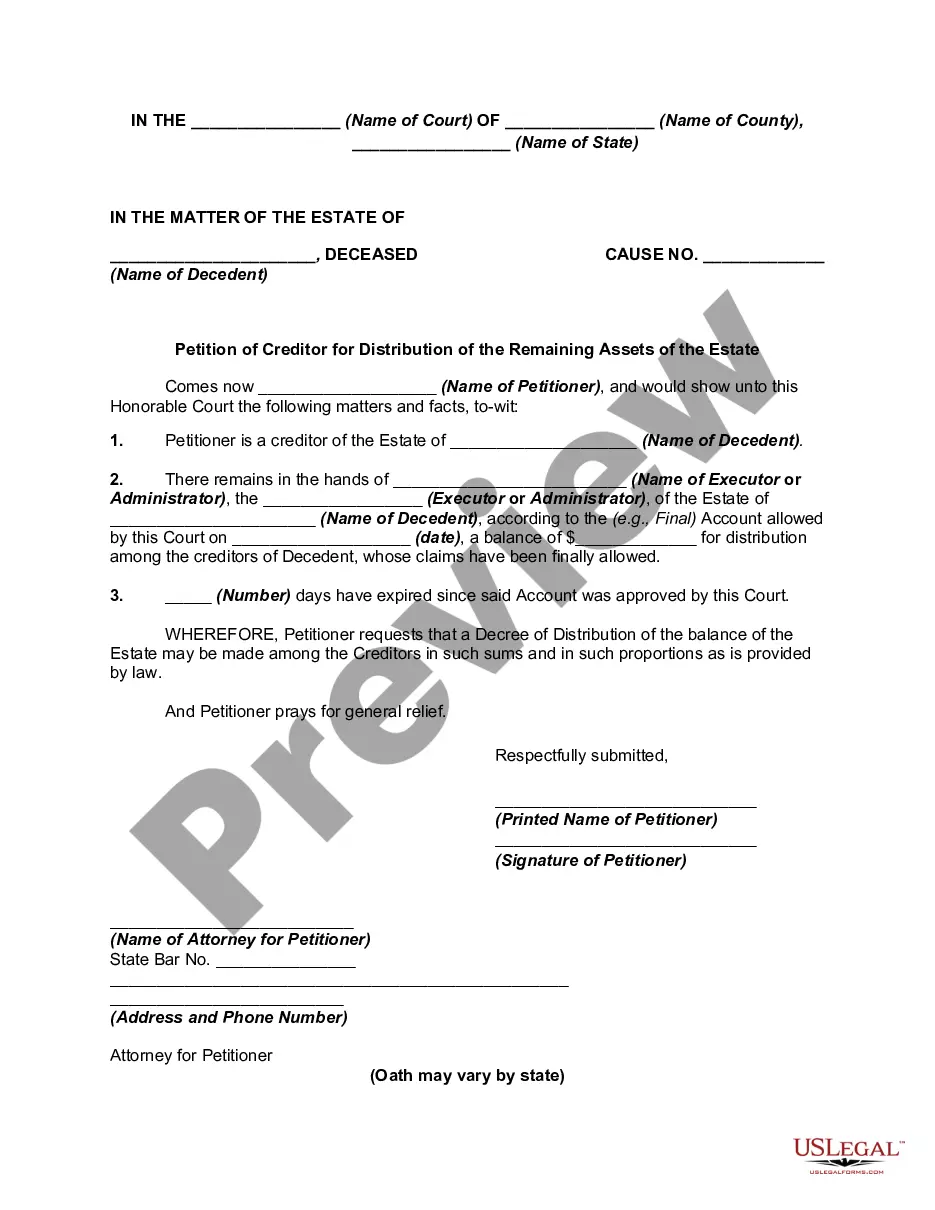

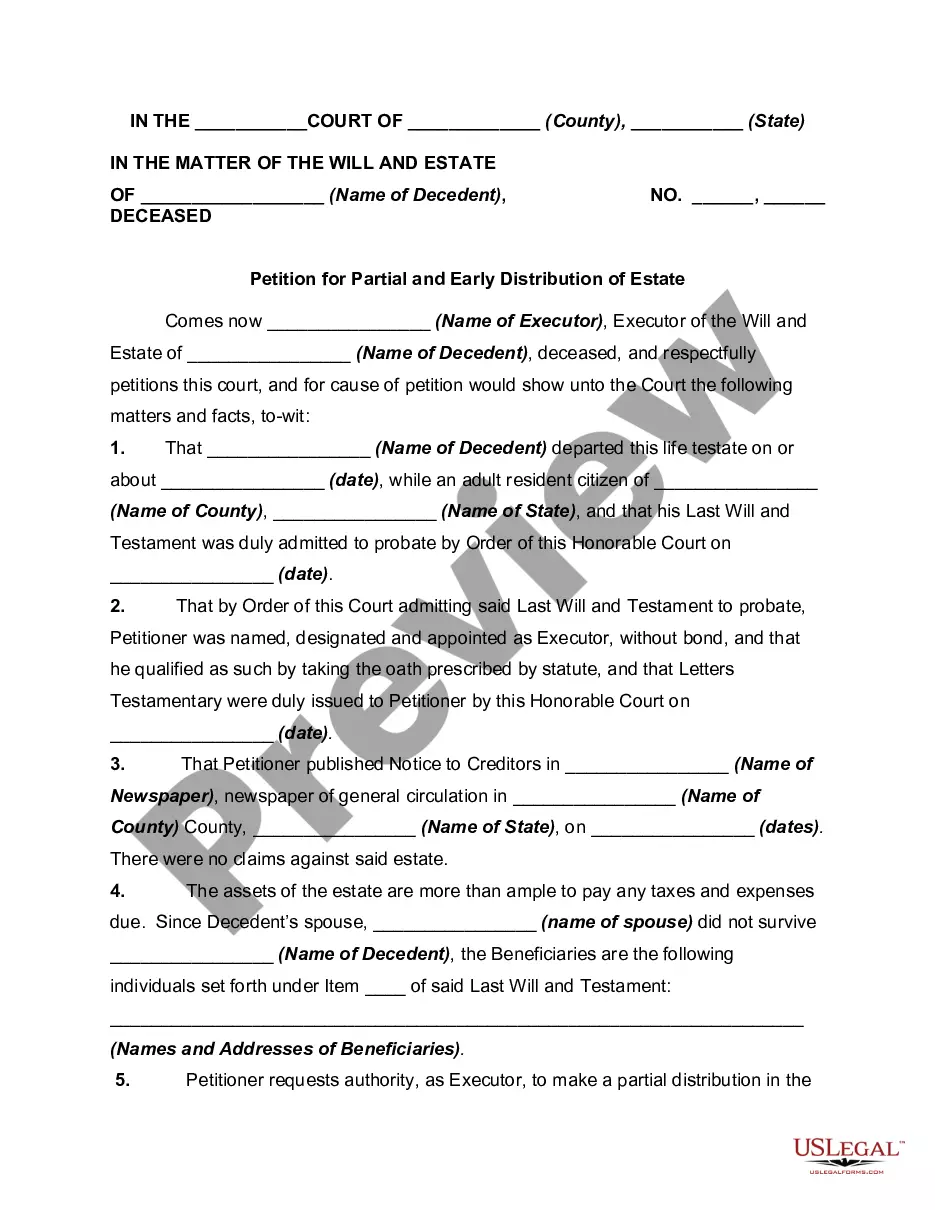

Distribution Assets Form For Government Employees

Description

How to fill out Petition To Determine Distribution Rights Of The Assets Of A Decedent?

It’s obvious that you can’t become a law expert overnight, nor can you learn how to quickly draft Distribution Assets Form For Government Employees without the need of a specialized set of skills. Putting together legal forms is a long process requiring a particular education and skills. So why not leave the preparation of the Distribution Assets Form For Government Employees to the specialists?

With US Legal Forms, one of the most comprehensive legal document libraries, you can access anything from court papers to templates for in-office communication. We understand how important compliance and adherence to federal and state laws are. That’s why, on our website, all forms are location specific and up to date.

Here’s start off with our platform and get the form you require in mere minutes:

- Discover the form you need with the search bar at the top of the page.

- Preview it (if this option available) and check the supporting description to determine whether Distribution Assets Form For Government Employees is what you’re looking for.

- Begin your search over if you need any other form.

- Register for a free account and choose a subscription plan to purchase the template.

- Choose Buy now. Once the transaction is complete, you can download the Distribution Assets Form For Government Employees, fill it out, print it, and send or mail it to the designated individuals or entities.

You can re-access your forms from the My Forms tab at any time. If you’re an existing client, you can simply log in, and locate and download the template from the same tab.

Regardless of the purpose of your paperwork-be it financial and legal, or personal-our platform has you covered. Try US Legal Forms now!

Form popularity

FAQ

Code 1 is used for early withdrawal from the plan. This means an investor is withdrawing funds from their retirement before they've entered into retirement. There can be many reasons why an investor might do an early withdrawal of funds from their retirement. Common reasons are a financial or medical emergency.

You'll most likely report amounts from Form 1099-R as ordinary income on line 4b and 5b of the Form 1040. The 1099-R form is an informational return, which means you'll use it to report income on your federal tax return.

Once you start withdrawing from your 401(k) or traditional IRA, your withdrawals are taxed as ordinary income. You'll report the taxable part of your distribution directly on your Form 1040. Keep in mind, the tax considerations for a Roth 401(k) or Roth IRA are different.

What is a qualified (tax-free) Roth 403(b) distribution? To qualify for tax-free distributions from your Roth 403(b), you must meet the following requirements: Age 59½, death, or disability, and. Hold account for five years.

When are penalty-free distributions from my 403(b) account available? Current IRS regulations allow withdrawals of 403(b) monies, without penalties, when you: Reach age 59½, Retire or separate from service during the year in which you reach age 55 or later,***