Nebraska Bankruptcy Guide and Forms Package for Chapters 7 or 13

Understanding this form

The Nebraska Bankruptcy Guide and Forms Package for Chapters 7 or 13 offers a comprehensive and organized set of legal documents necessary for individuals seeking bankruptcy relief. This package includes detailed instructions and resources tailored for filing under either Chapter 7 or Chapter 13, making it easier for users to understand their options and comply with legal requirements.

Key parts of this document

- Instructions for determining eligibility for Chapter 7 or Chapter 13 bankruptcy.

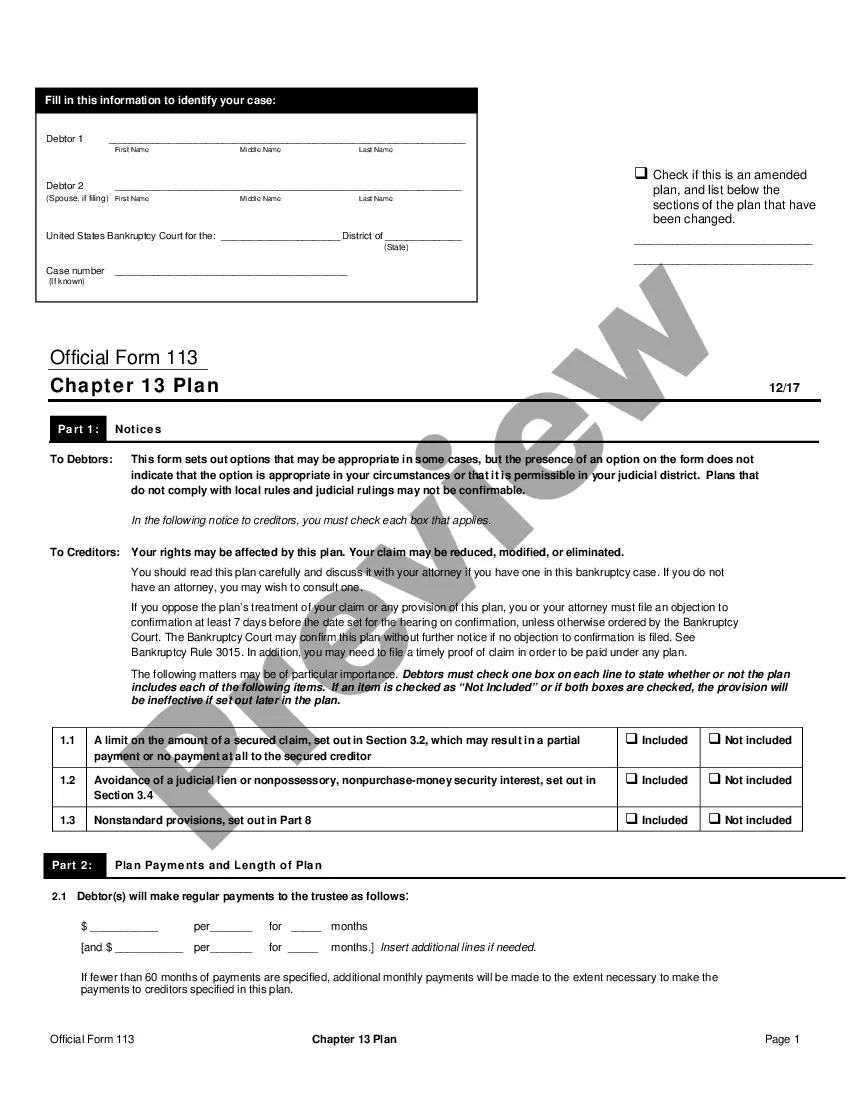

- Downloadable forms including the Chapter 7 Statement of Current Monthly Income and Chapter 7 Means Test Calculation.

- Templates for Chapter 13 repayment plan submission to the court.

- Guidance on listing exempt property to protect certain assets during bankruptcy.

- Information regarding the role of an attorney in the bankruptcy process.

When this form is needed

This form package should be used when an individual is facing overwhelming debt and is considering bankruptcy as a solution. It is particularly relevant for those unsure of whether to file under Chapter 7 for liquidation or Chapter 13 for structured repayment. Additionally, this package assists individuals in making informed decisions regarding the implications of each bankruptcy type.

Intended users of this form

This package is intended for:

- Individuals or couples facing financial difficulties.

- Sole proprietors needing to file for personal bankruptcy.

- Those unsure about which chapter of bankruptcy to file under.

- Individuals seeking resources and guidance on how to complete bankruptcy filings.

Completing this form step by step

- Identify the chapter of bankruptcy you are eligible for: Chapter 7 or Chapter 13.

- Gather all necessary financial documents to determine current income and debts.

- Complete the required forms, including the Chapter 7 Statement of Your Current Monthly Income or Chapter 13 repayment plan.

- List all exempt property on Schedule C and ensure it's accurately described.

- File your completed documents with the bankruptcy court and keep copies for your records.

Does this document require notarization?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Filing the incorrect chapter that does not suit your financial situation.

- Failing to list all creditors or debts, which can result in problems during discharge.

- Neglecting to complete the Means Test accurately.

- Omitting necessary documentation when filing with the court.

Benefits of using this form online

- Immediate access to up-to-date forms and instructions without waiting for physical delivery.

- Convenient editing of documents to tailor the forms to your specific situation.

- Secure storage of your completed forms for future reference.

- Enhanced guidance provided through easy-to-follow instructions.

Key takeaways

- The Nebraska Bankruptcy Guide and Forms Package aids in navigating the complexities of bankruptcy filings.

- Understanding the differences between Chapter 7 and Chapter 13 is critical for effective decision-making.

- Accurate and complete documentation is essential to avoid complications in the bankruptcy process.

- Consider legal representation for a smoother filing experience and to address unique circumstances.

Looking for another form?

Form popularity

FAQ

There is no minimum amount of debt you must have in order to file for bankruptcy relief. While the amount of your debt is an important factor to consider, there are other more important factors to take into account in determining if a bankruptcy filing is in your best interest.

In turn, the trustee disperses the funds to creditors. Sometimes, however, the filer can't continue funding the repayment plan due to a financial change and converts the case to a Chapter 7 bankruptcy. If the Chapter 13 trustee is holding any plan payments for your creditors, the funds will be returned to you.

Aside from amended Schedules I and J, all you have to do to convert your Chapter 13 case to one under Chapter 7 is file a Notice of Conversion that provides notice to the court and your creditors about the change. You will also be required to pay a one time $25 conversion fee.

Once filed, a Chapter 7 bankruptcy typically takes about 4 - 6 months to complete. The bankruptcy discharge is granted 3 - 4 months after filing in most cases. Written by Attorney Andrea Wimmer. Most Chapter 7 bankruptcy cases take between 4 - 6 months to complete after filing the case with the court.

Analyze your debt. Determine your property exemptions. Make sure you are eligible. Redeem or reaffirm secured debts. Fill out the bankruptcy forms. Take a credit counseling course. File the forms. Pay the filing fee or request a fee waiver.

Chapter 13 to Chapter 7. If you received a Chapter 13 discharge and you'd like to receive a Chapter 7 discharge, you'll have to wait six years between filing dates. But there is an exception to this rule. The six-year rule won't apply if, in the previous Chapter 13, you paid back: all of your unsecured debts, or.

For Chapter 7 bankruptcy filings, you must wait eight years from the filing date of your previous petition. Filing prematurely before those eight years have expired, you will not be granted a discharge.

A bankruptcy dismissal closes your bankruptcy case, and if it occurs before you receive a discharge, it will mean that: you've lost the protection of the automatic stay (the order that prohibits creditors from collecting debts), and. you'll continue to be liable for your debts.

Because a chapter 7 discharge is subject to many exceptions, debtors should consult competent legal counsel before filing to discuss the scope of the discharge. Generally, excluding cases that are dismissed or converted, individual debtors receive a discharge in more than 99 percent of chapter 7 cases.