Garnishment Hardship Form With 401

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

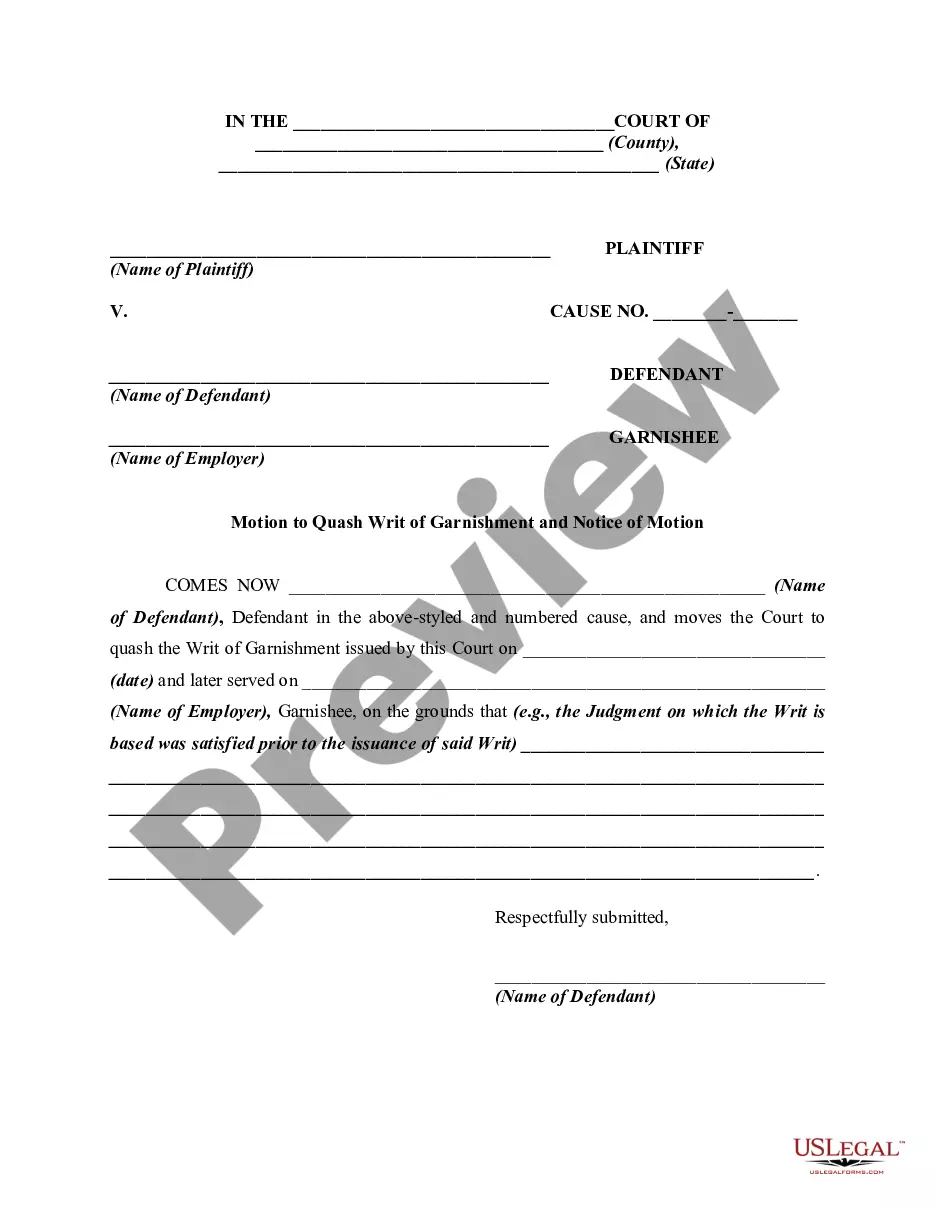

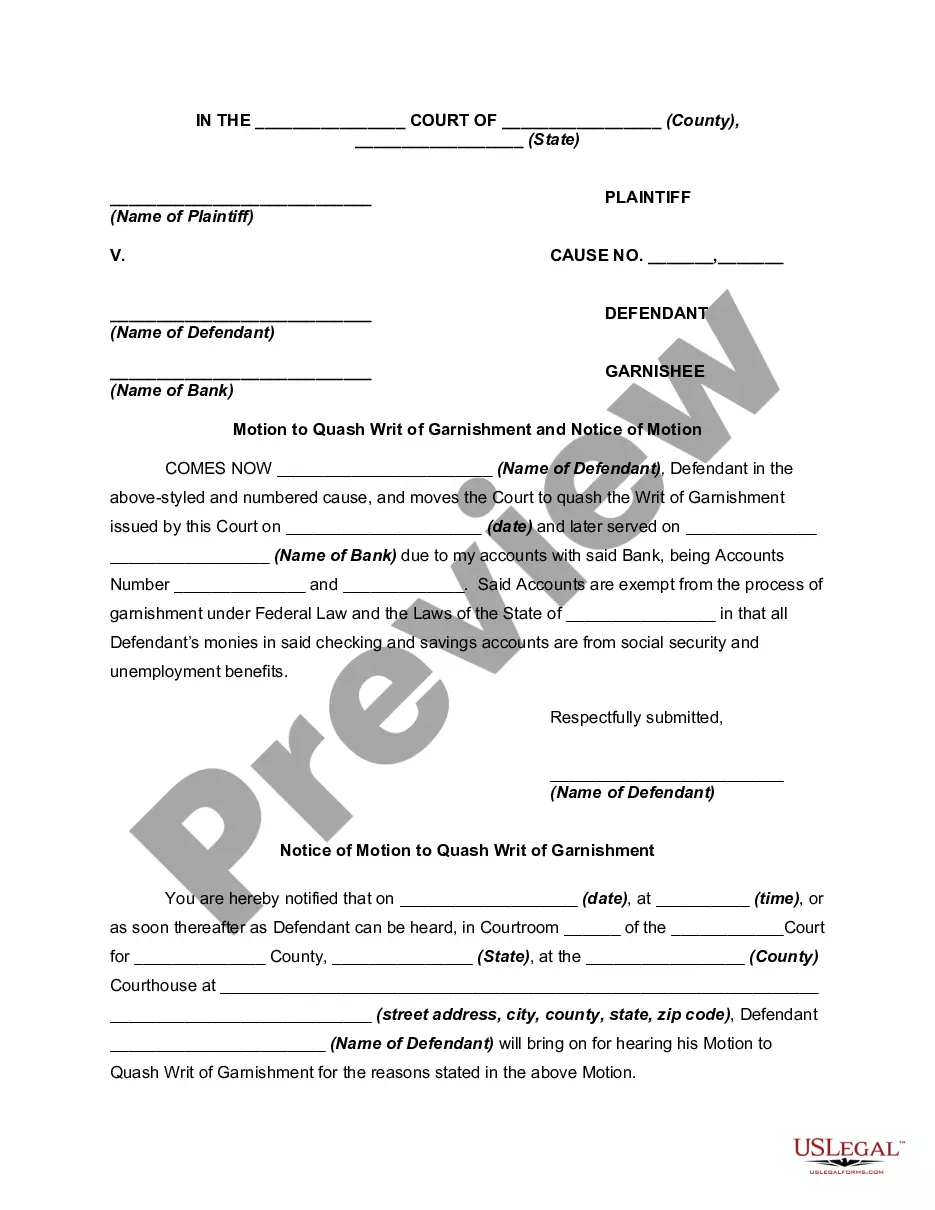

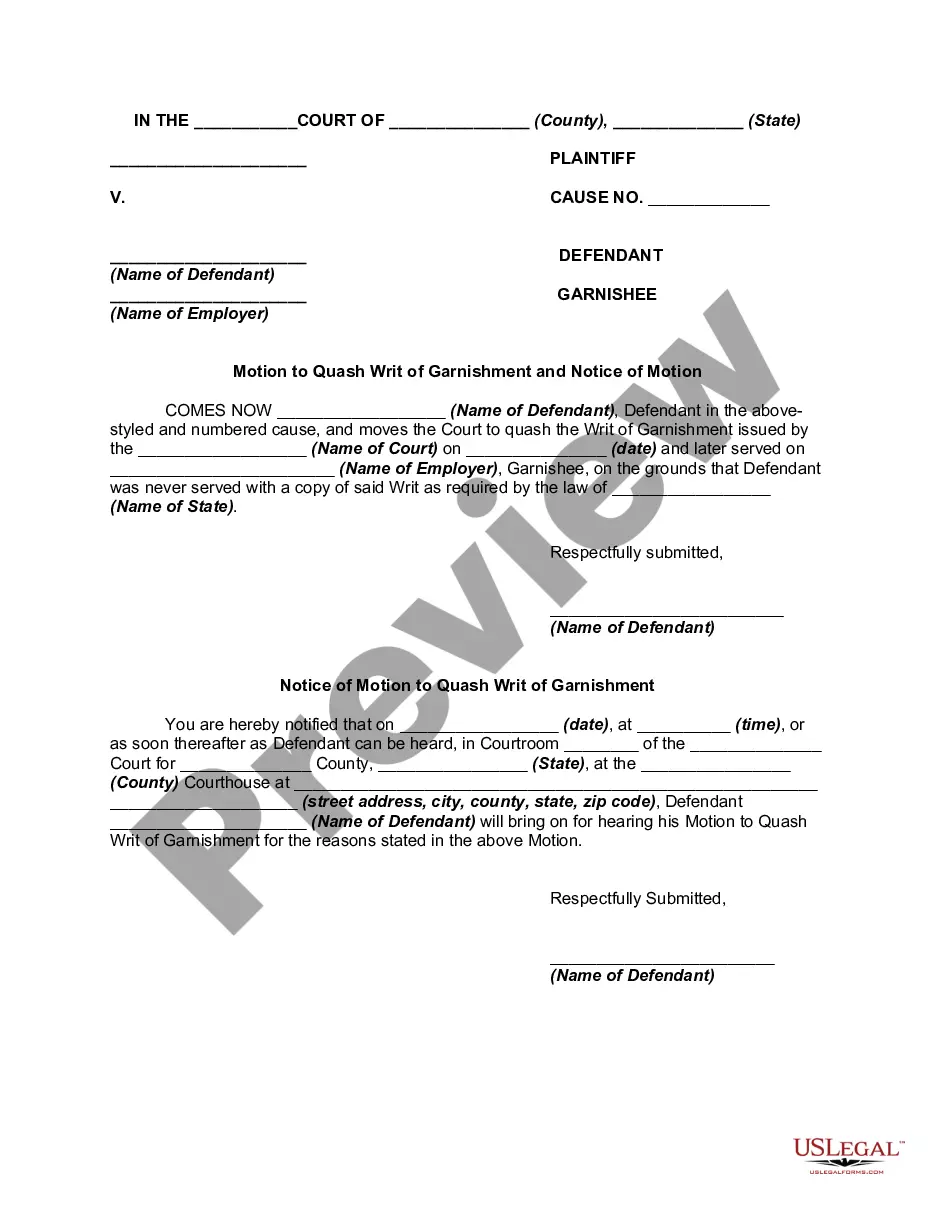

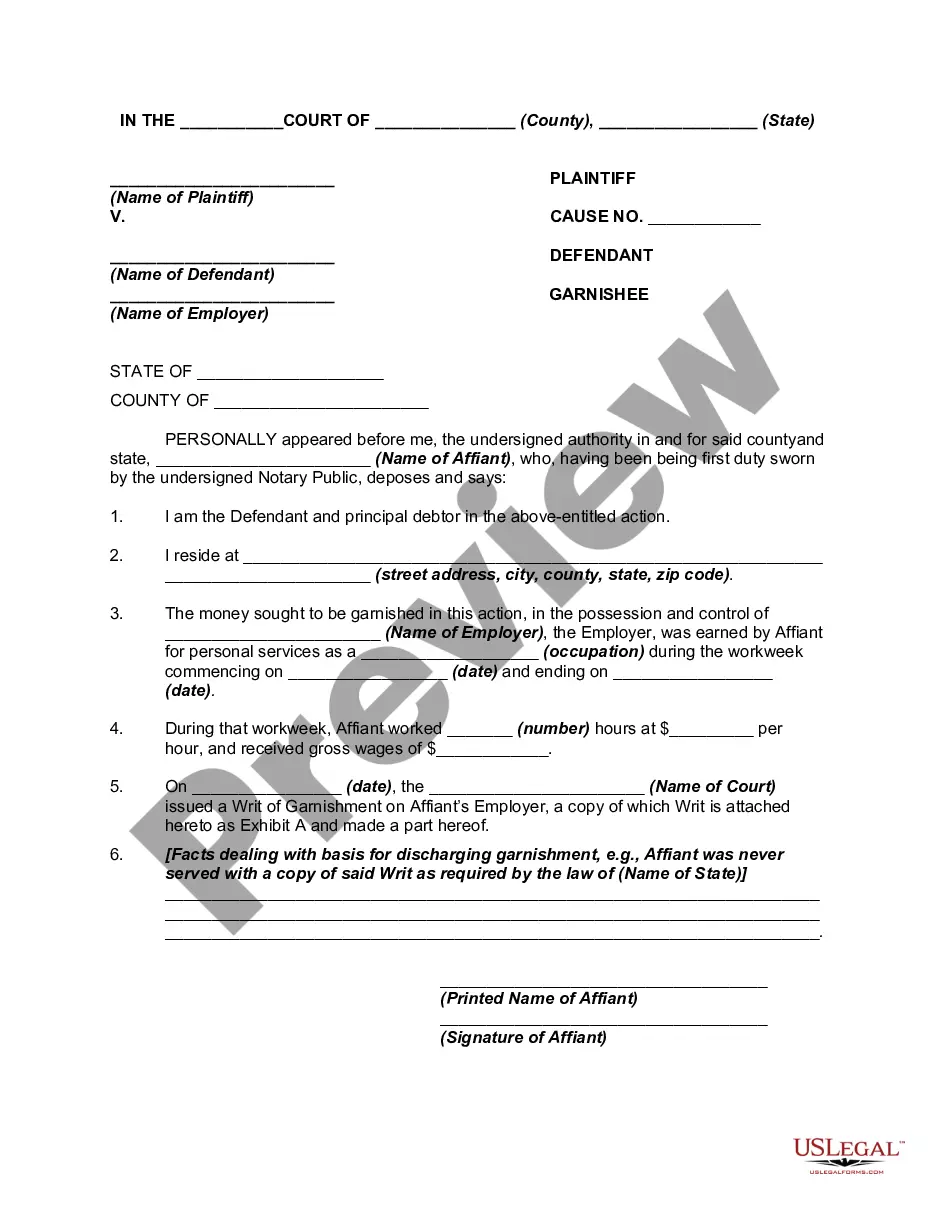

How to fill out Motion To Discharge Or Quash Writ Of Garnishment?

Locating a reliable source for the latest and most suitable legal documents is part of the challenge when dealing with bureaucracy.

Selecting the appropriate legal forms requires accuracy and consideration, which is why it’s essential to obtain examples of the Garnishment Hardship Form With 401 exclusively from reputable providers, such as US Legal Forms. A faulty template will consume your time and delay your current situation. With US Legal Forms, you can feel reassured.

Once you have the form on your device, you can modify it with the editor or print it and complete it manually. Eliminate the stress associated with your legal paperwork. Explore the comprehensive US Legal Forms catalog to discover legal documents, verify their relevance to your situation, and download them instantly.

- Utilize the library navigation or search option to find your template.

- Examine the form's description to ensure it aligns with the laws of your state and area.

- Preview the form, if accessible, to confirm it is indeed what you need.

- If the Garnishment Hardship Form With 401 does not meet your requirements, continue searching for the appropriate document.

- Once you’re certain of the form’s suitability, download it.

- If you are a member, click Log in to verify your account and access your selected templates in My documents.

- If you are not yet a member, click Buy now to purchase the form.

- Choose the pricing plan that best fits your needs.

- Proceed to register to complete your transaction.

- Finalize your order by selecting a payment option (credit card or PayPal).

- Choose the document format to download the Garnishment Hardship Form With 401.

Form popularity

FAQ

You may need to share proof of the hardship event and show that you don't have insurance or other assets and can't qualify for a loan before you receive the hardship withdrawal. Your employer may also want to verify that you can't cover the hardship by stopping your 401(k) contributions.

You may need to share proof of the hardship event and show that you don't have insurance or other assets and can't qualify for a loan before you receive the hardship withdrawal. Your employer may also want to verify that you can't cover the hardship by stopping your 401(k) contributions.

To qualify for a hardship distribution, a 401(k) participant must meet two criteria. First, they must have an ?immediate and heavy financial need.? Second, the distribution must be limited to the amount ?necessary to satisfy? the financial need.

To make a 401(k) hardship withdrawal, you will need to contact your employer and plan administrator and request the withdrawal. The administrator will likely require you to provide evidence of the hardship, such as medical bills or a notice of eviction.

The general answer is no, a creditor cannot seize or garnish your 401(k) assets. 401(k) plans are governed by a federal law known as ERISA (Employee Retirement Income Security Act of 1974). Assets in plans that fall under ERISA are protected from creditors.