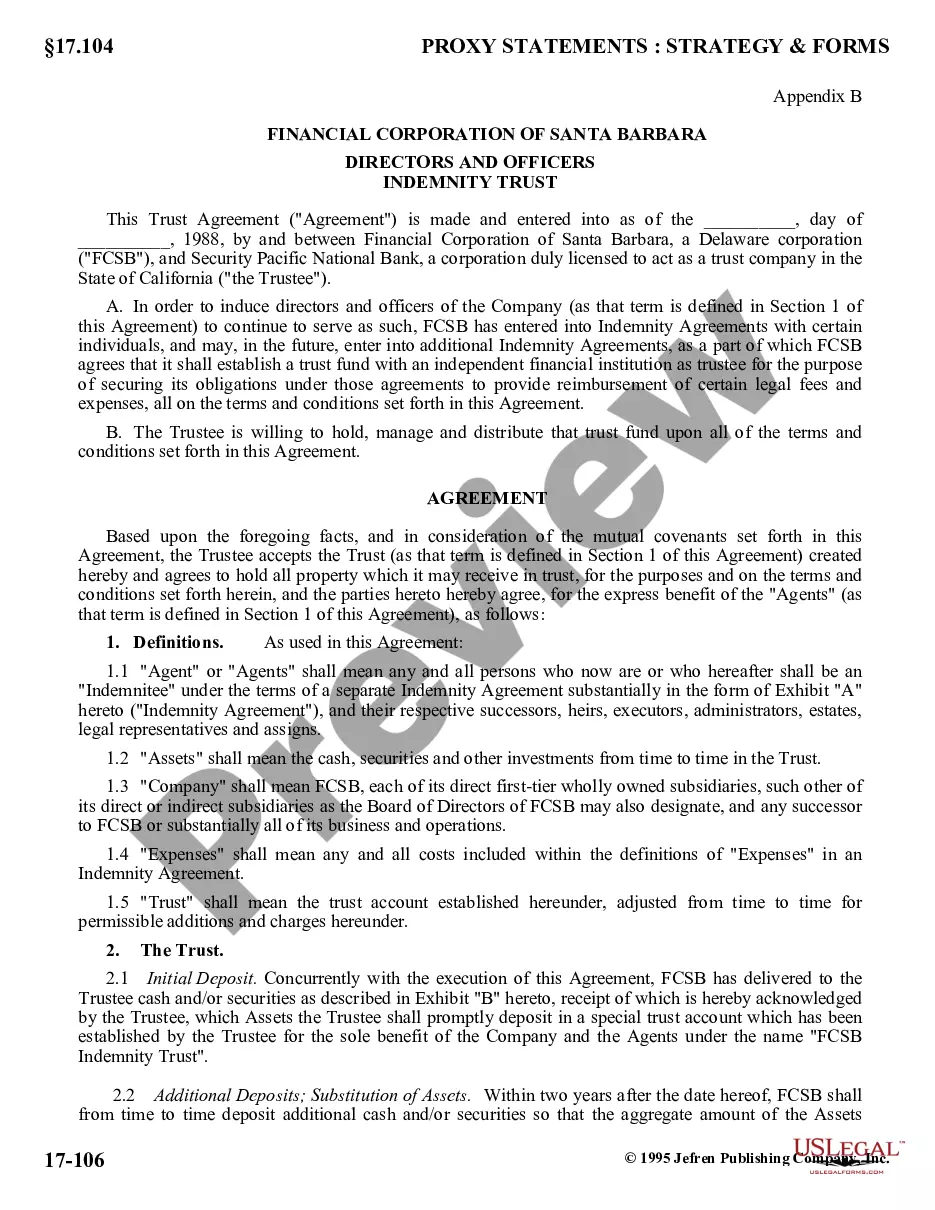

Directors And Officers Liability

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Directors And Officers Liability Insurance?

- If you're a returning user, log in to your account and navigate to the Download button to retrieve your desired form. Ensure that your subscription is active and renew it if necessary.

- For first-time users, start by reviewing the Preview mode and form description to confirm that you have selected the correct document that fits your state's requirements.

- If your needs change, utilize the Search tab at the top to find a different template that may be more suitable.

- Once you've found the appropriate form, click the Buy Now button and select your preferred subscription plan. You'll need to create an account to access the vast library.

- Proceed with your purchase by entering your credit card information or using your PayPal account to complete the transaction.

- After purchasing, download your selected form to your device and access it anytime from the My Forms section of your profile.

With US Legal Forms, you benefit from a robust collection of over 85,000 legal templates and the option to consult with premium legal experts for added assurance. This ensures that your documents are both precise and legally compliant.

Don’t wait to secure your business. Start accessing essential directors and officers liability forms today!

Form popularity

FAQ

An advertisement and officers (ad & o) policy, which is another term for directors and officers liability insurance, covers various financial liabilities faced by company leaders. This policy generally includes legal defense costs, settlements, and judgments that arise from the actions or decisions made by executives while performing their duties. By choosing the right ad & o policy, you can safeguard personal assets and ensure that leadership is able to perform their roles confidently and effectively.

Certain items are not included in directors and officers liability coverage, such as fraud, personal misconduct, or criminal acts committed by the insured. Additionally, coverage typically excludes claims arising from employment practices, such as wrongful termination or discrimination, which often require separate policies. Understanding these exclusions is vital, as it helps executives identify any additional coverage they may need to fully protect themselves.

Side A coverage is a specific part of directors and officers liability insurance that protects individual executives when the company cannot indemnify them due to financial instability or legal issues. This level of coverage ensures that executives receive legal defense and funds for settlements or judgments even if the company is unable to provide support. Essentially, Side A coverage acts as a safety net, empowering leaders to make decisions without worrying about personal financial risks.

Directors and officers liability insurance provides protection for individual leaders from legal actions taken against them while they manage a company. This coverage typically includes defense costs for lawsuits, settlements, and judgments related to allegations of wrongful acts, such as breach of fiduciary duty or mismanagement. By securing directors and officers liability, you ensure that personal assets remain protected even in challenging circumstances, allowing executives to focus on their responsibilities without fear.

General liability claims can stem from various incidents, such as property damage, bodily injury, or personal injury lawsuits. For instance, a slip and fall accident on company premises might result in a claim against the business. While these claims differ from directors and officers liability, they illustrate the wide array of legal challenges companies may face. Educating yourself about both types of liability is crucial for comprehensive risk management.

The most common D&O claims include allegations of fraud, misrepresentation, and failure to meet contractual obligations. Breach of fiduciary duty claims can also arise when directors make decisions that do not align with shareholder interests. These situations highlight the complexities of managing a company and the need for robust directors and officers liability coverage. By being informed, you can better protect your organization.

The limited liability rule protects officers and directors from personal accountability for company debts, as long as they act in good faith. This rule allows them to make decisions without fearing personal financial loss, providing a sense of security. However, it does not shield them from acts of gross negligence or intentional wrongdoing. Understanding this protection is vital when considering the significance of directors and officers liability.

A D&O claim refers to a legal action taken against directors and officers for alleged wrongful acts. These acts can include mismanagement, conflict of interest, or failing to fulfill fiduciary responsibilities. Such claims can significantly impact the financial health of a company and its leadership. Therefore, having directors and officers liability insurance is essential for safeguarding against these potential issues.

An example of a D&O claim involves a shareholder suing the company's board for failing to disclose financial information that affects stock prices. This lack of transparency can lead to significant losses for investors, prompting them to seek legal recourse. In such cases, claiming directors and officers liability is key, as it holds the responsible parties accountable. Protecting your leadership team with proper insurance can help mitigate these risks.

Directors and officers liability can arise from various situations. Common examples include breach of fiduciary duty, misuse of company funds, and failure to comply with regulations. These issues can lead to financial losses for shareholders or penalties for the company. Understanding these examples is crucial to recognizing the importance of directors and officers liability insurance.