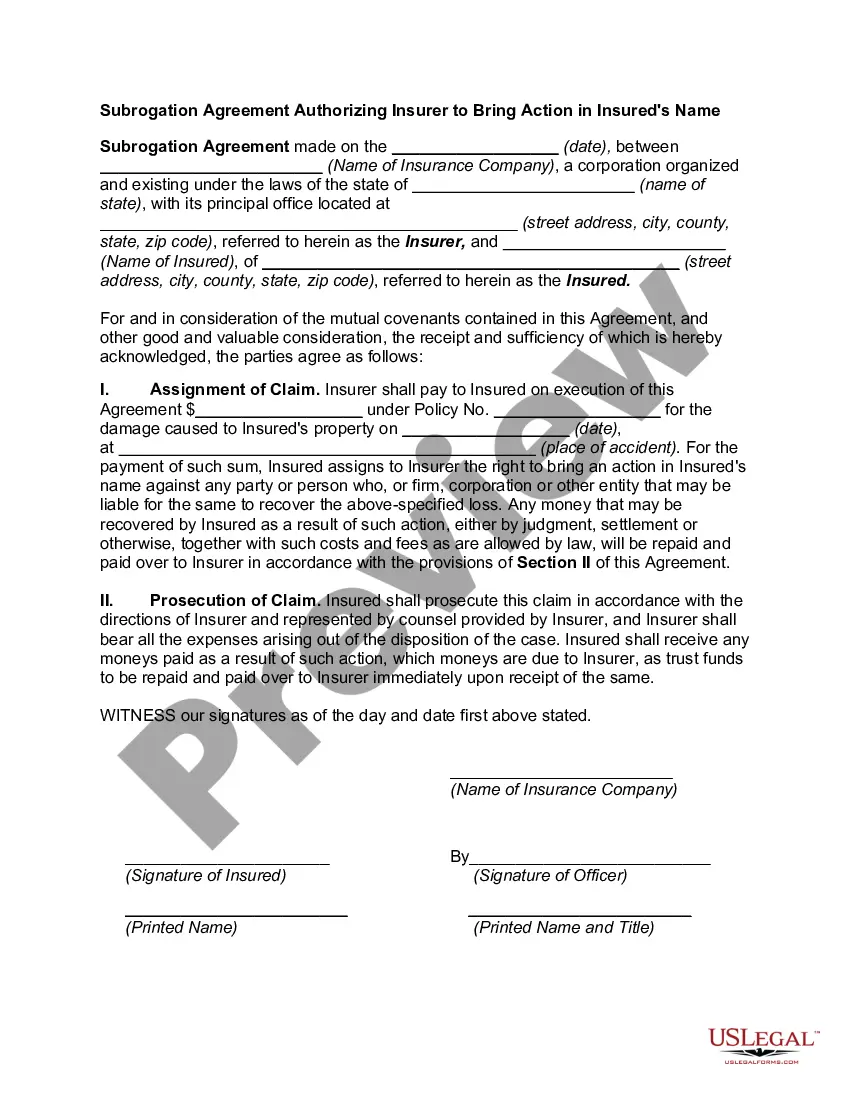

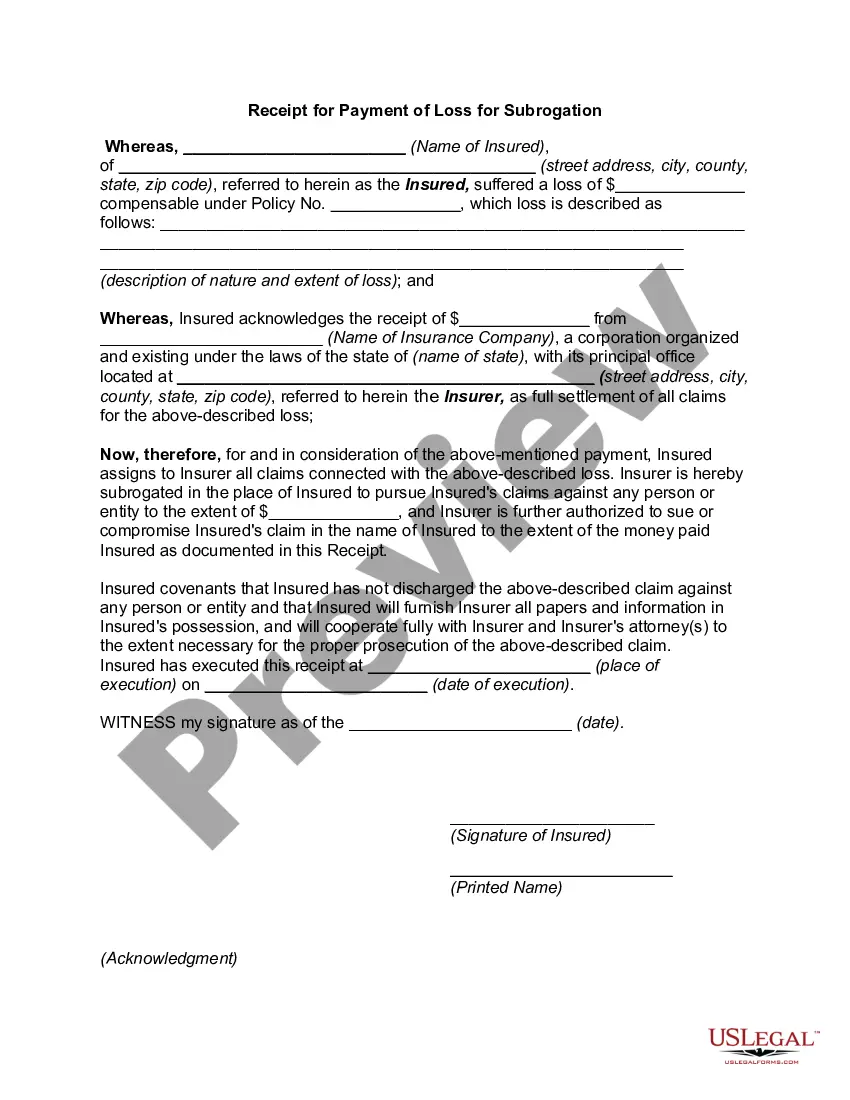

Alaska Subrogation Agreement between Insurer and Insured

Description

How to fill out Subrogation Agreement Between Insurer And Insured?

If you have to full, download, or print authorized papers layouts, use US Legal Forms, the greatest selection of authorized forms, that can be found on-line. Make use of the site`s easy and convenient look for to get the files you will need. A variety of layouts for company and specific functions are sorted by types and suggests, or keywords and phrases. Use US Legal Forms to get the Alaska Subrogation Agreement between Insurer and Insured with a handful of clicks.

When you are presently a US Legal Forms consumer, log in for your bank account and click on the Acquire key to get the Alaska Subrogation Agreement between Insurer and Insured. You can also access forms you formerly acquired inside the My Forms tab of the bank account.

If you work with US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have chosen the shape for the correct metropolis/region.

- Step 2. Take advantage of the Preview solution to look over the form`s content material. Never forget about to read the description.

- Step 3. When you are not satisfied using the kind, use the Search field near the top of the screen to discover other variations of the authorized kind design.

- Step 4. When you have found the shape you will need, click the Get now key. Opt for the costs prepare you choose and put your references to sign up on an bank account.

- Step 5. Method the financial transaction. You may use your charge card or PayPal bank account to accomplish the financial transaction.

- Step 6. Choose the structure of the authorized kind and download it in your system.

- Step 7. Total, modify and print or indication the Alaska Subrogation Agreement between Insurer and Insured.

Every authorized papers design you purchase is your own forever. You have acces to each kind you acquired in your acccount. Select the My Forms section and decide on a kind to print or download once again.

Contend and download, and print the Alaska Subrogation Agreement between Insurer and Insured with US Legal Forms. There are many professional and condition-specific forms you can use to your company or specific needs.

Form popularity

FAQ

What is Subrogation? Subrogation in insurance is a legal right of the insurance company to legally pursue a third-party responsible for the damages/insurance loss caused to the insured. Subrogation is done to recover the claim amount insurance company pays to the insured for the damages.

When factoring comparative negligence and improper referrals, the recovery rate should be somewhere in the range of 85-90%. This requires adjusters properly identifying subrogation, assessing comparative negligence and pursuing only what they are entitled to.

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.

It says that the insurer (which is the insurance company) pays for a loss to the insured (an individual or company) due to the wrongdoing of a third party, then the insurer has the authority to subrogate the rights of insured and therefore is able to prosecute a suit against the wrongdoer for the recovery of the amount ...

One example of subrogation is when an insured driver's car is totaled through the fault of another driver. The insurance carrier reimburses the covered driver under the terms of the policy and then pursues legal action against the driver at fault.

An insurer may attempt to subrogate against an additional insured for completed operations injuries caused by the insured if the additional insured endorsement provides coverage only for ongoing operations injuries.

Disadvantages of Subrogation On the downside, subrogation claims can sometimes result in delays. Recovering costs from the at-fault party can take time, especially if the case goes to court.