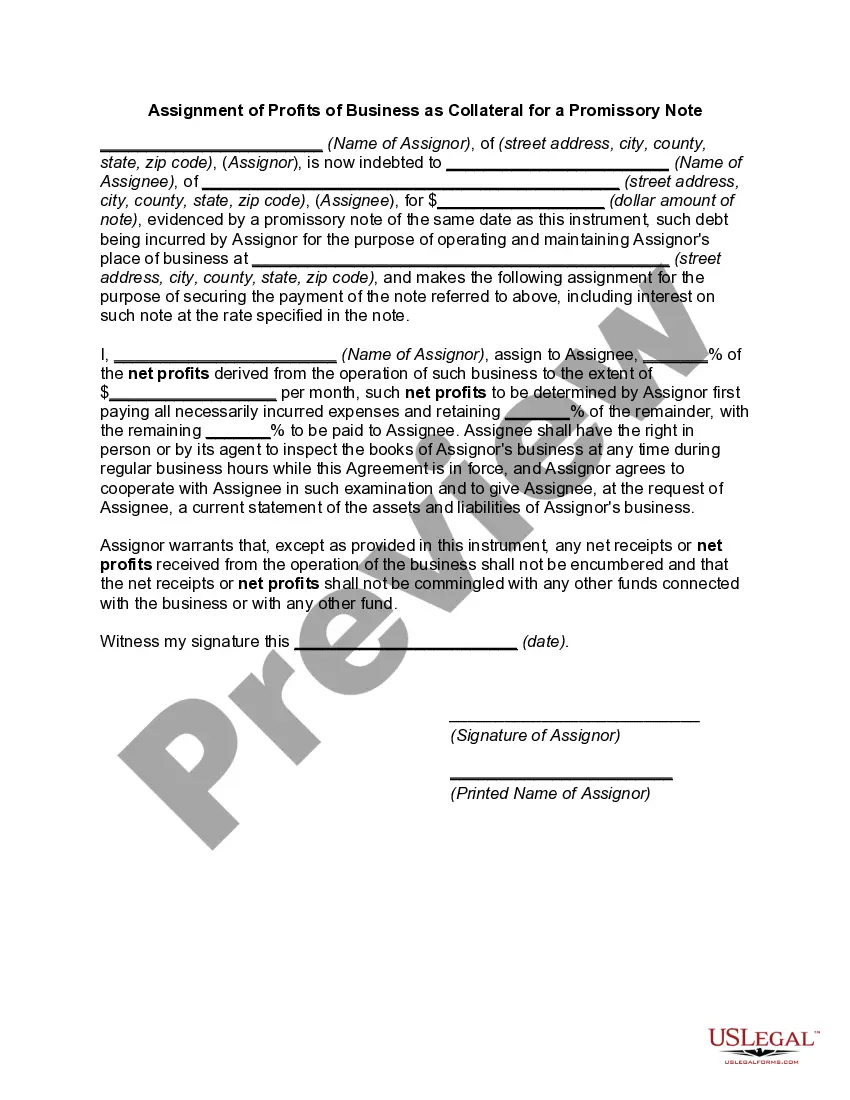

Arizona Assignment of Profits of Business

Description

How to fill out Assignment Of Profits Of Business?

Locating the appropriate legal document template could pose a challenge.

Of course, there are numerous formats available online, but how can you find the legal template you require.

Utilize the US Legal Forms website. The platform offers a vast selection of templates, such as the Arizona Assignment of Profits of Business, which can be utilized for both business and personal needs.

You can preview the form using the Preview button and read the form description to confirm it is suitable for you.

- All the documents are verified by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click on the Download button to get the Arizona Assignment of Profits of Business.

- Use your account to review the legal documents you have previously ordered.

- Navigate to the My documents tab in your account to download another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple steps for you to follow.

- First, ensure you have chosen the correct form for your jurisdiction.

Form popularity

FAQ

To request a 1099-G form in Arizona, visit the Arizona Department of Economic Security website. You can typically view and download this form directly online or request it through their contact options. This form is necessary for reporting certain types of income, including that associated with the Arizona Assignment of Profits of Business.

Employee or Employer Out-of-State Withholding (Remote Worker) Withholding of Arizona state income tax from the commencement of employment is required for any resident employee physically working in the state of Arizona regardless of where the employer is based.

Apportioned revenue is the label applied to income that is only partially subject to taxes. For example, the daily income of a retail store is apportioned revenue. Before determining the taxable revenue, the shop owner first subtracts his operating expenses and depreciation on equipment.

In most cases, state withholding applies to state residents only. In Maine, Massachusetts, Montana, Nebraska, Oregon, and Wisconsin, state withholding also applies to individuals required to file a state tax return in that state.

Nonresidents are subject to Arizona tax on any income earned from Arizona sources. Nonresidents may also exclude income Arizona law does not tax. Individuals subject to tax by both Arizona and another state on the same income may also be eligible for a tax credit.

Apportionment is the determination of the percentage of a business' profits subject to a given jurisdiction's corporate income or other business taxes. U.S. states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders.

All business income of each trade or business of the taxpayer shall be apportioned to this state by use of the apportionment formula in A.R.S. § 43-1139. The elements of the apportionment formula are the property factor, the payroll factor, and the sales factor of the trade or business of the taxpayer.

An employer must withhold Arizona tax from wages paid for services performed within the state regardless of whether the employee is a resident or nonresident.

The employee can submit a Form A-4 for a minimum withholding of 0.8% of the amount withheld for state income tax. An employee required to have 0.8% deducted may elect to increase this rate to 1.3%, 1.8%, 2.7%, 3.6%, 4.2%, or 5.1% by submitting a Form A-4. The $15,000 annual wages threshold has been removed.

To keep your withholding the same as last year, choose a withholding percentage of 1.8% (40,000 x . 018 = 720) and withhold an additional $10.77 per biweekly pay period (1,000 - 720 = 280 / 26 = 10.77). Be sure to take into account any amount already withheld for this year.