Gift Real Estate With Tax

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

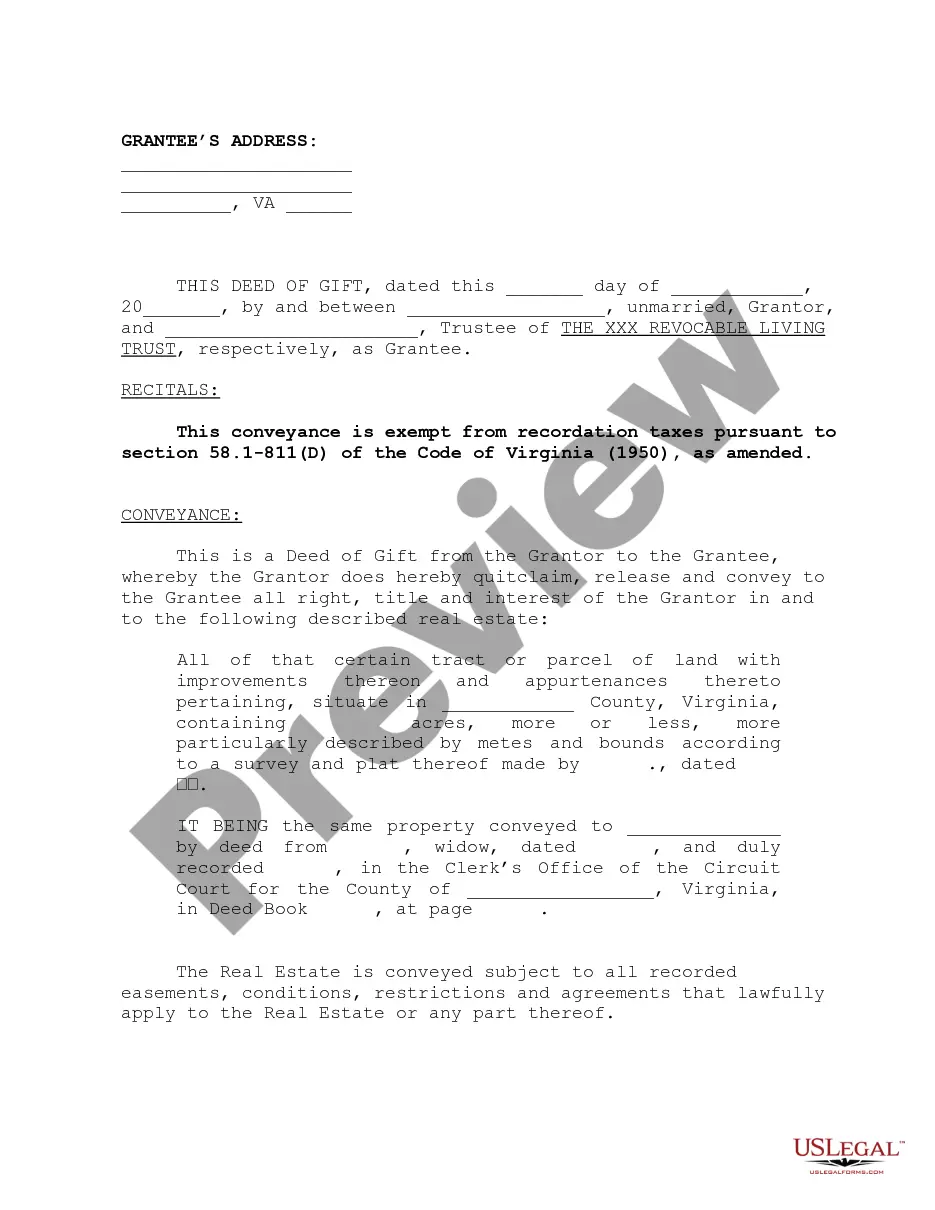

How to fill out Virginia Deed Of Gift?

Securing a primary location to obtain the most up-to-date and suitable legal templates constitutes a significant portion of managing bureaucracy. Identifying the appropriate legal documents requires accuracy and meticulousness, which is why it is essential to obtain samples of Gift Real Estate With Tax exclusively from reliable sources, such as US Legal Forms. An incorrect template can squander your time and delay your current situation. With US Legal Forms, you have minimal concerns. You can access and review all the information regarding the document’s applicability and significance for your situation and within your state or county.

Consider the following steps to finalize your Gift Real Estate With Tax.

Eliminate the stress associated with your legal documentation. Explore the extensive US Legal Forms library where you can discover legal templates, assess their relevance to your situation, and download them immediately.

- Utilize the catalog navigation or search bar to find your template.

- Review the form’s details to confirm it meets the criteria of your state and locality.

- Examine the form preview, if accessible, to verify that it is indeed the one you need.

- Return to the search and seek the appropriate template if the Gift Real Estate With Tax does not align with your needs.

- If you are confident about the form’s applicability, download it.

- If you are a registered user, click Log in to verify and access your selected templates in My documents.

- If you do not have an account yet, click Buy now to obtain the template.

- Choose the pricing plan that fits your requirements.

- Proceed to the registration to complete your purchase.

- Finalize your purchase by selecting a payment method (credit card or PayPal).

- Choose the file format for downloading Gift Real Estate With Tax.

- After you have the form on your device, you can modify it using the editor or print it and complete it manually.

Form popularity

FAQ

When you buy a house with someone else, you must file taxes based on your ownership percentage. It’s crucial to keep records of your contributions, as this affects your tax responsibilities. If you plan to gift real estate with tax considerations, consulting a tax professional can help clarify how to best file your taxes.

To transfer real estate as a gift, you need to prepare a deed that clearly states the intent to gift the property. You should also consider filing a gift tax return if the value exceeds the annual exclusion limit. Utilizing a platform like US Legal Forms can guide you through the paperwork to ensure a smooth transfer while addressing gift real estate with tax properly.

You do not necessarily need an attorney to file a gift tax return, but consulting one can be beneficial. Gift real estate with tax can be complex, and an attorney can help ensure you follow all legal requirements. They can also assist in understanding the implications of your gift and help you avoid potential pitfalls.

When you gift your son $75,000 for a down payment, you may trigger gift tax considerations. In the United States, the IRS allows an annual gift exclusion, which is the amount you can give without incurring gift tax. For 2023, this exclusion is $17,000 per recipient. Since your gift exceeds this amount, you will likely need to file a gift tax return, but you may not owe any tax if you stay within your lifetime exemption.

To document a gift of real estate with tax considerations, you need a written agreement that outlines the details of the gift, including the property description and its fair market value. Additionally, filing IRS Form 709 is essential if the gift exceeds the exclusion limit. Proper documentation ensures that both you and the recipient comply with tax regulations. Utilizing platforms like uslegalforms can streamline this process by providing templates and guidance.

When you gift real estate with tax implications, the IRS considers the fair market value of the property at the time of the gift. If the value exceeds the annual exclusion limit, you may need to file a gift tax return. However, the recipient typically does not owe taxes when they receive the property. Understanding these tax rules can help you navigate the complexities of gifting real estate.

Yes, you can gift a house that you own to your children. The most common way to gift property is by way of a "transfer for nil consideration" (or a ?deed of gift?, as it is commonly known). This is often a way to reduce the amount of Inheritance Tax they need to pay.

You don't need to pay CGT if: You've lived there the entire time (it was your home) Or you give it to your spouse. Or you put it into a trust for the benefit of your child. In this situation, it will be deferred until your child sells the property.

You don't need to pay CGT if: You've lived there the entire time (it was your home) Or you give it to your spouse. Or you put it into a trust for the benefit of your child. In this situation, it will be deferred until your child sells the property.

Generally, if you give a property away, then you will be treated as making a disposal for capital gains tax purposes. This means that capital gains tax will be calculated as if the property had been sold for its market value at the time of the gift.