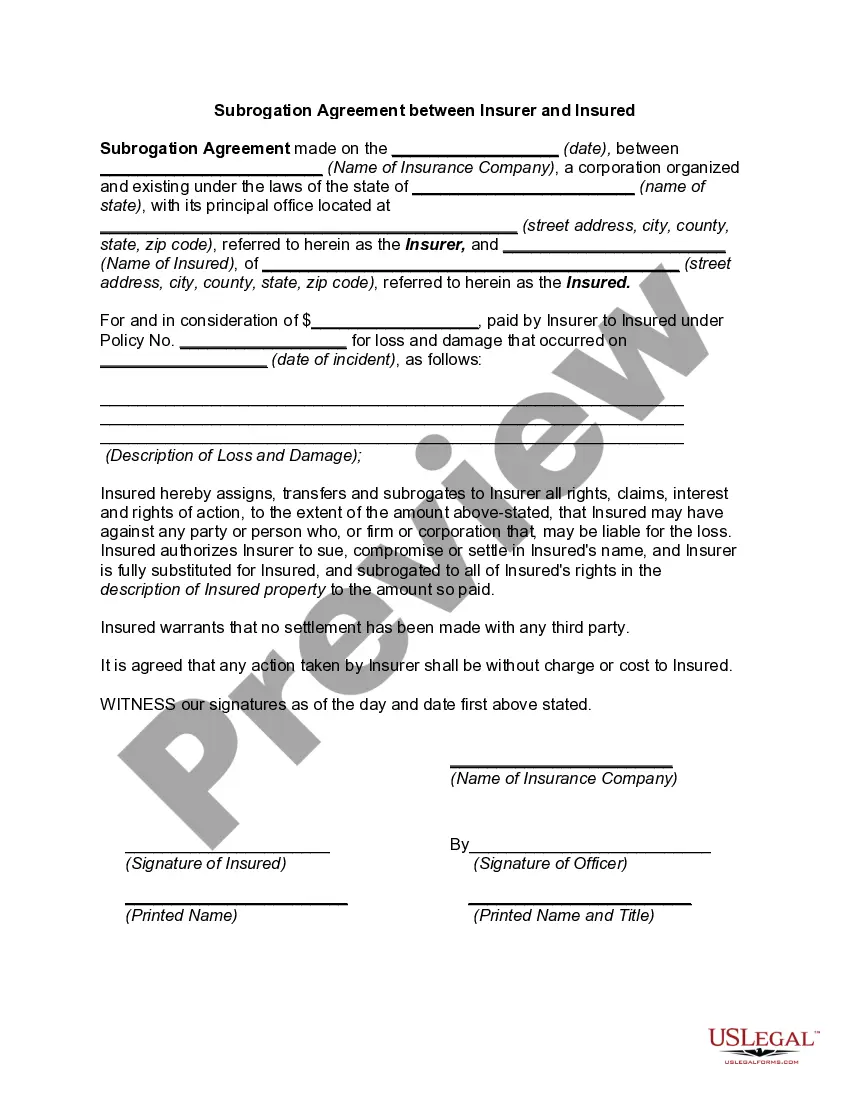

Waiver Of Subrogation Without Additional Insured

Description

Form popularity

FAQ

A waiver of subrogation is beneficial for businesses and individuals engaged in contracts where mutual protection from liability is essential. It protects parties from having their insurance companies pursue claims against each other, which can lead to strained relationships. Anyone operating in fields with high risk, such as construction or event planning, should consider securing this waiver. A 'Waiver of subrogation without additional insured' provision is a smart choice for those seeking peace of mind.

A waiver of subrogation should be included in contracts when parties wish to avoid disputes over liability. It becomes crucial when projects involve shared risks, such as construction or joint ventures, where insurance claims might arise. Including this waiver from the outset may create a more supportive environment for collaboration. Having the right 'Waiver of subrogation without additional insured' provision can ease concerns for all parties involved.

Typically, contractors, developers, or businesses involved in collaborative projects may request a waiver of subrogation. This waiver helps protect their interests by preventing insurance companies from seeking reimbursement from other parties involved in the contract. It fosters a cooperative relationship among parties by limiting potential claims after accidents. Utilizing a 'Waiver of subrogation without additional insured' can simplify these arrangements.

Insurance companies are not strictly required to subrogate, but they often choose to do so as a way to recover losses. By exercising subrogation rights, insurers can hold the responsible party accountable, ensuring that costs do not solely fall on policyholders. However, the decision to pursue subrogation depends on the specific circumstances of a claim and the policy terms. Understanding the 'Waiver of subrogation without additional insured' can be important in these situations.

Writing a subrogation demand letter requires clarity and precision to ensure all parties understand your position. Begin with a clear statement of facts, including the nature of the loss and your request for reimbursement. Mention the waiver of subrogation without additional insured if relevant, as this can impact your claim. By being direct and professional, you can improve the likelihood of a favorable outcome.

To add a waiver of subrogation without additional insured, consult your insurance policy details. You'll need to contact your insurance agent, discuss your requirements, and request the amendment to be included. It's important to document this change and ensure all relevant parties are aware. This addition can greatly enhance your protection against potential claims.

Avoiding subrogation involves careful risk management and clear communication with your contractors or partners. You may consider including a waiver of subrogation without additional insured in your agreements. This mitigates the risk of one party seeking recovery from another after a loss. Always review your insurance contracts to understand your obligations and protections.

To obtain a waiver of subrogation without additional insured, start by reaching out to your insurance provider. Explain your needs and request this specific amendment. They will guide you through any necessary paperwork or adjustments to your policy. Also, ensure that your contracts accurately reflect this waiver, as it can help protect your interests.

There is generally no additional insured status on workers' compensation insurance because the policy is designed to cover employees and employers directly. This insurance focuses on providing benefits to workers injured on the job, not extending coverage to third parties. This unique structure helps streamline processes without complicating contractual obligations. Recognizing this aspect can guide you when navigating waivers of subrogation without additional insured.

Typically, your employer continues to provide health insurance while you are on workers' compensation. The payments may vary based on company policy and specific circumstances, so it's vital to review your employment contract. Health insurance coverage remains crucial during recovery, helping to ease concerns related to medical expenses. Understanding these conditions supplements your knowledge about waiver of subrogation without additional insured.