Arizona Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Balloon Secured Note Addendum And Rider To Mortgage, Deed Of Trust Or Security Agreement?

Selecting the appropriate authorized document template can be quite a challenge. Obviously, there are many templates available on the web, but how do you find the legal form you need? Use the US Legal Forms website. The service offers a vast array of templates, including the Arizona Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement, which can be utilized for business and personal purposes. All forms are reviewed by professionals and comply with federal and state requirements.

If you are already registered, Log In to your account and click the Acquire button to obtain the Arizona Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement. Use your account to access the legal forms you may have purchased previously. Go to the My documents tab in your account and retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions for you to follow: First, make sure you have selected the correct form for your city/state. You can browse the form using the Preview button and read the form description to ensure this is the right choice for you. If the form does not satisfy your needs, use the Search field to locate the correct form. Once you are confident that the form is suitable, click the Buy now button to obtain the form. Choose the pricing plan you prefer and enter the required information. Create your account and pay for the transaction using your PayPal account or credit card. Select the document format and download the authorized document template to your device. Complete, edit, print, and sign the acquired Arizona Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement.

US Legal Forms is indeed the largest repository of legal forms where you can find a variety of document templates.

- Utilize the service to download professionally-crafted paperwork that adhere to state requirements.

- Access a wide range of document templates available at your fingertips.

- Ensure compliance with legal standards through expertly reviewed forms.

- Retrieve previously purchased forms easily through your account.

- Follow simple steps for new users to successfully obtain the necessary documents.

- Select the appropriate format for your specific needs.

Form popularity

FAQ

Cons of balloon payments Unsecured loans with balloon payments usually have a higher interest rate than conventional loans. Paying that large balloon payment at the end of the loan may be financially difficult for your business.

One of the most common ways to handle a balloon payment is to simply refinance the loan. The new loan pays the balloon payment, and you're either left with a fully amortizing loan ? with no balloon involved ? or at least a completely new timeline.

One way out of a balloon payment is to refinance the loan to another mortgage before the balloon payment is due. Most lenders require minimum amounts of home equity to refinance a mortgage, however, so this might not be in reach ? those low initial monthly payments may not have helped you build enough equity.

There are also some risks associated with balloon mortgages, including defaulting on the loan if you're unable to make the balloon payment at the end of the loan term. In such cases, your lender will likely take steps to foreclose on your home.

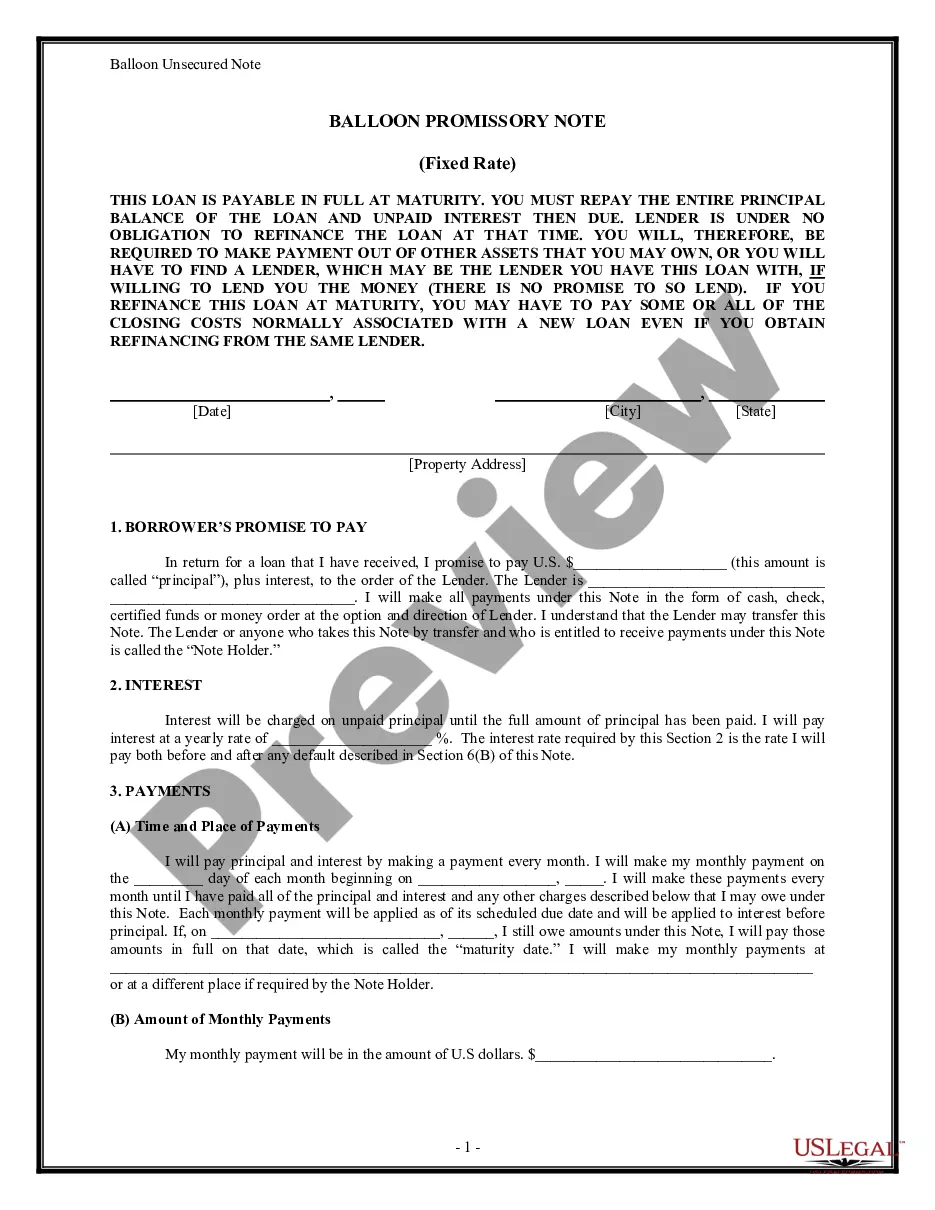

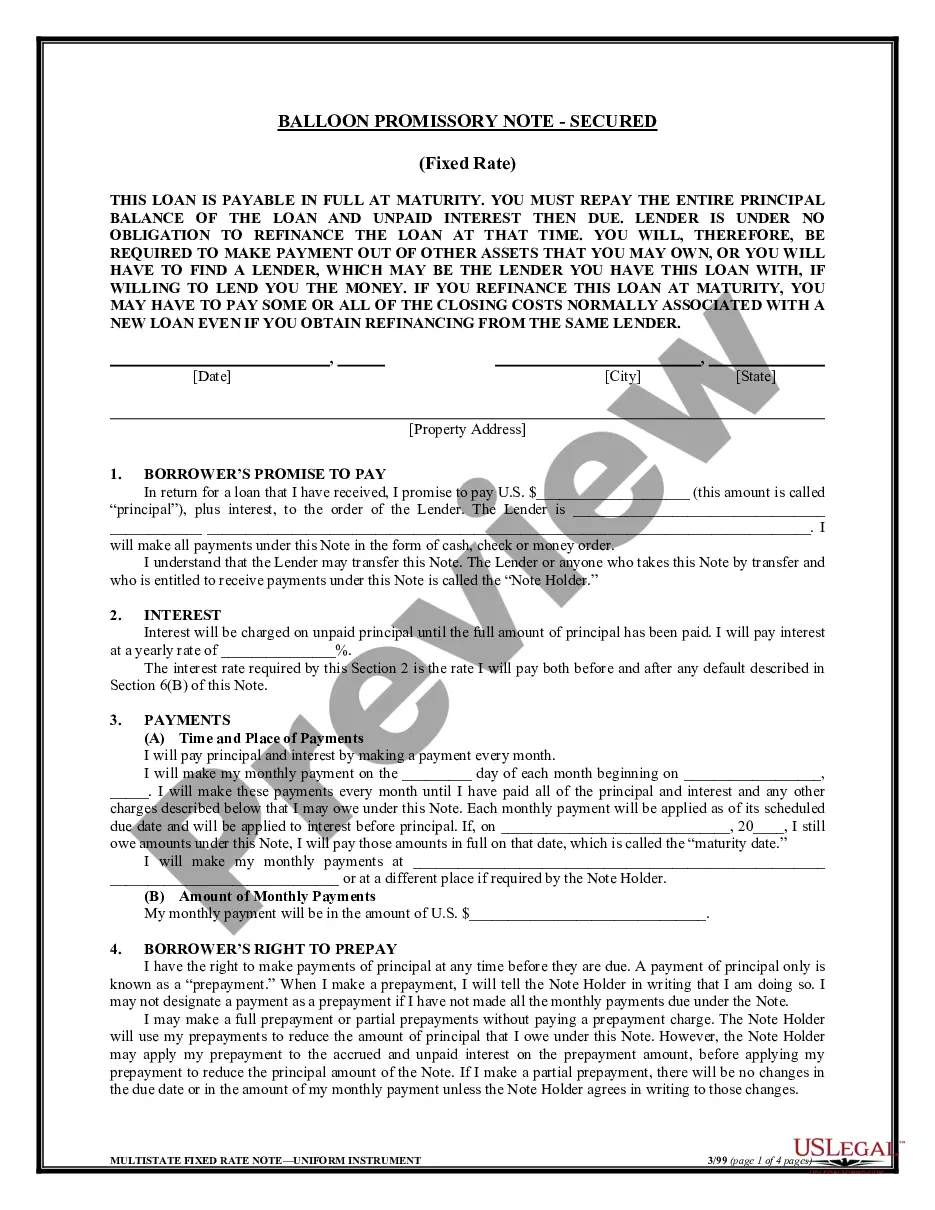

A Promissory Note with Balloon Payments is a loan contract that enables a lender set loan terms with one or more larger payments at the end. This lending document helps you to clarify the terms of a loan, define the payment schedule, and provide an amortization table, if the loan includes interest.

Make the balloon payment so you own the car - If you have the money, you can make the optional final payment and own the car outright. Return the car - If you don't have the money available, or you just don't want the car, you can return it without having to make any more payments.

When the loan is interest-only, you only pay interest throughout the life of the loan. The final payment on the loan is called a balloon payment and equals the entire principal. This amount is due at the end of the loan period.

Selling the vehicle is usually the most popular option for when your balloon payment is due. Selling the car will typically cover the cost of the balloon payment, at which point you can then buy a new car and apply for another loan. Trading in the vehicle works much like selling it.

Let's dive into these in detail. Pay in Full: Settle the Balloon Payment. ... Refinancing Options: Managing Balloon Payments. ... Trade-In Route: Alternatives for Balloon Payments. ... Make Extra Payments: Gradually Reduce the Balloon Amount. ... Negotiate with the Lender: Seek Flexible Repayment Terms.

If your car is worth less than the balloon payment value, it can be better to hand the car back to the dealer as you'd lose money and can find similar models for less. But if your PCP car is worth more than the value of the balloon payment, you could be better off paying it in full or refinancing it.