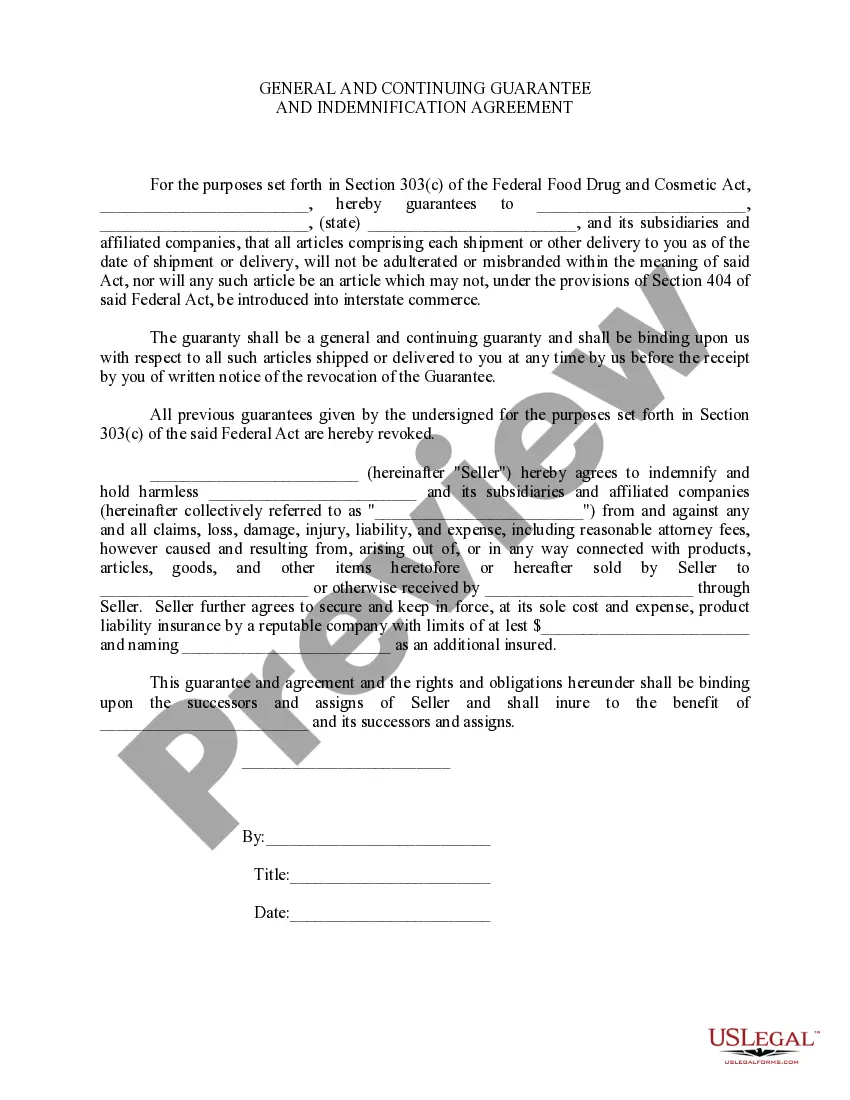

This form states that the guarantor does covenant and agree to defend, indemnify and hold harmless, absolutely and unconditionally,the seller from and against any and all damages, losses, claims, demands, actions, causes of actions, costs, expenses, liabilities and obligations of any kind whatsoever, including, but not limited to, attorney's fees.

Arizona General Guaranty and Indemnification Agreement

Category:

State:

Multi-State

Control #:

US-00525

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out General Guaranty And Indemnification Agreement?

Have you visited a location where you consistently require documents for various enterprises or particular tasks.

There are numerous legal document templates accessible online, but locating reliable ones isn't straightforward.

US Legal Forms offers a vast collection of document templates, including the Arizona General Guaranty and Indemnification Agreement, designed to fulfill federal and state regulations.

Once you find the suitable document, click on Purchase now.

Choose a payment plan you prefer, enter the necessary information to create your account, and finalize your purchase using PayPal or credit card.

- If you are already familiar with the US Legal Forms site and have an account, simply Log In.

- Then, you can download the Arizona General Guaranty and Indemnification Agreement template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Find the document you need and ensure it is for the correct city/region.

- Utilize the Preview button to examine the form.

- Review the description to verify that you have selected the correct document.

- If the document is not what you seek, use the Search field to find one that meets your requirements.

Form popularity

FAQ

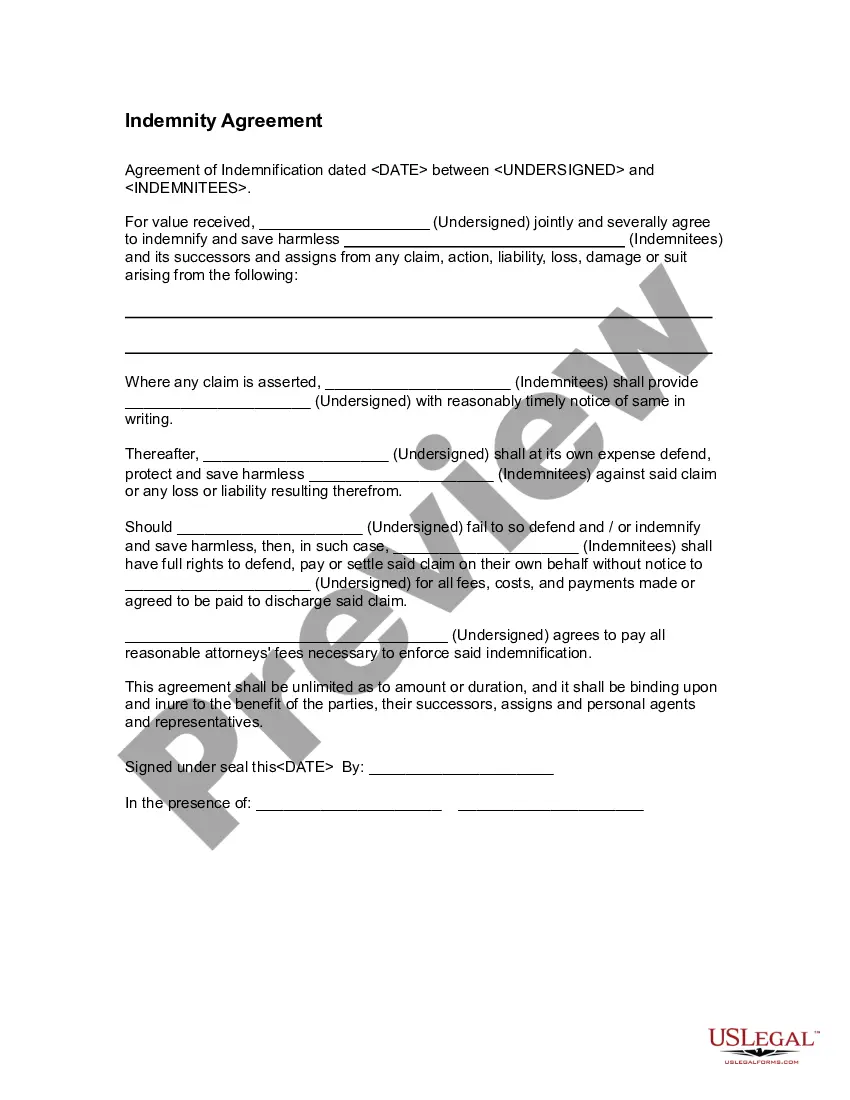

Indemnity is a comprehensive form of insurance compensation for damages or loss. In this type of arrangement, one party agrees to pay for potential losses or damages caused by another party.

A common example of indemnification happens with reagrd to insurance transactions. This often happens when an insurance company, as part of an individual's insurance policy, agrees to indemnify the insured person for losses that the insured person incurred as the result of accident or property damage.

An indemnification agreement, also called an indemnity agreement, hold harmless agreement, waiver of liability, or release of liability, is a contract that provides a business or a company with protection against damages, loss, or other burdens.

The key differences between guarantees and indemnities include: a guarantee is a secondary liability, which means that there will be another person who is primarily liable for the obligation; whereas, an indemnity imposes a primary liability.

A continuing guaranty is an agreement by the guarantor to be liable for the obligations of someone else to the lender, even if there are several different obligations that are made, renewed or repaid over time. In contrast, a specific guaranty is limited only to one individual transaction.

The essence of a continuing guarantee is that it covers a series of transactions and each transaction is a separate transaction which creates a liability on the surety till it is repaid. The liability of the surety changes with every further advance by the creditor to the debtor.

An indemnity agreement is a contract that protect one party of a transaction from the risks or liabilities created by the other party of the transaction. Hold harmless agreement, no-fault agreement, release of liability, or waiver of liability are other terms for an indemnity agreement.200c

To indemnify means to compensate someone for his/her harm or loss. In most contracts, an indemnification clause serves to compensate a party for harm or loss arising in connection with the other party's actions or failure to act. The intent is to shift liability away from one party, and on to the indemnifying party.

Guaranty Agreement a two-party contract in which the first party agrees to perform in the event that a second party fails to perform. Unlike a surety, a guarantor is only required to perform after the obligee has made every reasonable and legal effort to force the principal's performance.