Promissory Issued Agreement Forbearance

Description

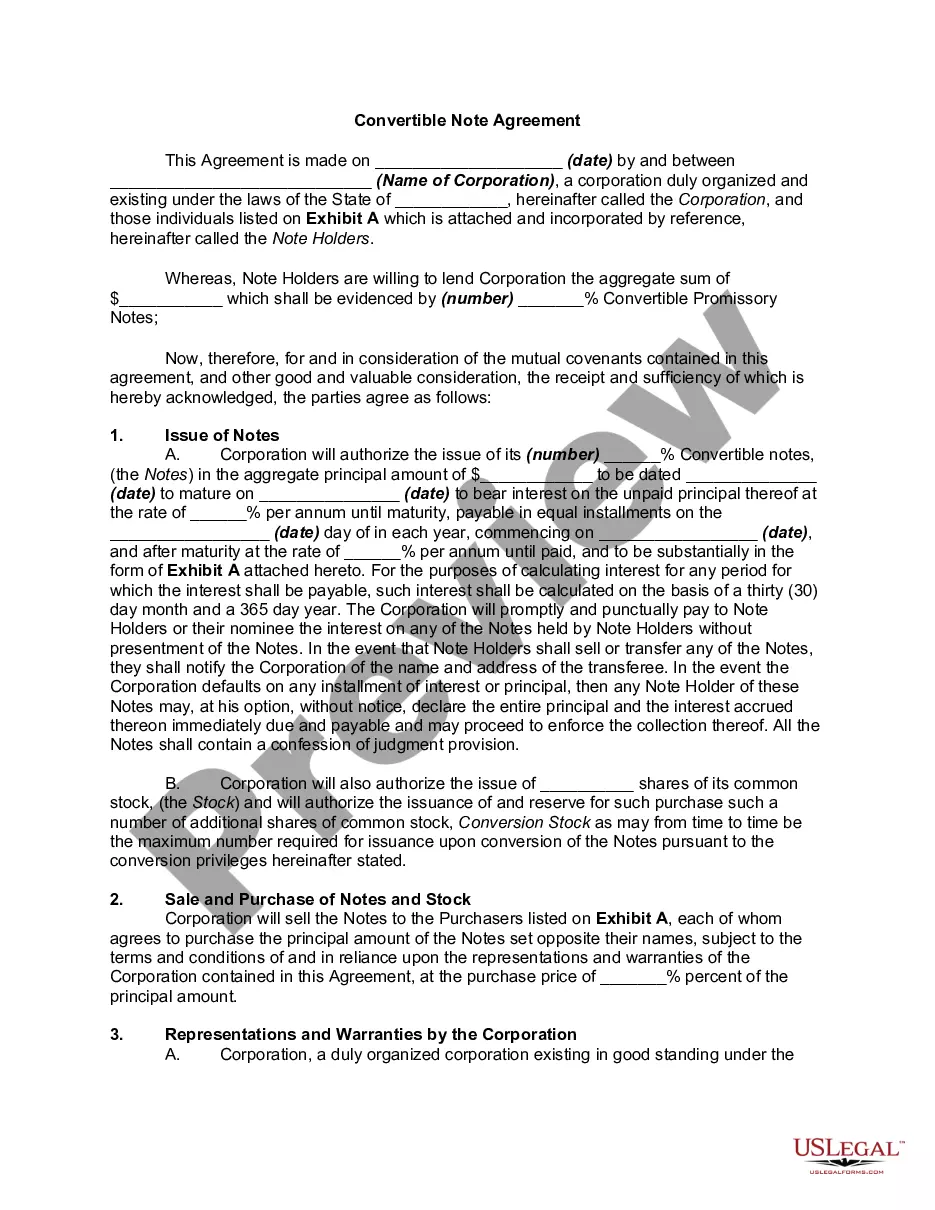

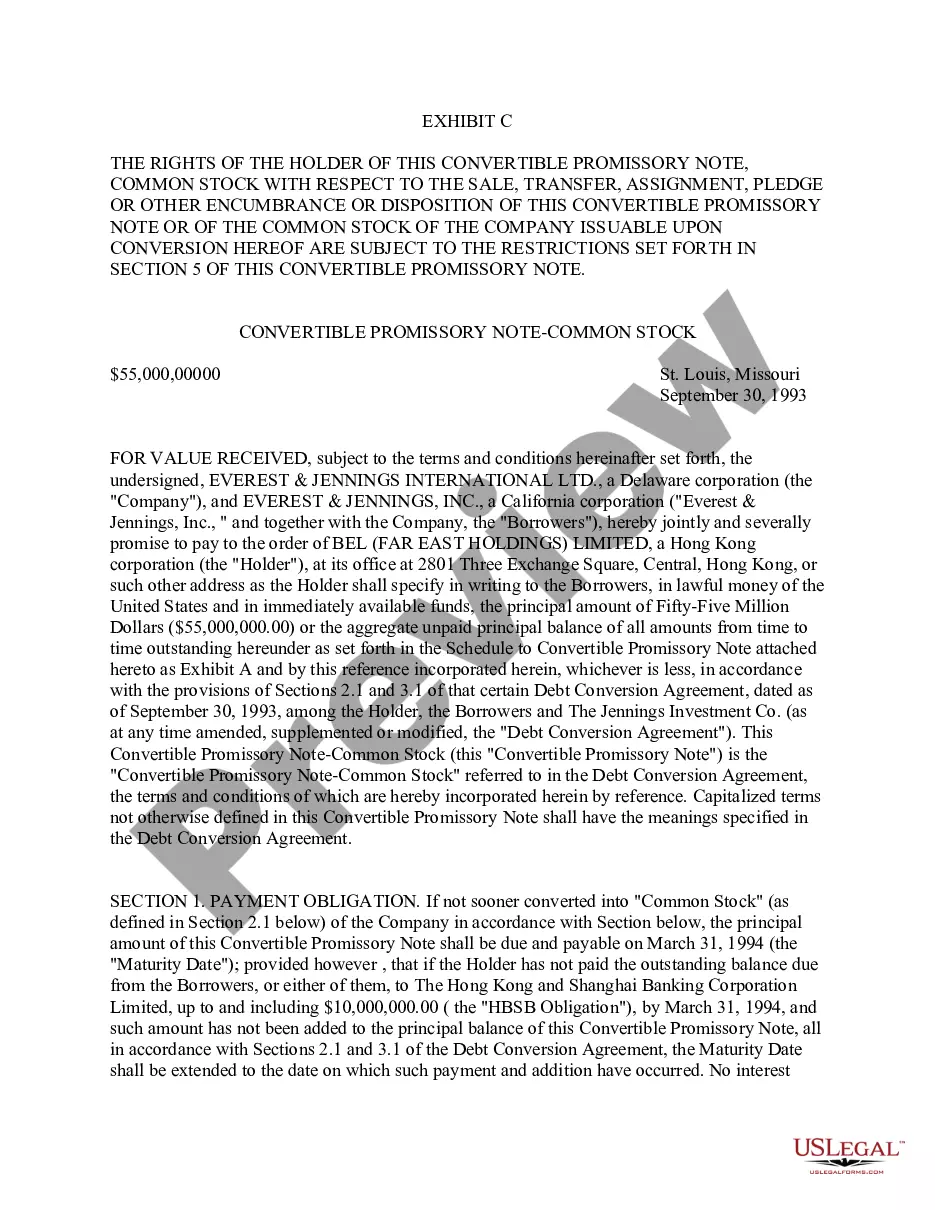

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

The Promissory Issued Agreement Forbearance displayed on this site is a reusable legal template created by experienced attorneys according to federal and local laws.

For over 25 years, US Legal Forms has offered individuals, companies, and legal practitioners access to more than 85,000 authenticated, state-specific documents for any business and personal situation.

Re-download your documents when necessary. Access the 'My documents' section in your account to retrieve any previously downloaded templates. Enroll in US Legal Forms to have confirmed legal templates for every situation in life readily available.

- Search for the document you need and examine it.

- Browse through the sample you looked for and preview it or review the form details to ensure it meets your needs. If it doesn't, use the search function to find the correct one. Click 'Buy Now' once you have identified the template you require.

- Select and Log In.

- Choose the pricing option that fits your requirements and create an account. Utilize PayPal or a credit card for a fast payment. If you already possess an account, Log In and verify your subscription to continue.

- Obtain the fillable template.

- Choose the file format you desire for your Promissory Issued Agreement Forbearance (PDF, DOCX, RTF) and download the document onto your device.

- Complete and sign the documents.

- Print the template to fill it out manually. Alternatively, use an online multifunctional PDF editor to quickly and accurately fill out and sign your form digitally.

Form popularity

FAQ

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

Key takeaways Mortgage forbearance allows a borrower to temporarily stop making payments or make smaller payments amid financial hardship. Mortgage forbearance typically lasts three to six months. The borrower is still responsible for making full mortgage payments after the forbearance period ends.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

Forbearance is the intentional action of abstaining from doing something. In the context of the law, it refers to the act of delaying from enforcing a right, obligation, or debt. For example, a creditor may forbear legal action against the debtor if they settle the debt payment with new payment conditions.

Forbearance is when your mortgage servicer, that's the company that sends your mortgage statement and manages your loan, or lender allows you to pause or reduce your payments for a limited period of time. Forbearance does not erase what you owe. You'll have to repay any missed or reduced payments in the future.