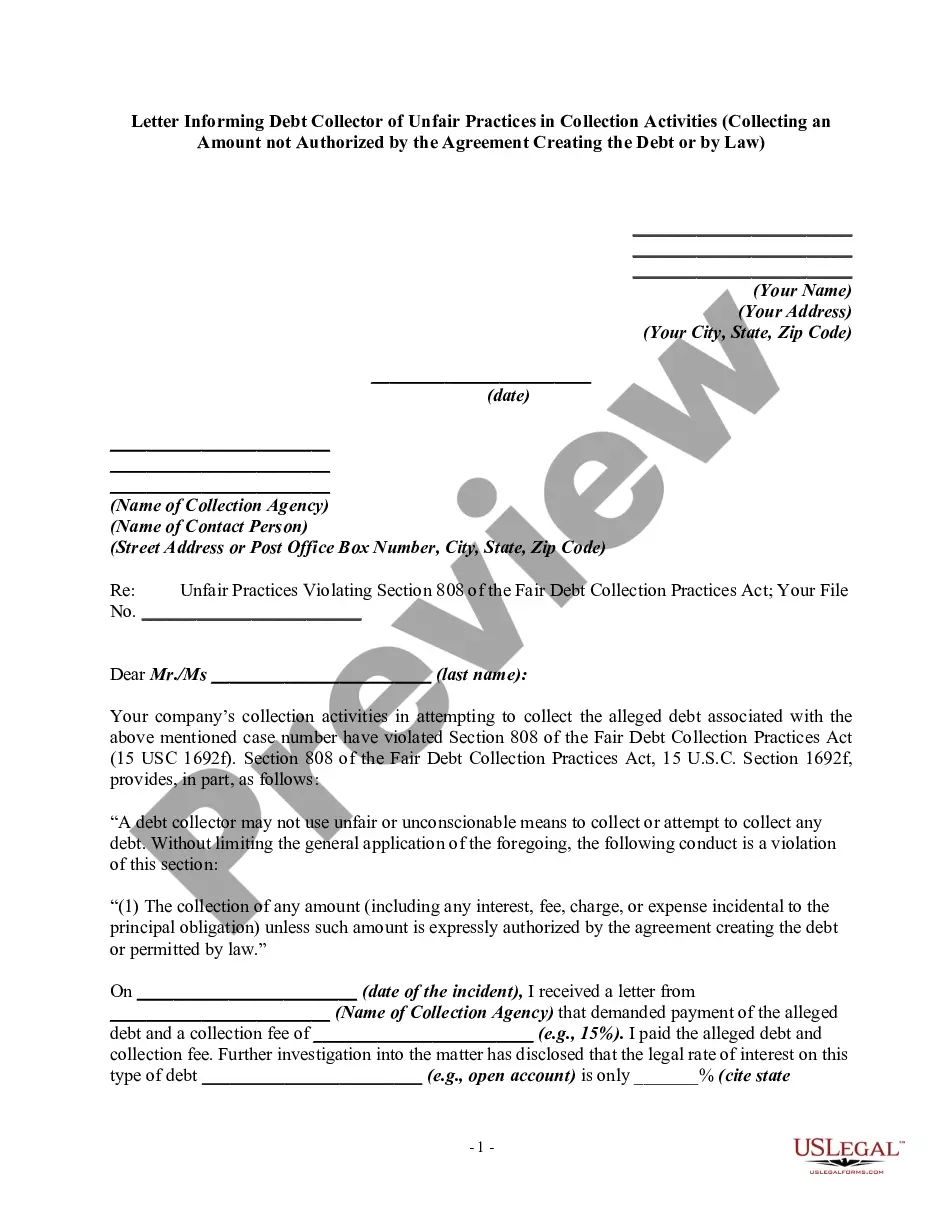

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Arizona Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

US Legal Forms - one of the most extensive collections of legal documents in the USA - provides a broad selection of legal document templates that you can obtain or create.

By utilizing the website, you can access thousands of forms for business and personal purposes, categorized by types, states, or keywords.

You can find the latest versions of documents such as the Arizona Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law in just minutes.

If the form does not meet your needs, use the Search bar at the top of the page to find one that does.

When you are satisfied with the form, confirm your choice by selecting the Get now button. Then, choose the pricing plan you prefer and provide your details to register for the account.

- If you already have a subscription, Log In and obtain the Arizona Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law from the US Legal Forms library.

- The Download button will appear on every form you view.

- You can access all previously downloaded forms in the My documents section of your account.

- If you are using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the correct form for your region/area.

- Click the Review button to verify the content of the form.

Form popularity

FAQ

While a debt validation letter provides information about the debt the collection agency claims you owe, a verification letter must prove it. In other words, if the collection agency doesn't have enough evidence to prove you owe it, their hands may be tied.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Debt collectors can ONLY withdraw funds from your bank account with YOUR permission. That permission often comes in the form of authorization for the creditor to complete automatic withdrawals from your bank account.

You are not obliged let a debt collector into your home and they don't have the right to take goods away. It's very important to understand that a debt collector is not the same as an enforcement agent or bailiff. Debt collectors have no special legal powers.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

Can a Debt Collector Take Money From Your Account Without Permission? Usually, a debt collector must obtain a court order before accessing your bank account. However, certain federal agencies, including the IRS, may be able to access your bank account without permission from a court.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Repeated calls. Threats of violence. Publishing information about you. Abusive or obscene language.