What Is A Mortgage Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

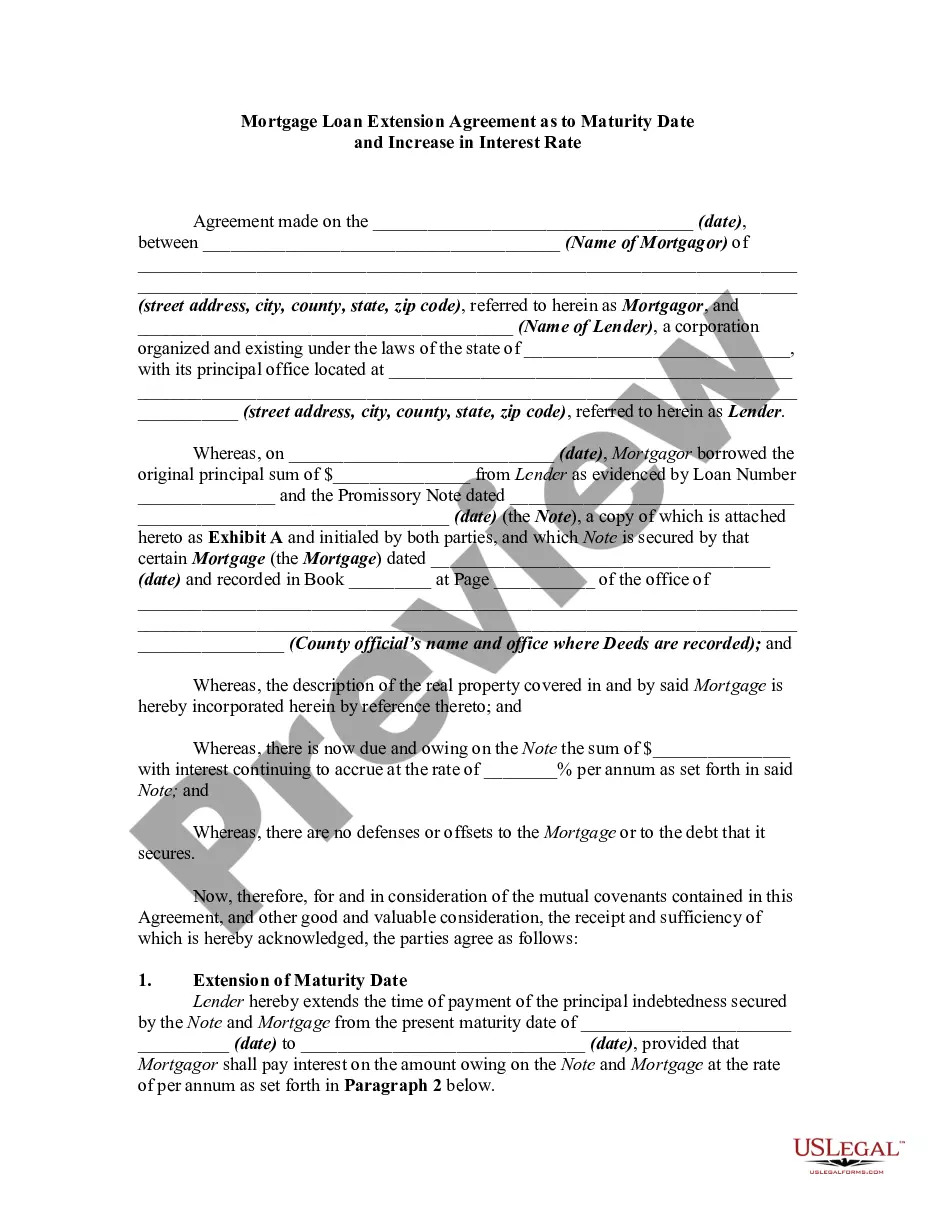

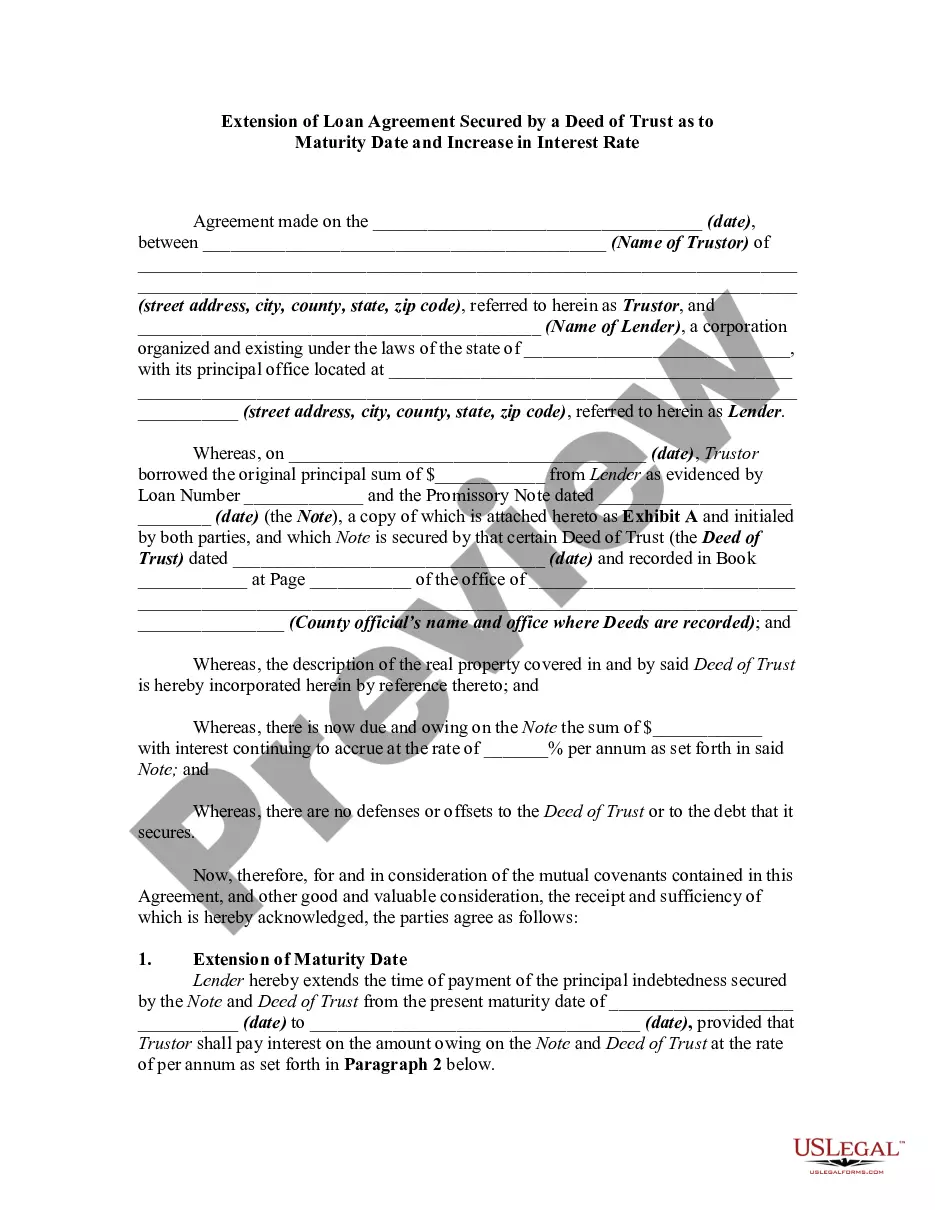

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

- Log into your US Legal Forms account if you've previously used the service. If you need the specific form again, simply click the Download button. Confirm that your subscription is active; if it has lapsed, renew it based on your payment plan.

- For first-time users, start by checking the Preview mode and read the form description to make sure it meets your needs and complies with your local jurisdiction.

- If you find that the selected template doesn’t fit your requirements, use the Search tab to find the correct document.

- Once you locate the right form, click on the Buy Now button and choose a suitable subscription plan. Registration is required to access the library's resources.

- Proceed with your purchase by entering your credit card information or using your PayPal account to finalize the subscription.

- After completing your purchase, download the form and save it on your device for easy access. You can revisit it anytime from the My Forms section of your profile.

Utilizing US Legal Forms gives you access to an extensive library of over 85,000 legal documents—more than competitors for similar costs. This service not only simplifies the process of obtaining legal forms but also connects you with premium experts for assistance, guaranteeing that your documents are both precise and legally sound.

In conclusion, understanding 'What is a mortgage agreement' can greatly impact your real estate journey. Leverage US Legal Forms for easy access to necessary documentation and expert assistance. Start your journey today!

Form popularity

FAQ

A mortgage in agreement refers to the specific terms outlined in a mortgage contract between a borrower and a lender. It details how much you will borrow, the interest rate, and the repayment schedule. This document serves to protect both parties' interests and ensures that the borrower understands their obligations. Knowing what a mortgage agreement entails is vital for successful home financing.

The length of a mortgage agreement typically ranges from 15 to 30 years. This time frame allows borrowers to spread out their payments over many years, making homeownership more manageable. You can choose a duration that aligns with your financial goals, which is crucial for your planning. Understanding how long your mortgage agreement lasts helps you prepare for future financial commitments.

A mortgage agreement typically consists of several sections, including borrower and lender information, property details, and repayment terms. It often includes clauses addressing interest rates, penalties, and foreclosure procedures. When using services like US Legal Forms, you can view customizable templates to understand the structure and content of a standard mortgage agreement.

You can obtain a mortgage agreement through various sources, including lenders such as banks or credit unions. Alternatively, you can use online platforms like US Legal Forms, which provide templates and guidance for creating your own mortgage agreement. It's essential to choose a reliable source to ensure your document meets legal standards and protects your interests.

You can obtain a copy of a mortgage note by contacting your lender or visiting the local county recorder’s office. Lenders keep records of the agreements, so they can often provide you with a copy if necessary. Familiarizing yourself with what is a mortgage agreement can help you ask the right questions when seeking this document.

To get a copy of a mortgage note, you can visit the county recorder’s office where the property is located. There, you can request to view or obtain copies of the document. Understanding what is a mortgage agreement will help you navigate this process, as you will better recognize the terms and stipulations contained in the note.

The 2 2 2 rule for mortgages is a simple guideline that highlights the key aspects to consider. This includes the two documents needed for application, two key things your lender will evaluate, and about two weeks as a typical timeline for processing. Understanding this rule can prepare you for your mortgage agreement journey.

When speaking with a mortgage lender, avoid making ambiguous statements about your financial situation. Do not imply that you have other ongoing debts or previous financial struggles without proper context. Maintaining clear and honest communication is vital, as it affects the terms of your mortgage agreement.

To fill out a mortgage form, begin by entering your personal details, including your income and assets. Then, specify the property information and the amount you wish to borrow. Take your time, and if you need guidance, platforms like US Legal Forms offer templates that can help you create your mortgage agreement accurately.