Promissory Corporation Notes With 50

Description

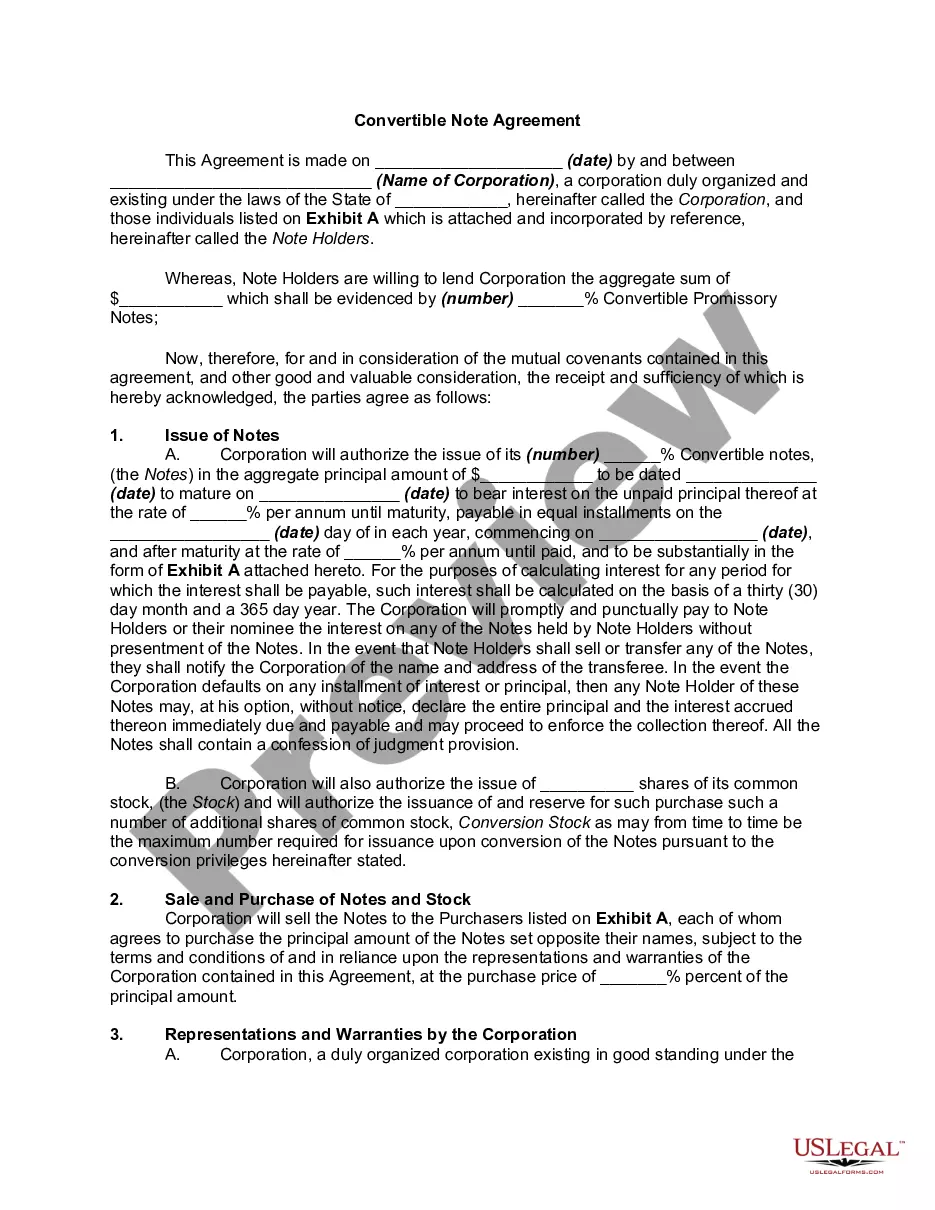

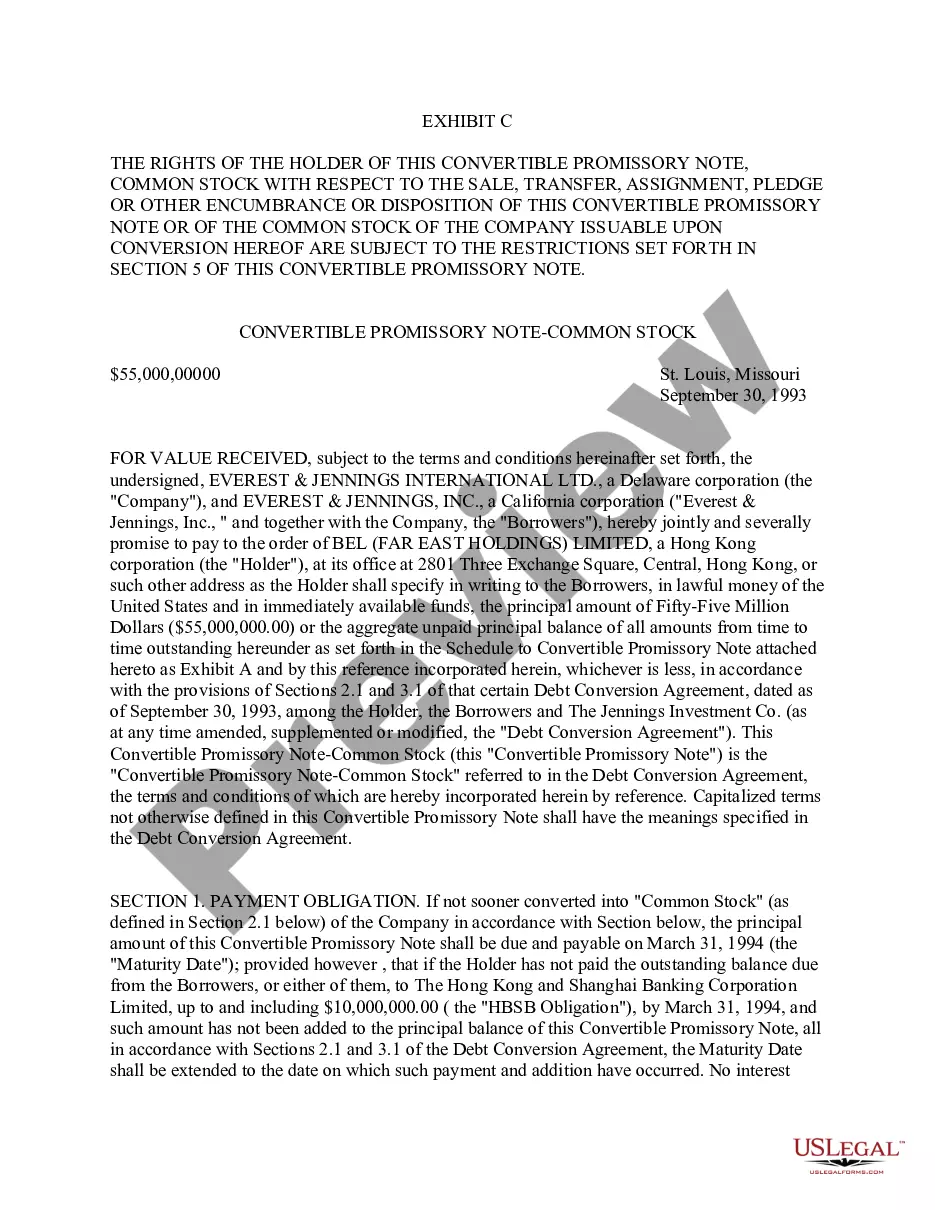

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

Whether for commercial reasons or personal issues, everyone must confront legal matters at some point in their lives. Completing legal documents requires meticulous attention, starting with selecting the appropriate form template. For example, if you choose an incorrect version of the Promissory Corporation Notes With 50, it will be declined upon submission. Thus, it is vital to obtain a trustworthy source of legal documents like US Legal Forms.

If you need to acquire a Promissory Corporation Notes With 50 template, adhere to these straightforward steps.

With a comprehensive US Legal Forms catalog available, you will never need to waste time searching for the correct template online. Utilize the library’s user-friendly navigation to find the appropriate form for any occasion.

- Locate the template you require using the search bar or catalog navigation.

- Review the form’s description to confirm it suits your needs, state, and county.

- Click on the form’s preview to examine it.

- If it is the incorrect form, return to the search feature to find the Promissory Corporation Notes With 50 template you require.

- Obtain the file when it aligns with your requirements.

- If you possess a US Legal Forms account, simply click Log in to access previously saved documents in My documents.

- If you do not have an account yet, you can download the form by clicking Buy now.

- Choose the appropriate pricing option.

- Complete the account registration form.

- Select your payment method: you can use a credit card or PayPal account.

- Choose the document format you prefer and download the Promissory Corporation Notes With 50.

- Once it is saved, you can fill out the form using editing software or print it and complete it manually.

Form popularity

FAQ

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

All Promissory Notes are valid only for a period of 3 years starting from the date of execution, after which they will be invalid. There is no maximum limit in terms of the amount which can be lent or borrowed. The issuer / lender of the funds is normally the one who will hold the Promissory Note.

If a lender did not sue on the promissory note within six years of the date of the loan, the claim was barred by the Limitation Act. Six years was the applicable limitation period. However, the same was not so for promissory notes for contingent loans.

While each state has its rules governing what must be in the document, standard items that you may expect to see within a promissory note include: Borrower's name and contact information. Lender details and contact information. Total amount of money to be borrowed.

You'll also include the promissory note payment terms, such as: The amount of each payment. You can require periodic payments at certain times, such as monthly. Or, repayment can be in a lump sum. When payments are due. The address where payments should be sent. Penalties for late payments.