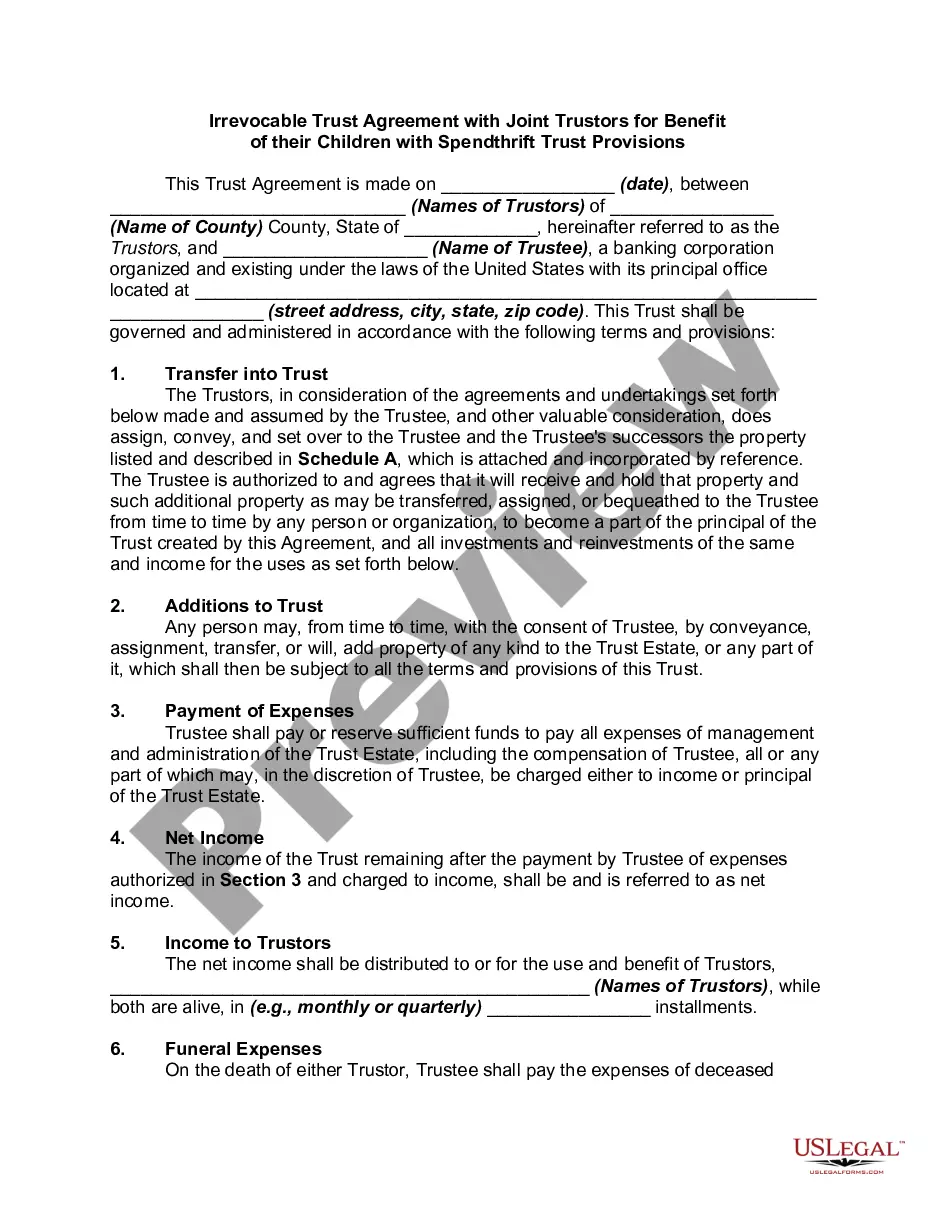

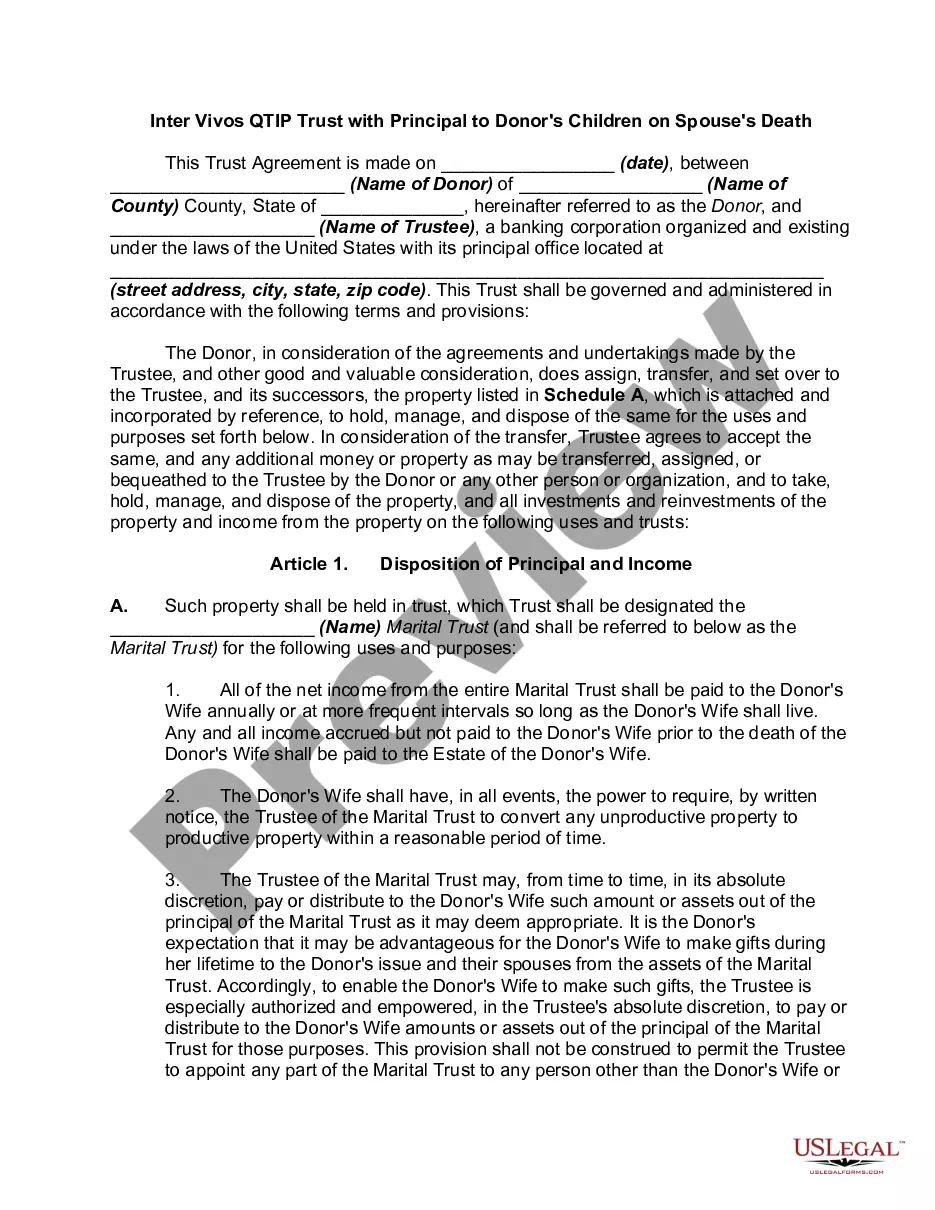

Irrevocable Grantor Trusts With A Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Trust Agreement For Benefit Of Trustor's Children And Grandchildren With Spendthrift Trust Provisions?

- If you are a returning user, log in to your account to access previously downloaded forms.

- To start fresh, first browse the library and click on the Preview mode to review the form description. Ensure it aligns with your jurisdiction's requirements.

- If you find inconsistencies or require a different document, utilize the Search tab to locate the appropriate template.

- Once you find the correct form, click on the Buy Now button and select a subscription plan that suits you. Create an account to access the resources.

- Proceed to payment by entering your credit card details or signing in with your PayPal account.

- Finally, download the form to your device, and you can access it anytime in the My Forms section of your profile.

By using US Legal Forms, individuals and attorneys can quickly and easily draft legal documents that are precise and compliant with the law.

Don't hesitate; start your journey toward creating irrevocable grantor trusts with a trust today by visiting US Legal Forms!

Form popularity

FAQ

Putting assets in a trust can lead to potential downsides, such as reduced access to those assets for the grantor. Once you transfer assets into irrevocable grantor trusts with a trust, you cannot easily retrieve them or control their management. Moreover, the initial setup costs may be seen as a disadvantage by some individuals, but the long-term benefits often outweigh these concerns.

A major mistake parents often make when establishing a trust fund is not clearly communicating their intentions to their children. This lack of communication can lead to misunderstandings and disputes later. Additionally, failing to properly fund the irrevocable grantor trusts with a trust can render the intended benefits ineffective, so careful planning is essential.

Reporting income from an irrevocable grantor trust involves including the trust’s income on your personal tax return, as it is still considered part of your income. The trust must provide a Schedule K-1 that details the income distribution you must report. Understanding these reporting requirements can be complex, but utilizing resources like US Legal Forms can simplify the process.

Filling out an irrevocable trust involves several steps, starting with identifying the assets to be placed in the trust. Next, working with a qualified attorney can help ensure that all legal requirements are met. Form templates, like those available on US Legal Forms, can guide you through the process, making it straightforward and compliant with state laws.

One notable disadvantage of a family trust is the complexity involved in managing it. When family members are the trustees, conflicts can arise, potentially complicating decision-making. Furthermore, establishing irrevocable grantor trusts with a trust can incur costs, including legal fees and maintenance expenses, which can be a concern for some families.

Yes, an irrevocable trust can indeed be classified as a grantor trust under specific circumstances. This means that the person who creates the trust still retains certain powers, leading to taxable income on the grantor's personal tax return. This setup allows for certain tax benefits while still providing the protection features of irrevocable grantor trusts with a trust.

If your parents have substantial assets, establishing irrevocable grantor trusts with a trust can be a wise decision. This arrangement may help in shielding their assets from creditors and potential lawsuits. Moreover, it can facilitate smoother estate planning and inheritance processes for beneficiaries by bypassing probate court.

One significant downfall of having irrevocable grantor trusts with a trust is the loss of control over the assets. Once the trust is established, you cannot change the terms or revoke it, which can pose challenges if your personal circumstances change. Additionally, there may be costs associated with setting up and maintaining the trust, such as legal fees and ongoing administration expenses.

Ownership of assets in an irrevocable trust is held by the trust itself, not the grantor. Once the grantor transfers assets into the trust, they relinquish control and ownership. This setup provides advantages such as asset protection from creditors and potential estate tax benefits. If you're navigating the intricacies of irrevocable trusts, US Legal Forms can provide the forms necessary to simplify the journey.

To make an irrevocable trust a grantor trust, specific provisions need to be included in the trust document that grant the grantor certain powers. These may involve control over the trust’s income or the ability to change beneficiaries. It’s important to carefully outline these powers to comply with IRS regulations. When you look for guidance on this process, consider exploring options at US Legal Forms for valuable resources.