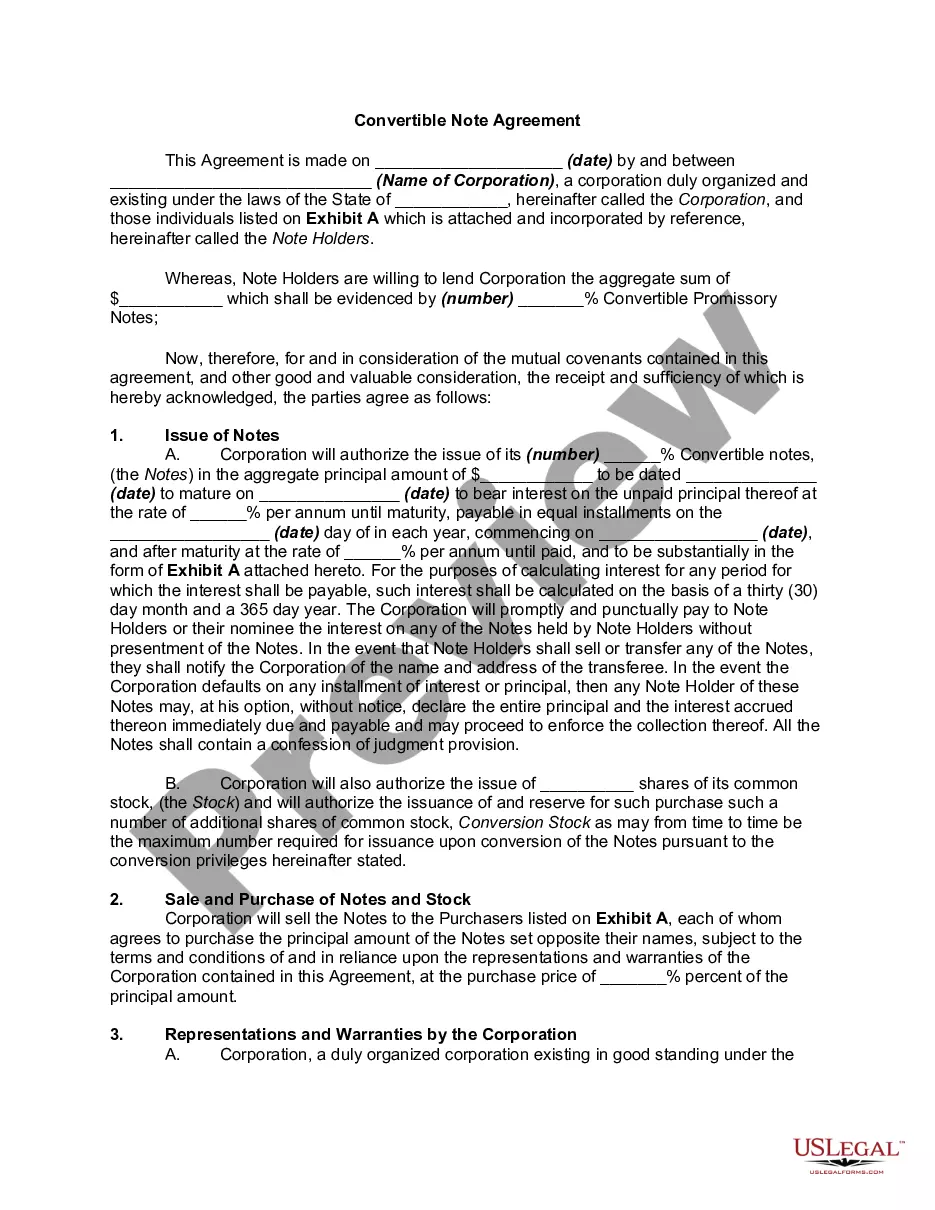

Convertible Promissory Note With Personal Guarantee Template

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

Steering through the red tape of official documents and templates can be challenging, particularly if one does not engage in that professionally.

Even selecting the appropriate template to acquire a Convertible Promissory Note With Personal Guarantee Template can be time-intensive, as it must be accurate and precise to the last detail.

However, you'll require significantly less time seeking a suitable template from a reliable source.

Acquire the appropriate form in a few straightforward steps: Enter the document name in the search field. Locate the right Convertible Promissory Note With Personal Guarantee Template in the results list. Review the sample outline or view its preview. When the template meets your requirements, click Buy Now. Proceed to select your subscription option. Use your email and establish a secure password to register at US Legal Forms. Choose a credit card or PayPal for payment. Save the template document to your device in the desired format. US Legal Forms can spare you time and energy verifying if the form you found online is appropriate for your needs. Establish an account and gain unlimited access to all the templates you require.

- US Legal Forms is a platform that streamlines the process of locating the correct forms online.

- US Legal Forms is a singular destination where you can find the latest examples of forms, learn about their usage, and download these examples to complete them.

- It is a repository comprising over 85K forms applicable in various sectors.

- When searching for a Convertible Promissory Note With Personal Guarantee Template, you won't have to doubt its authenticity, as all the forms are validated.

- Having an account at US Legal Forms will guarantee you have all the necessary samples at your fingertips.

- You can store them in your history or add them to the My documents collection.

- Access your saved forms from any device by clicking Log In on the library website.

- If you have not yet created an account, you can always search for the template you require.

Form popularity

FAQ

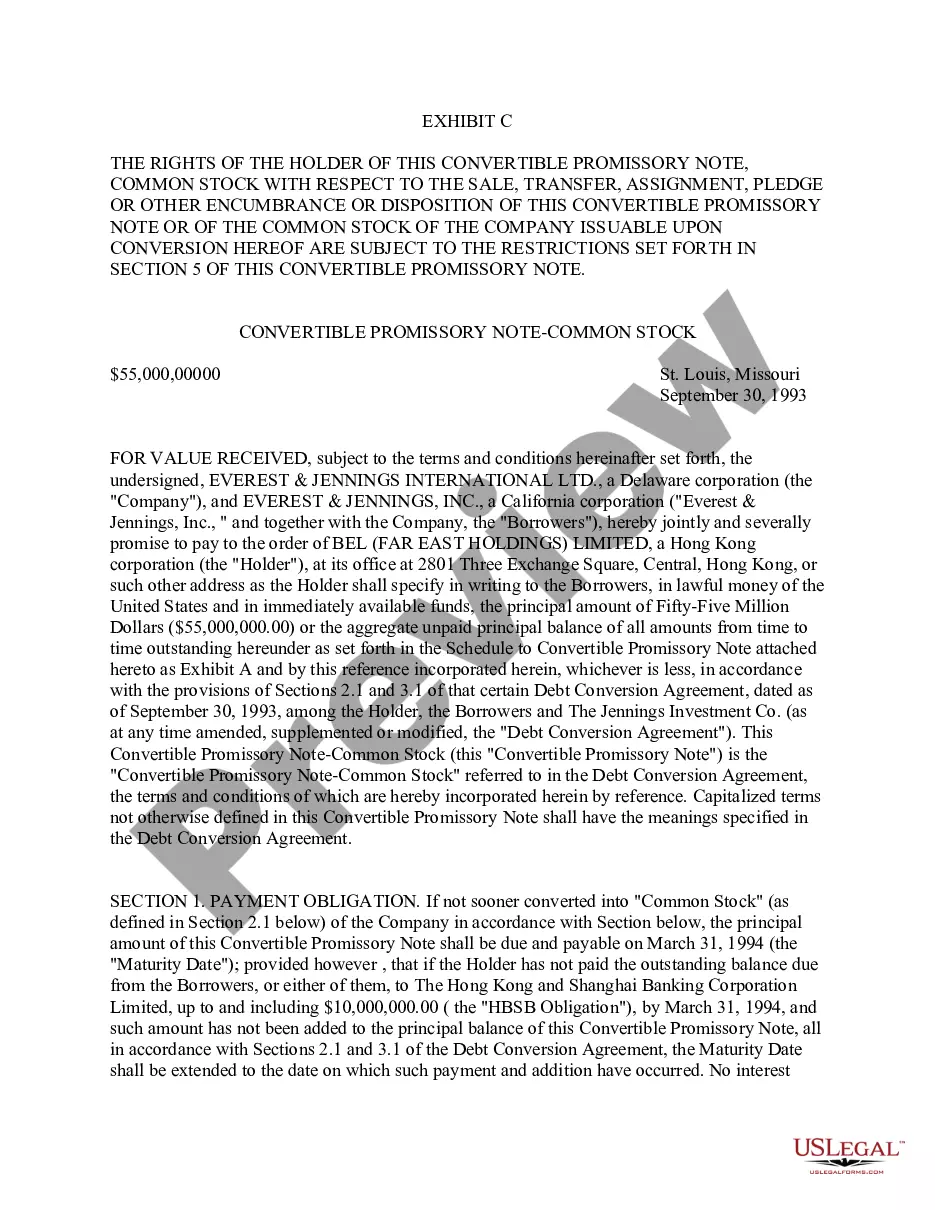

In almost all cases, your bank debt will be secured (see the Q&A above regarding security interests) and your convertible notes will be unsecured.

A Convertible Note is a type of financial document, which allows companies to exchange equity or other non-tangible assets for a typically short-term loan.

Also known as convertible promissory notes, bridge notes, or convertible debt. Since convertible notes are securities, they must be registered, or qualify for an exemption from registration, under the Securities Act.

Convertible notes are promissory notes that serve an additional business purpose other than merely representing debt. Convertible notes include all of the terms of a vanilla promissory note, such as an interest rate and the pledge of underlying security (if applicable).

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.19-Aug-2021