Aviso Desalojo Withdrawn

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

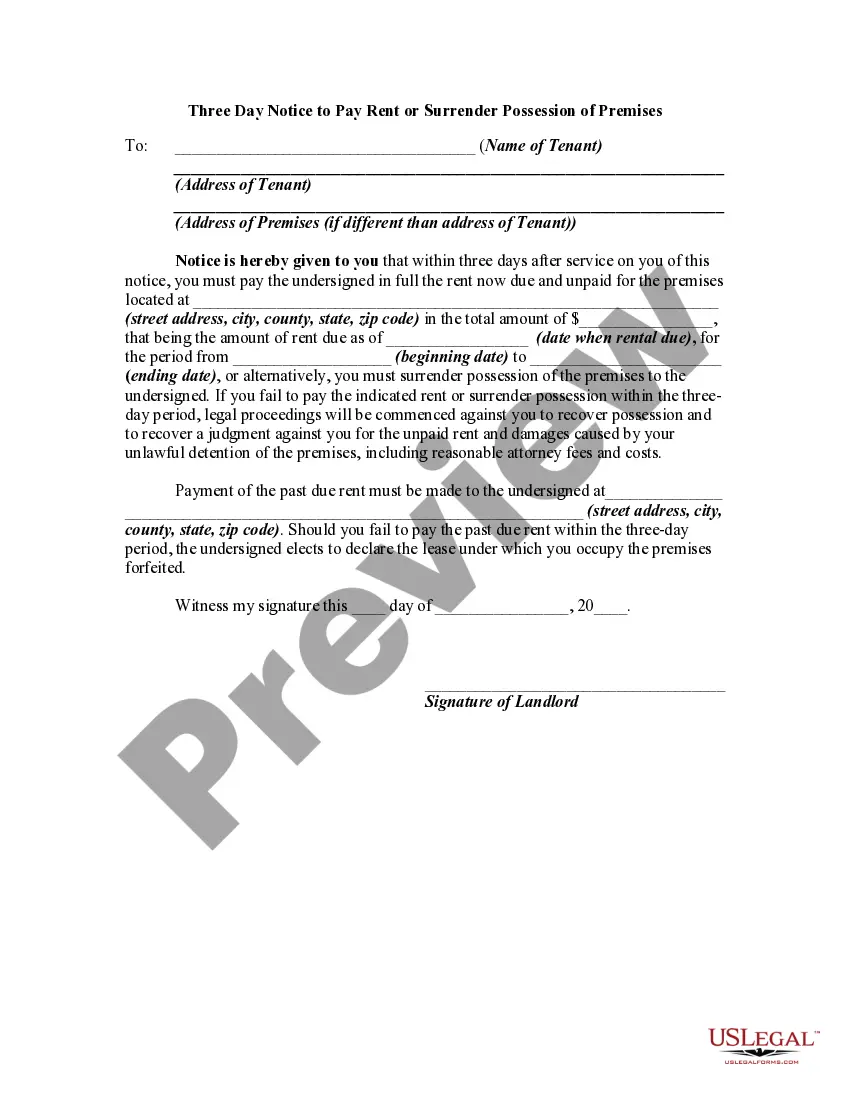

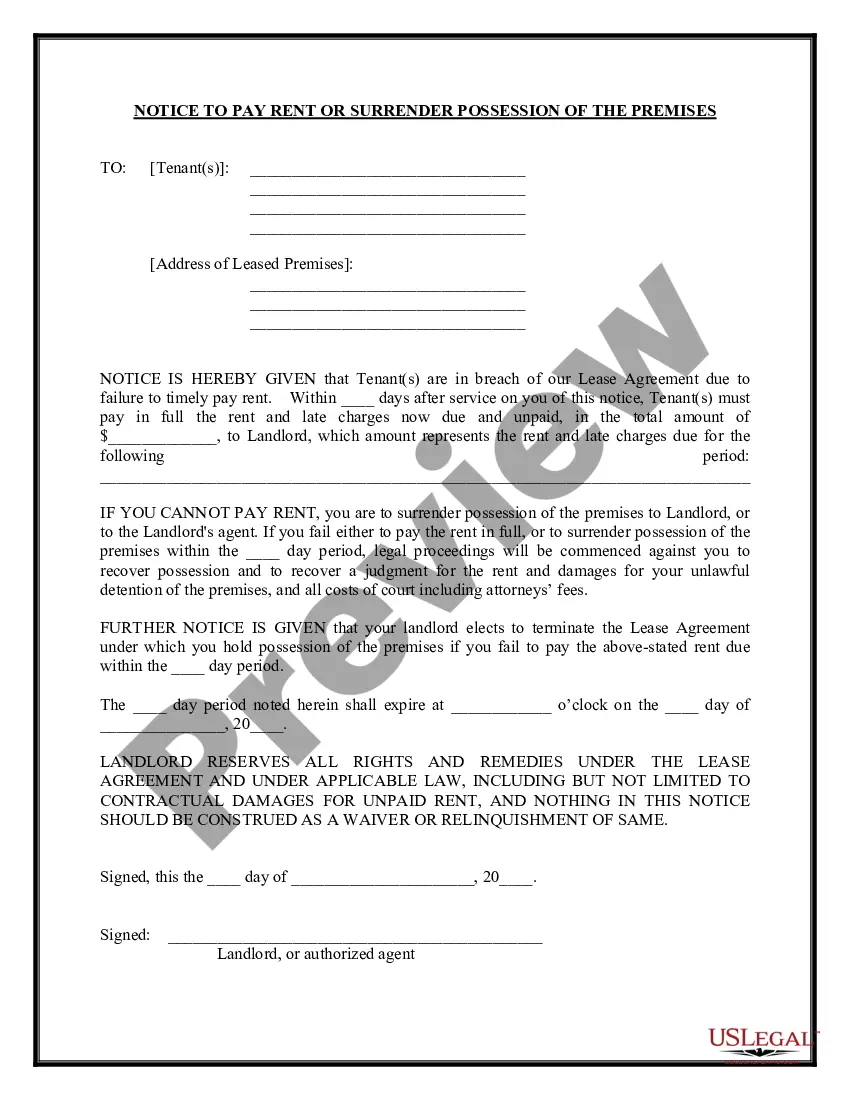

How to fill out Notice To Quit - Give Possession To Landlord - For Nonpayment Of Rent - Past Due Rent?

Whether for professional reasons or personal concerns, everyone has to handle legal matters at some point in their lives.

Completing legal documents necessitates meticulous focus, starting from selecting the appropriate form template.

With an extensive US Legal Forms catalog available, you will never have to waste time searching for the right template on the internet. Utilize the library’s user-friendly navigation to find the correct form for any circumstance.

- Locate the template you require using the search feature or catalog browsing.

- Review the form’s details to make sure it fits your case, state, and area.

- Click on the form’s preview to view it.

- If it is the incorrect document, return to the search option to find the Aviso Desalojo Withdrawn example you need.

- Acquire the template if it meets your needs.

- If you possess a US Legal Forms account, click Log in to access previously saved files in My documents.

- In case you don’t have an account yet, you can obtain the form by clicking Buy now.

- Select the suitable pricing choice.

- Fill out the account registration form.

- Choose your payment method: you can use a credit card or PayPal account.

- Select the file format you prefer and download the Aviso Desalojo Withdrawn.

- After saving it, you can complete the form using editing software or print it and finish it manually.

Form popularity

FAQ

It's possible to avoid a UCC filing by taking out an unsecured business loan rather than a secured one. For example, many online and alternative lenders offer unsecured loans, and you can get an SBA 7(a) loan of up to $25,000 without collateral.

The UCC filing establishes a lien against the collateral the borrower uses to secure the loan ? giving the lender the right to claim that collateral as repayment in the case of default. However, in many cases, the terms UCC lien and UCC filing are used interchangeably.

You must pay off or refinance the debt to eliminate the UCC filing. But in some cases, you may need to take further steps to remove the UCC lien from your credit report. In some cases, you might need to dispute the lien or enlist the help of an attorney to protect your business.

Typical collateral For example, if you take out a loan to buy new machinery, the lender might file a UCC-1 lien and claim that new machinery as collateral on the loan. You would, of course, work with your lender to designate what the collateral will be before you sign any documentation committing to the loan.

To do so you will generally need to make a trip in person down to your secretary of state's office. Once there, you will be able to swear under oath that you've satisfied the debt in full and wish to request for the UCC-1 filing to be removed.

If you have not filed a UCC-1, then you are considered unsecured, and as such, you are placed in the ?back of the line,? behind the secured creditors. Secured creditors are taken care of first in the division of assets.

Fill in the debtor's name and mailing address. It may be an individual, or it may be in the name of a business or organization. If the loan is in the name of the business, include the business mailing address. There is space for additional debtors. Include them exactly as they appeared on the loan agreement.

Luckily, this process is simple, and all you have to do is request your lender file a UCC-3 termination statement with your last loan payment. This will remove the UCC-1 lien and free you up for other loans.