Default Promissory Note Form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice Of Default In Payment Due On Promissory Note?

Individuals generally link legal documents with complexity that solely an expert can manage. In a certain sense, this is accurate, as creating a Default Promissory Note Form requires comprehensive understanding of subject matter criteria, including regional and local laws.

However, with US Legal Forms, the process has become simpler: pre-made legal documents for any life or business scenario tailored to state regulations are compiled in a single online repository and are now accessible to everyone.

US Legal Forms offers over 85,000 current documents categorized by state and purpose of use, allowing you to search for a Default Promissory Note Form or any specific template in just minutes. Existing users with an active subscription must Log In to their account and click Download to receive the document. New users need to create an account and subscribe prior to downloading any files.

All templates in our collection are reusable: once purchased, they remain saved in your profile. You can access them whenever necessary via the My documents tab. Experience all the benefits of utilizing the US Legal Forms platform. Subscribe now!

- Thoroughly review the page content to confirm it fulfills your requirements.

- Examine the form description or review it using the Preview option.

- If the first sample does not meet your needs, search for another using the Search field in the header.

- When you identify the correct Default Promissory Note Form, click Buy Now.

- Select a pricing plan that aligns with your needs and financial plan.

- Create an account or Log In to advance to the payment section.

- Complete your payment through PayPal or with your credit card.

- Choose the format of your document and click Download.

- Either print your document or upload it to an online editor for quicker completion.

Form popularity

FAQ

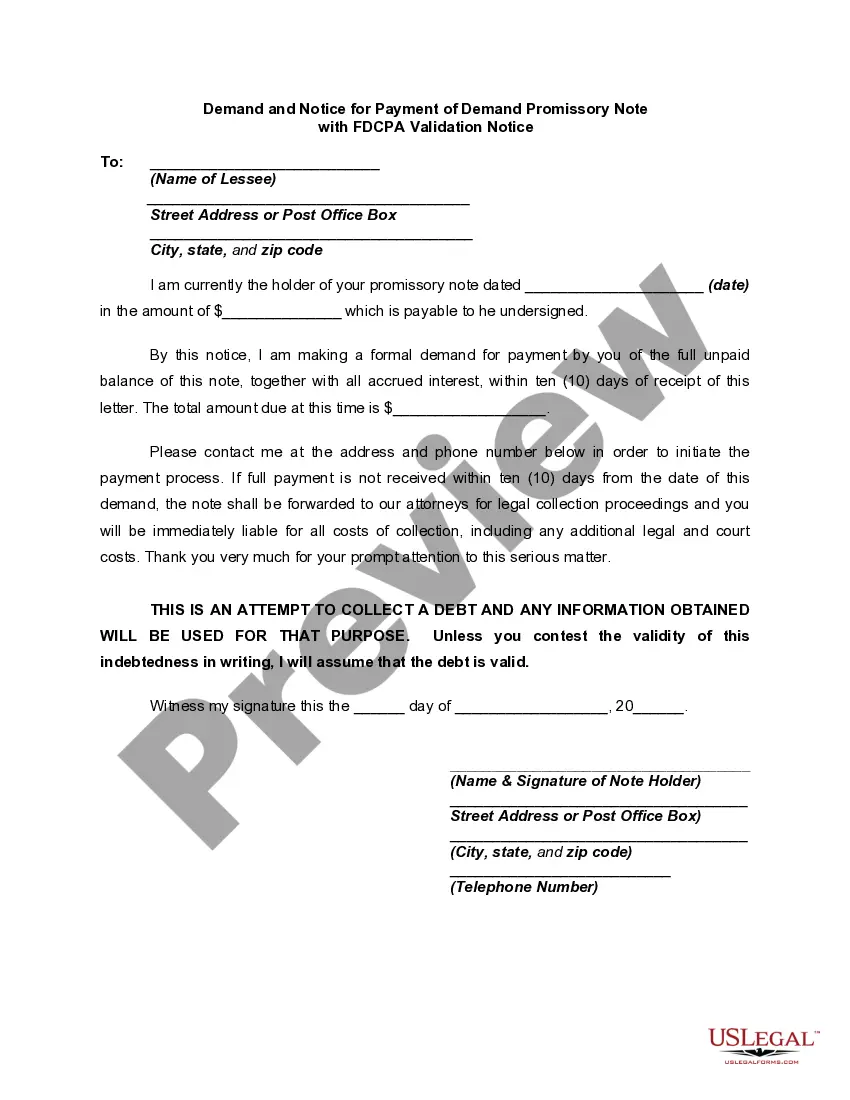

The first step in enforcing an unsecured promissory note is to file a petition with the courts and get a judgment in your favor. Although this is a powerful legal enforcement of your rights under the promissory note, it does not in and of itself guarantee repayment of the note.

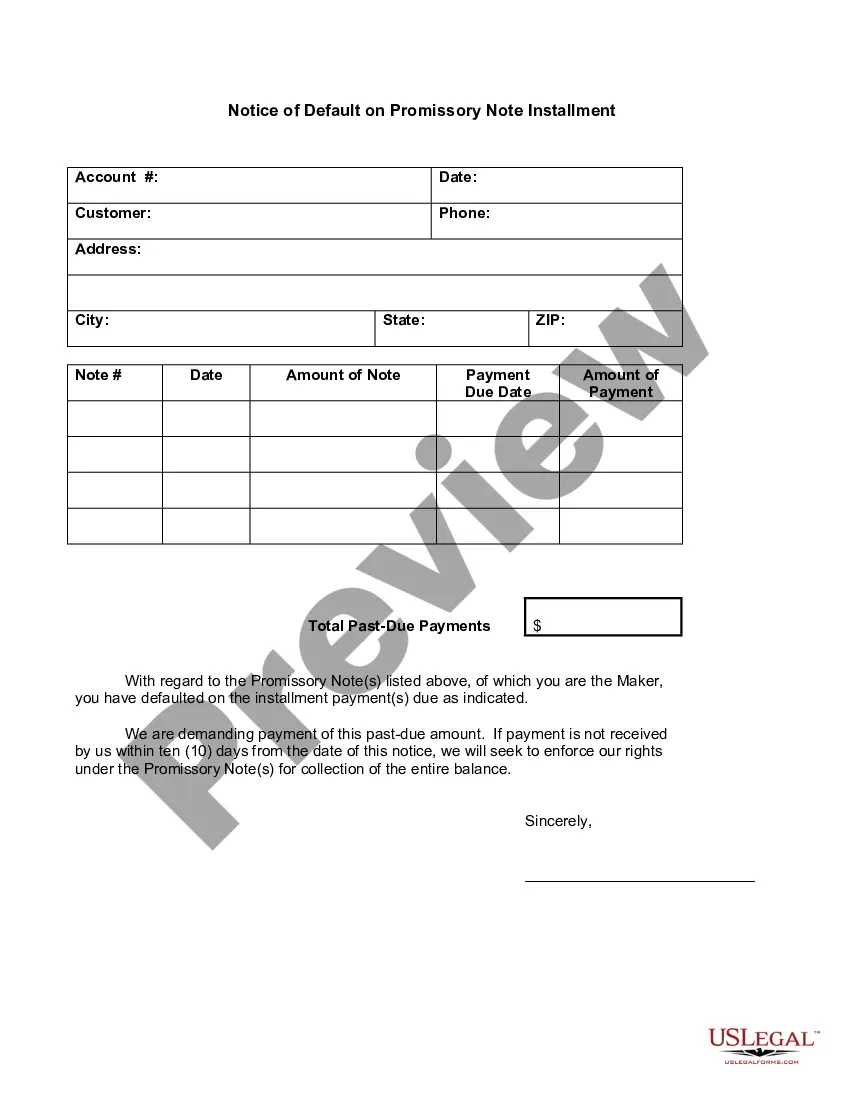

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

Detailed Information The note has all the required information including the name of the drawer and payee, date of maturity, terms of repayment, issue date, name of the drawee, name, and signature of the drawer, principal amount, and the rate of interest, etc.

A promissory note may include a default on secured debt as part of the agreement. This means that if the borrower fails to pay under the agreed-upon terms of the promissory note, then the lender can take the secured debt as a form of payment.

A default on a loan happens when the borrower fails to make the scheduled payments in full. Default could happen with one missed payment or might not occur until after several payments have been missed, depending on the terms of the note.