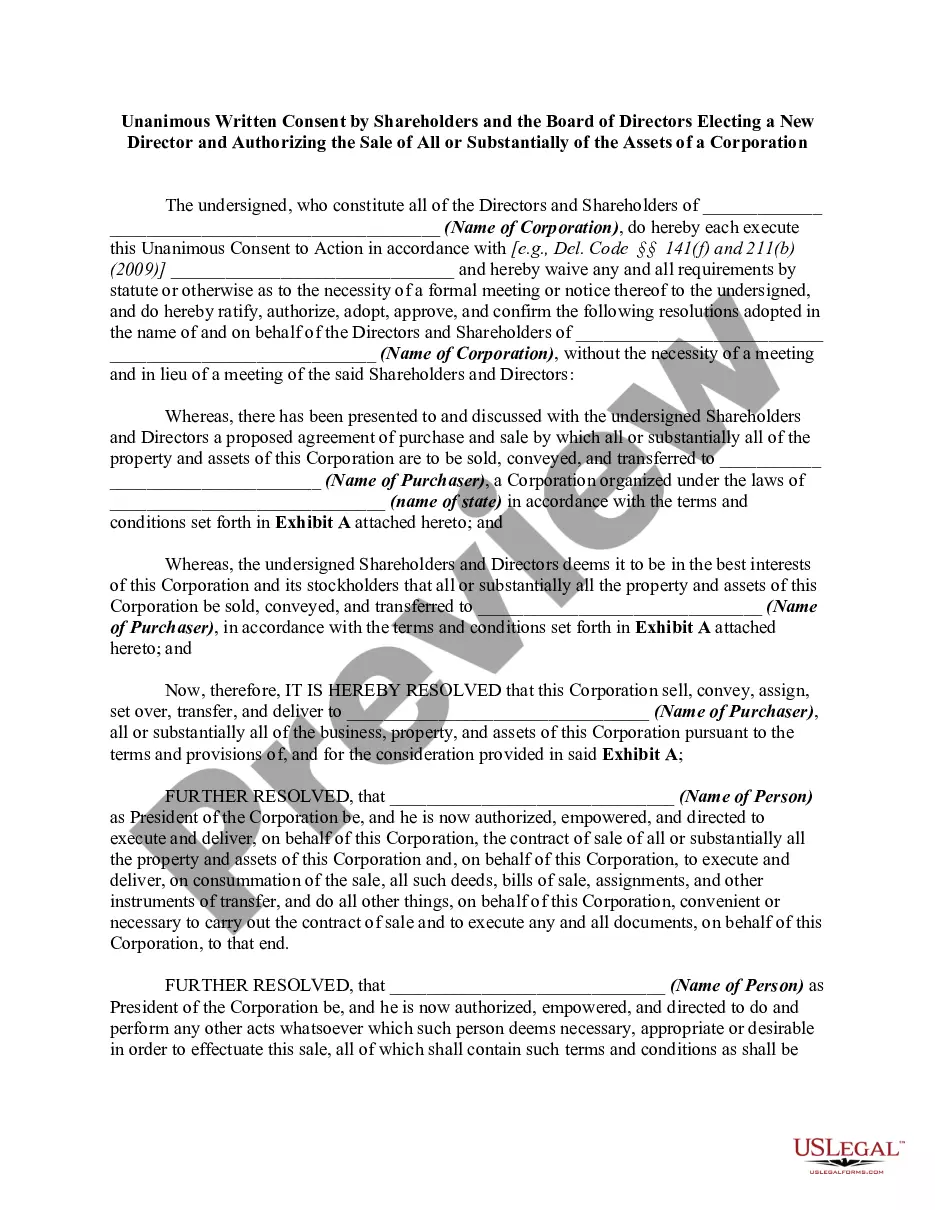

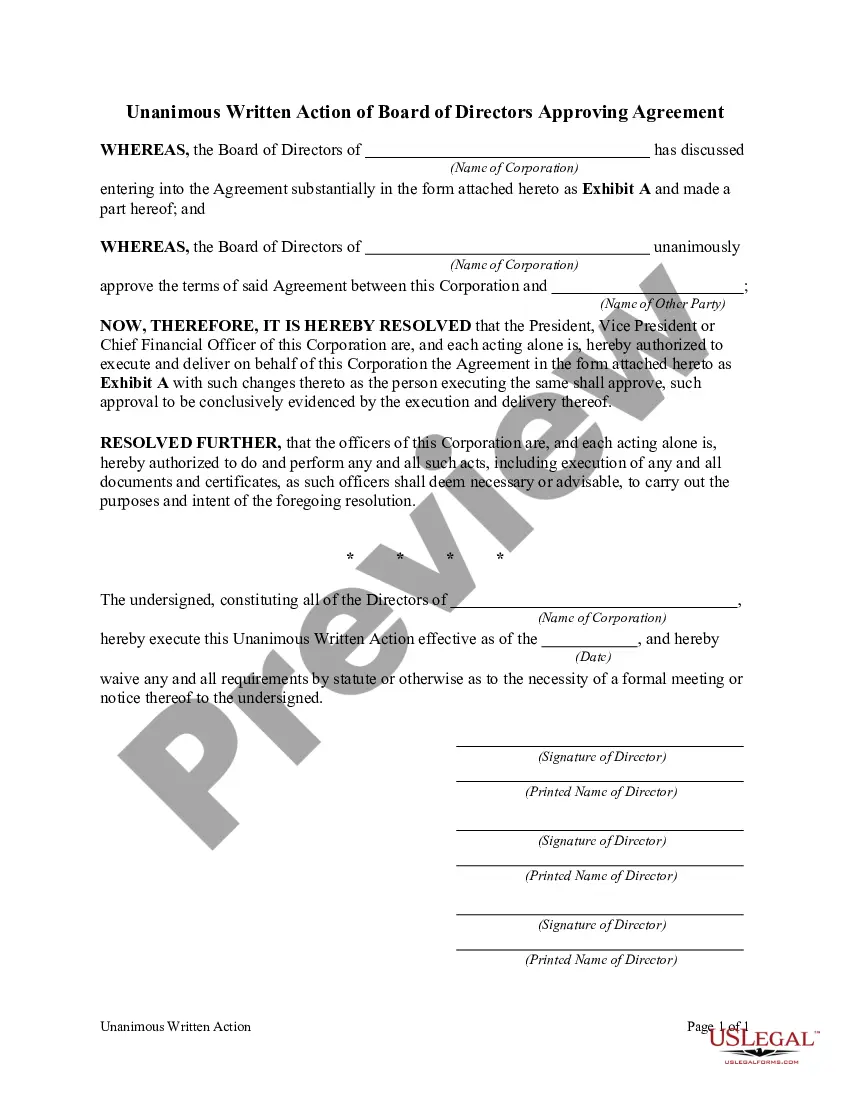

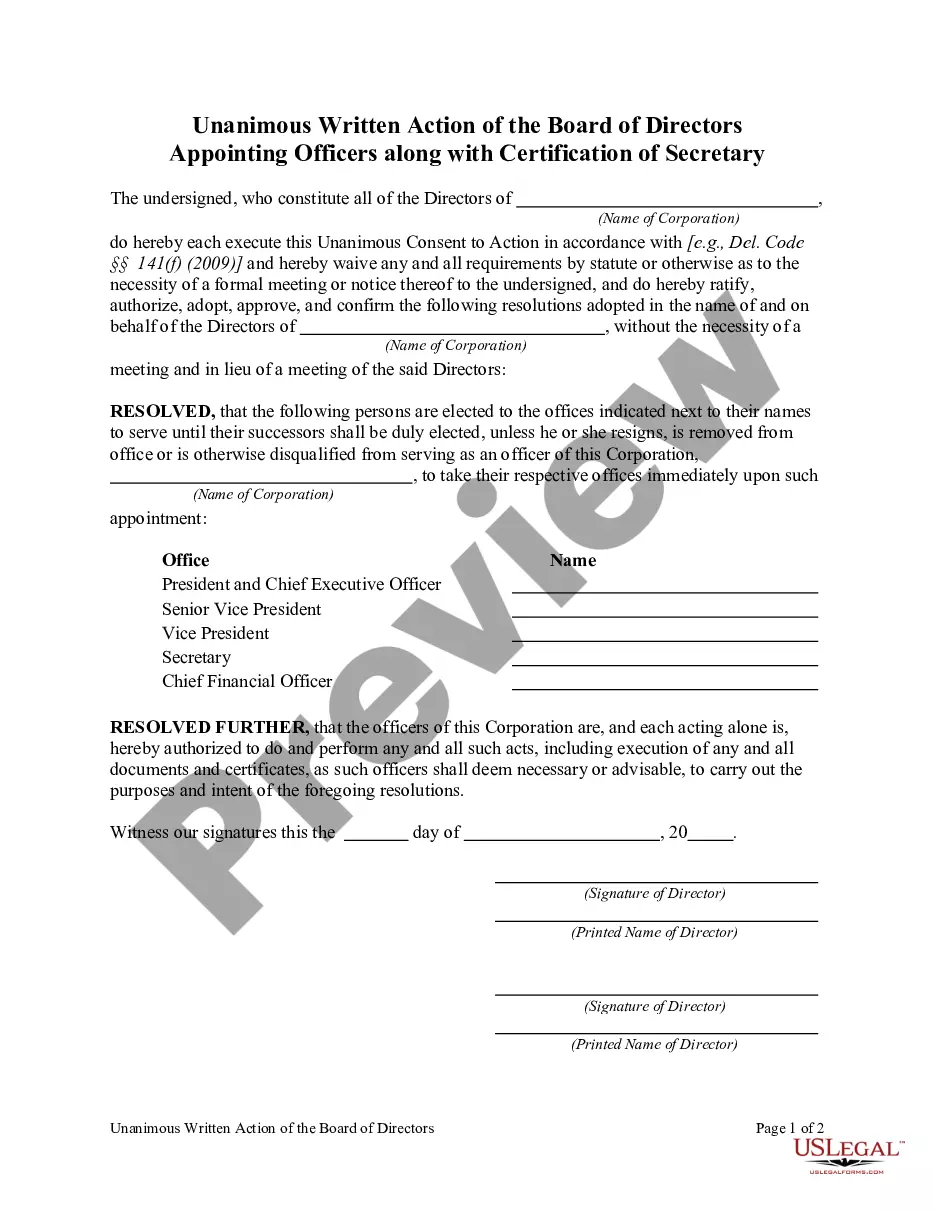

Corporation Removing Foreign Countries

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Unanimous Written Action Of Shareholders Of Corporation Removing Director?

It’s clear that you can’t instantly become a legal authority, nor can you swiftly learn how to prepare Corporation Removing Foreign Countries without a specialized skill set.

Creating legal documents is a labor-intensive task that requires specific education and expertise. So why not entrust the preparation of the Corporation Removing Foreign Countries to the experts.

With US Legal Forms, one of the most extensive legal document collections, you can find everything from court papers to templates for internal corporate communication. We recognize how vital compliance and adherence to federal and local regulations are.

Sign up for a free account and select a subscription plan to purchase the form.

Click Buy now. Once the payment is complete, you can download the Corporation Removing Foreign Countries, complete it, print it, and send or mail it to the designated individuals or organizations.

- That’s why, on our site, all forms are location-specific and current.

- Begin with our platform and obtain the document you require in just minutes.

- Discover the document you need by utilizing the search bar at the top of the page.

- Preview it (if this option is available) and read the accompanying description to determine if Corporation Removing Foreign Countries is what you’re seeking.

- Start your search anew if you require any other form.

Form popularity

FAQ

A foreign corporation that maintains an office or place of business in the United States must generally file Form 1120-F by the 15th day of the 4th month after the end of its tax year. A new corporation filing a short-period return must generally file by the 15th day of the 4th month after the short period ends.

Form 1120-F differs from Form 1120 in that it excludes interest, dividends and royalties derived outside of the U.S., as well as rent paid to unrelated parties outside of the U.S., while Form 1120 includes such items in taxable income on Line 12 of Part I.

Are You Required to File Tax Form 5471? U.S. citizens and residents who are officers, directors or shareholders in certain foreign corporations must file Form 5471 as part of their expat tax return. This form is officially called the Information Return of U.S. Persons with Respect to Certain Foreign Corporations.

Every foreign corporation that is engaged in trade or business in the United States at any time during the tax year or that has income from United States sources must file a return on Form 1120-F, U.S. Income Tax Return of a Foreign Corporation.

Form 1120-F differs from Form 1120 in that it excludes interest, dividends and royalties derived outside of the U.S., as well as rent paid to unrelated parties outside of the U.S., while Form 1120 includes such items in taxable income on Line 12 of Part I.