The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

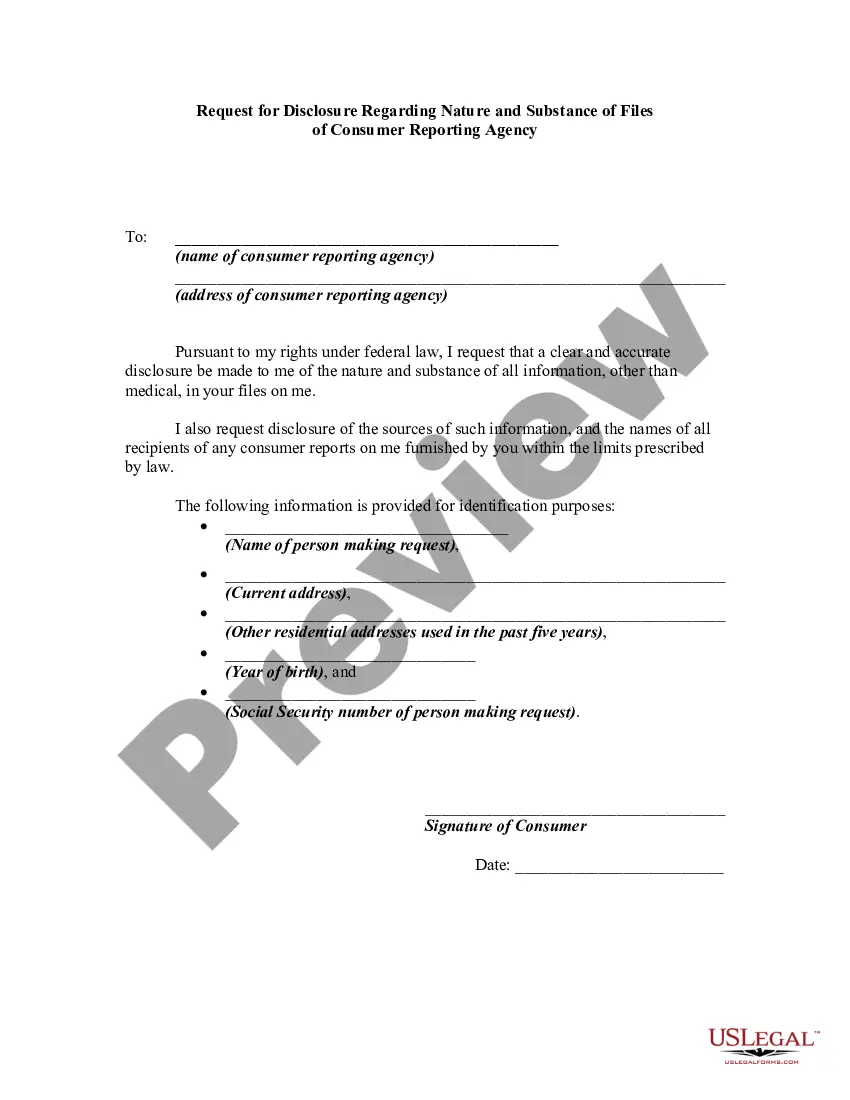

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

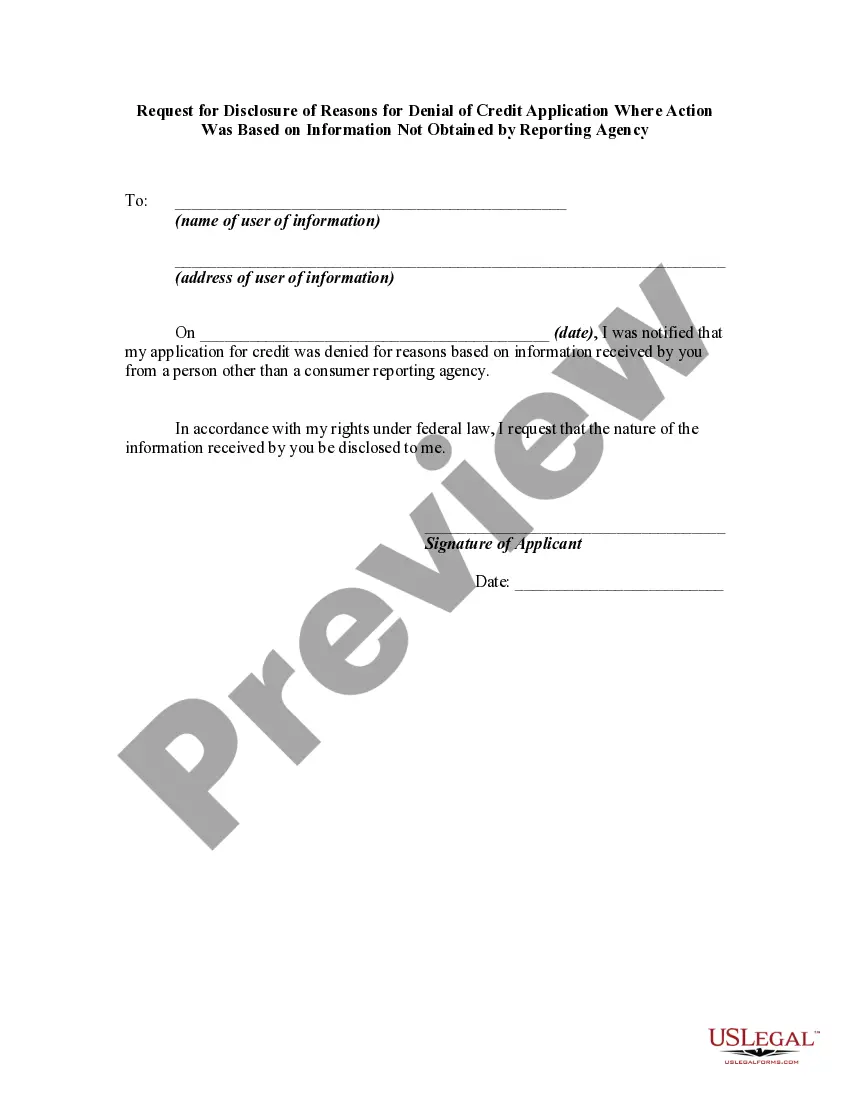

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

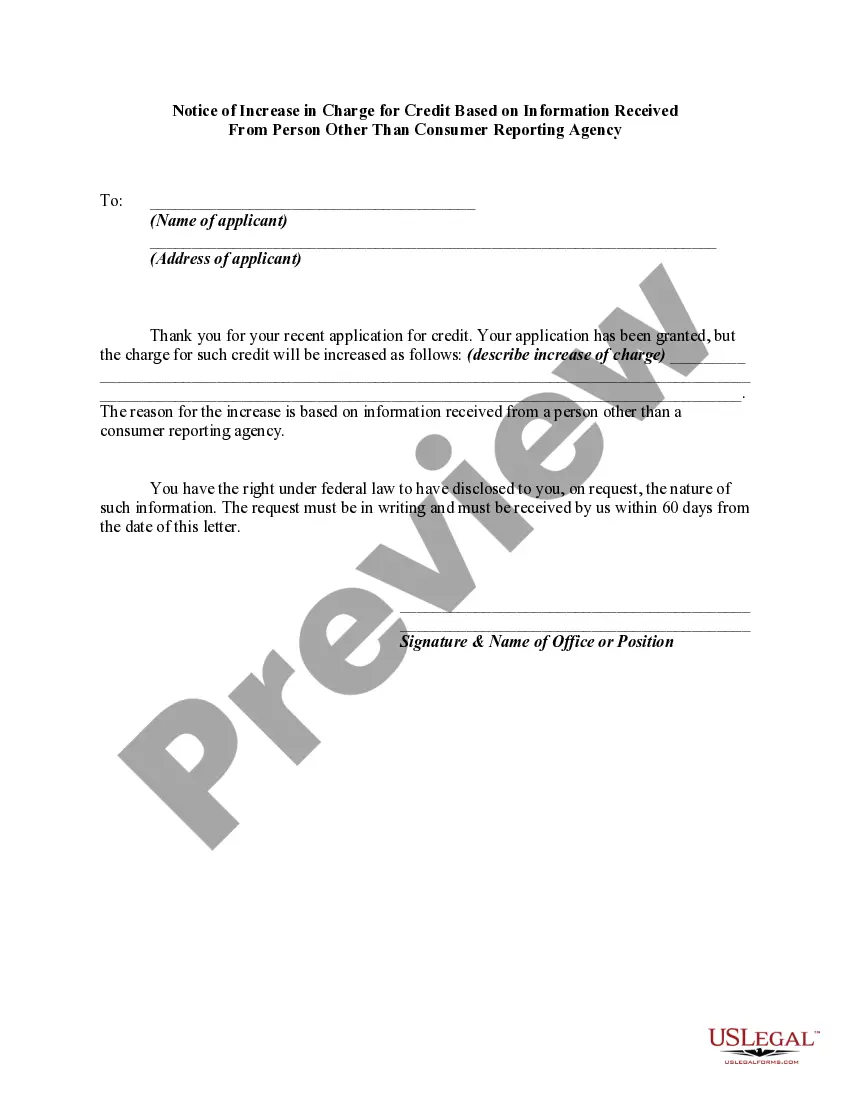

Arizona Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Increasing Charge For Credit Regarding Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

Are you presently in the position in which you require paperwork for both enterprise or personal functions almost every working day? There are tons of legitimate document themes available on the Internet, but discovering kinds you can rely on isn`t easy. US Legal Forms provides a huge number of develop themes, just like the Arizona Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency, that are published to satisfy state and federal demands.

Should you be already informed about US Legal Forms web site and also have an account, just log in. Following that, you are able to down load the Arizona Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency template.

Unless you offer an accounts and wish to begin to use US Legal Forms, follow these steps:

- Find the develop you want and ensure it is for your proper town/area.

- Use the Review key to check the form.

- Look at the description to actually have selected the appropriate develop.

- When the develop isn`t what you`re looking for, make use of the Lookup area to discover the develop that meets your needs and demands.

- When you get the proper develop, click Get now.

- Choose the rates prepare you would like, submit the required information and facts to make your bank account, and pay money for an order making use of your PayPal or Visa or Mastercard.

- Decide on a hassle-free document file format and down load your version.

Discover all the document themes you have purchased in the My Forms menu. You may get a further version of Arizona Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency anytime, if needed. Just click the necessary develop to down load or printing the document template.

Use US Legal Forms, by far the most substantial variety of legitimate types, to conserve some time and steer clear of blunders. The service provides appropriately produced legitimate document themes that can be used for a selection of functions. Make an account on US Legal Forms and start producing your lifestyle a little easier.

Form popularity

FAQ

It may also include employment information, present and previous addresses, whether they have ever filed for bankruptcy or owe child support, and any arrest record. In some, but not all, instances, consumers must have initiated a transaction or agreed in writing before the credit bureau can release their report. How the Fair Credit Reporting Act (FCRA) Protects Consumer Rights investopedia.com ? terms ? fair-credit-report... investopedia.com ? terms ? fair-credit-report...

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

In conducting any reinvestigation under paragraph (1) with respect to disputed information in the file of any consumer, the consumer reporting agency shall review and consider all relevant information submitted by the consumer in the period described in paragraph (1)(A) with respect to such disputed information. 15 U.S. Code § 1681i - Procedure in case of disputed accuracy cornell.edu ? uscode ? text cornell.edu ? uscode ? text

You must provide the notice either before you furnish the negative information or within 30 days of furnishing it. You may include the notice with a notice of default, a billing statement, or another item sent to the consumer, but you cannot send it with a Truth In Lending Act notification.

The Dodd-Frank Act also amended FCRA to require disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing. On December 21, 2011, CFPB restated FCRA regulations, named Regulation V (12 CFR Part 1022). Fair Credit Reporting Act (Regulation V) - NCUA ncua.gov ? manuals-guides ? lending-regulations ncua.gov ? manuals-guides ? lending-regulations

The notice described in paragraph (f)(1)(iii) of this section must be provided to the consumer as soon as reasonably practicable after the person has requested the credit score, but in any event not later than consummation of a transaction in the case of closed-end credit or when the first transaction is made under an ...

If you deny a consumer credit based on information in a consumer report, you must provide an ?adverse action? notice to the consumer.

Common violations of the FCRA include: Creditors give reporting agencies inaccurate financial information about you. Reporting agencies mixing up one person's information with another's because of similar (or same) name or social security number. Fair Credit Reporting Act of 1970: Common Violations and Your Rights incharge.org ? credit-score-and-credit-report incharge.org ? credit-score-and-credit-report