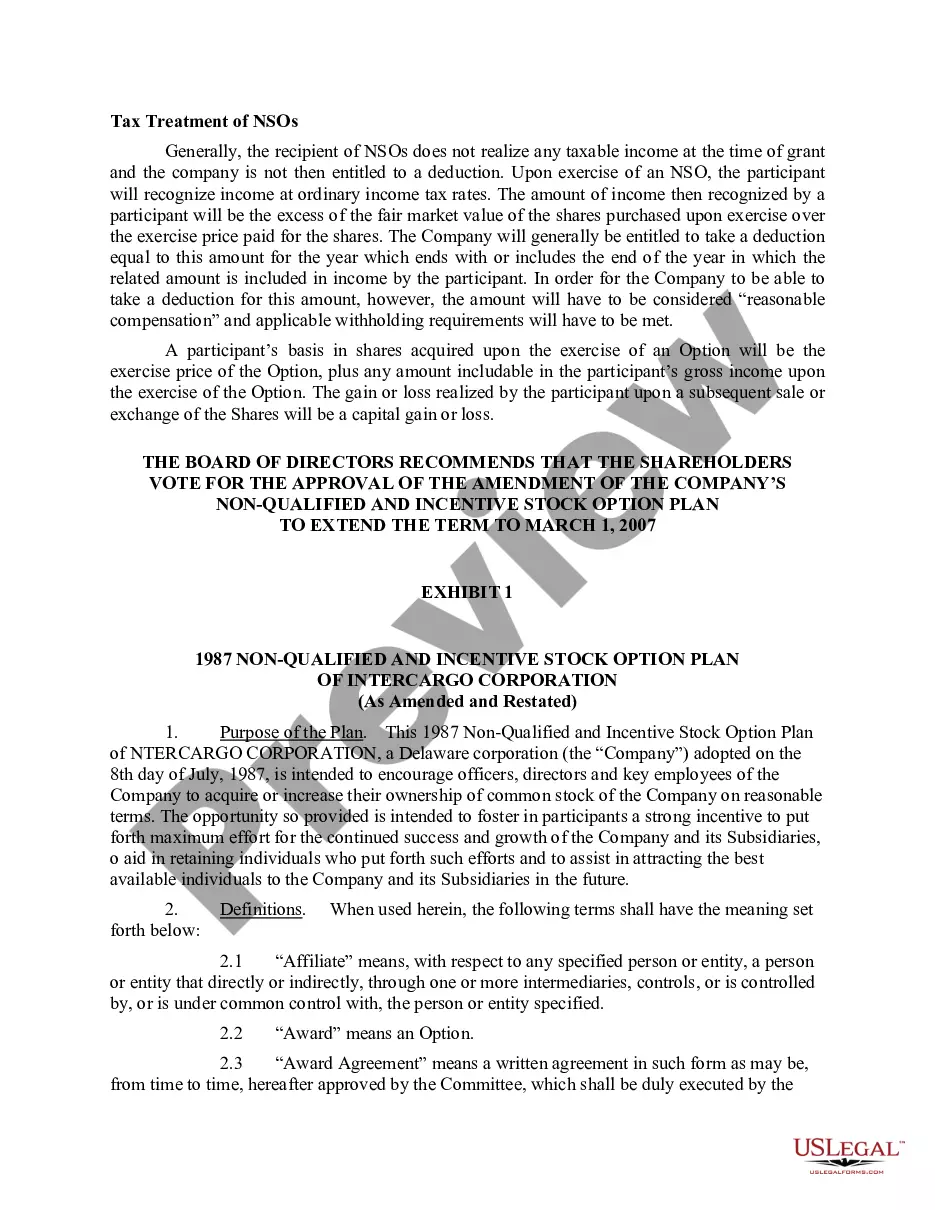

Stock Option Plan Explained

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Stock Incentive Plan Of Ambase Corp.?

- If you're a returning user, log in to your account and retrieve the necessary form by clicking the Download button. Confirm your subscription is still active; renew if it's expired.

- For first-time users, start by browsing the Preview mode and reviewing the form descriptions. Choose the template that meets your specific needs and complies with your local regulations.

- If you encounter any issues or inaccuracies, use the Search tab above to locate an alternative template that suits your requirements.

- Proceed to purchase your selected document by clicking on the Buy Now button. Select a subscription plan, ensuring to create an account to access a wealth of legal resources.

- Complete the payment process using your credit card or PayPal account to finalize your subscription.

- Once the purchase is confirmed, download your legal form and save it on your device. You can access it anytime in the My Forms section of your user profile.

In conclusion, US Legal Forms streamlines the process of handling legal documents with its vast library and expert support. By following these straightforward steps, you can effortlessly manage your stock option plan and other legal needs.

Start today by visiting US Legal Forms and unlocking the best resources for your legal documentation!

Form popularity

FAQ

The risk of stock options primarily lies in their potential to become worthless. If the company's stock does not perform well, your options may not be financially viable. Moreover, understanding your stock option plan explained is essential, as poor timing in exercising options can lead to substantial losses. Utilizing platforms like USLegalForms can provide clarity and support in navigating these complexities.

If you resign from your job, the handling of your Employee Stock Ownership Plan (ESOP) can vary. Typically, you may have the opportunity to exercise any vested options. However, unvested options generally become void. Understanding how your specific stock option plan explained works is crucial for making informed decisions regarding your benefits.

The $100,000 rule relates to employee stock options and indicates that an employee can only exercise stock options worth $100,000 or less per year, based on the fair market value at the time of the grant. This limit ensures that employees receive favorable tax treatment on their options. Understanding this rule is essential for leveraging your stock option plan effectively. For more information, you can explore our resources on the uslegalforms platform to gain clarity.

Yes, an LLC can implement a stock option plan, known as a member option plan. However, the structure of LLCs differs from corporations, so it's essential to understand how to legally frame these options. Using a stock option plan explained within the context of an LLC can allow members or employees to enjoy similar financial incentives, aligning their efforts with company success.

100K stock options typically refer to stock options granted to employees, with a potential value of $100,000 becoming exercisable within a tax-efficient framework. Understanding how these options function is essential when considering a stock option plan explained, as they offer significant benefits both for employee incentives and for company performance motivation. Utilizing platforms like USLegalForms can provide insightful resources on structuring these options effectively.

The rule of 100,000 often refers to the annual limit on the value of incentive stock options granted under tax rules. Specifically, it means that the stock options that become exercisable cannot exceed $100,000 for tax purposes. When reviewing stock option plans explained, this concept is vital for managing employee equity compensation and maximizing potential tax advantages.

The $100,000 incentive stock option limit refers to the maximum value of ISOs that can be granted to an employee in a calendar year. If the total value of options exceeds this limit, the excess options may be treated as non-qualified stock options. For those exploring stock option plans explained, knowing this limit helps in structuring compensation packages that align with tax benefits.

The $100,000 rule of code 422 D relates to incentive stock options (ISOs) under the Internal Revenue Code. It limits the value of stock options that can become exercisable for any employee in a single year to $100,000. Understanding this rule is crucial as part of a stock option plan explained, allowing employees and employers to navigate tax implications effectively.