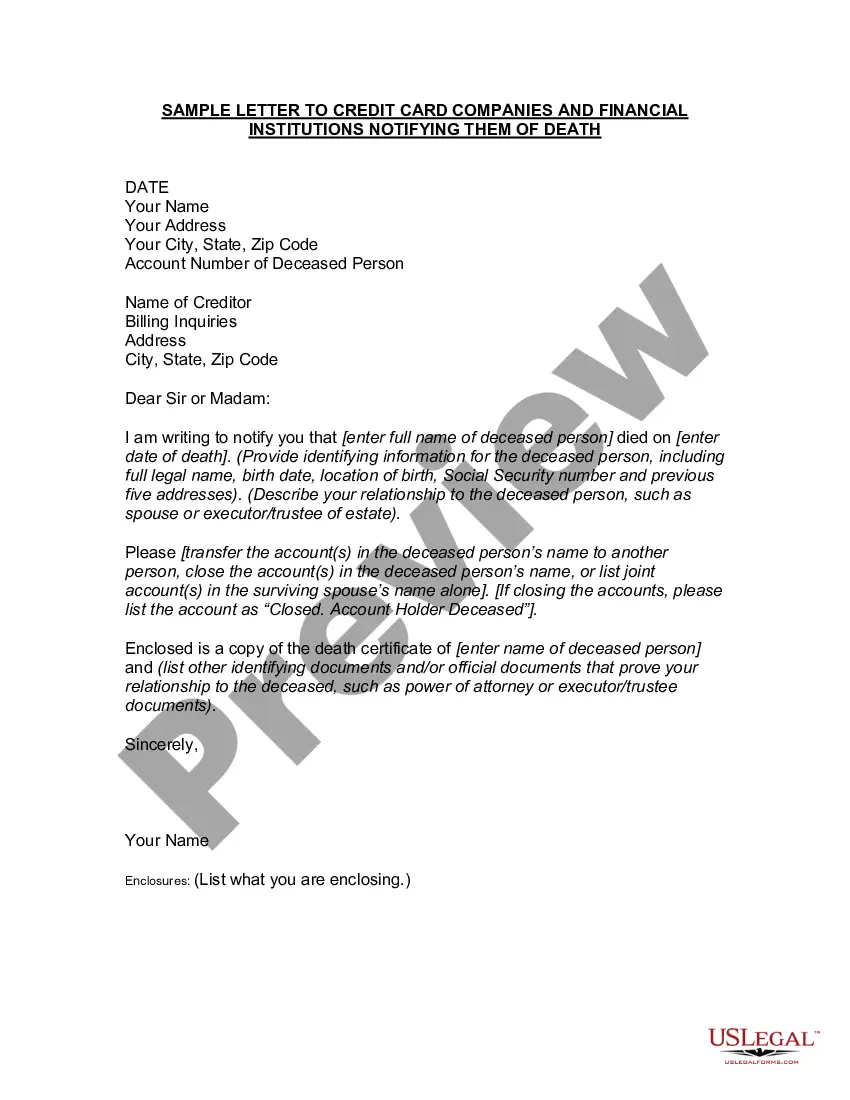

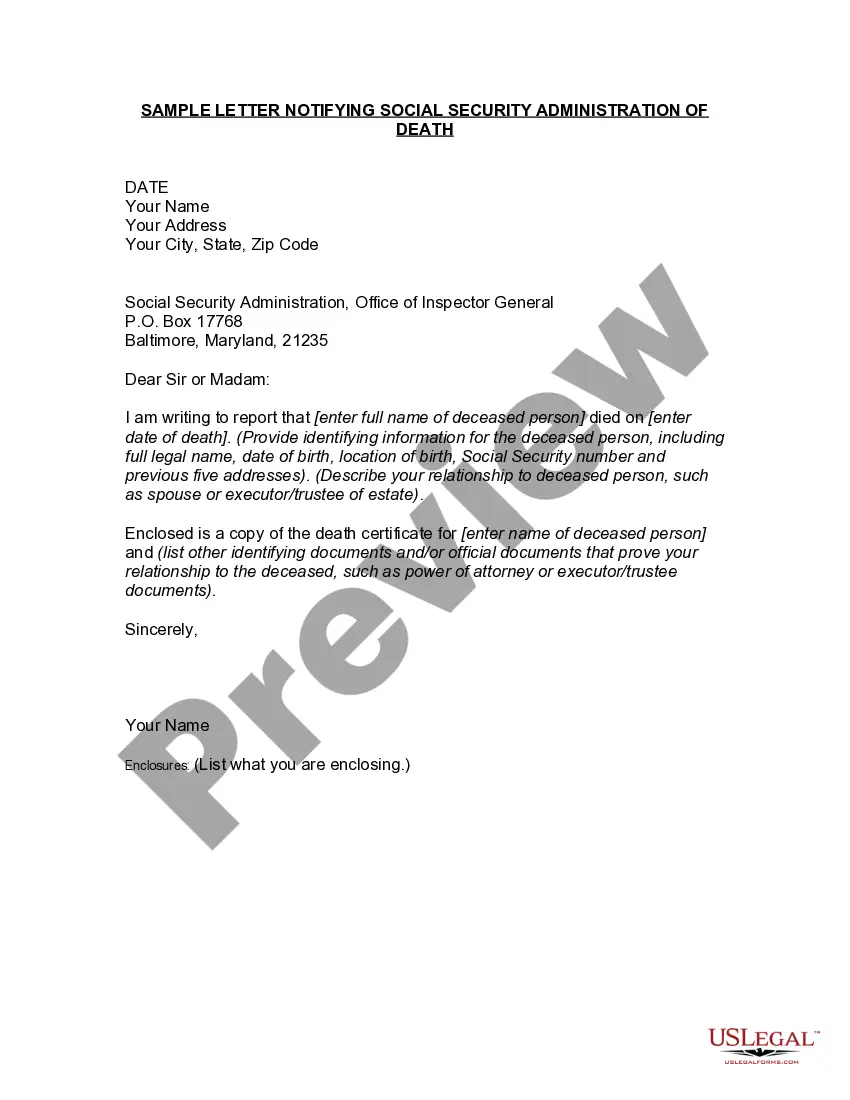

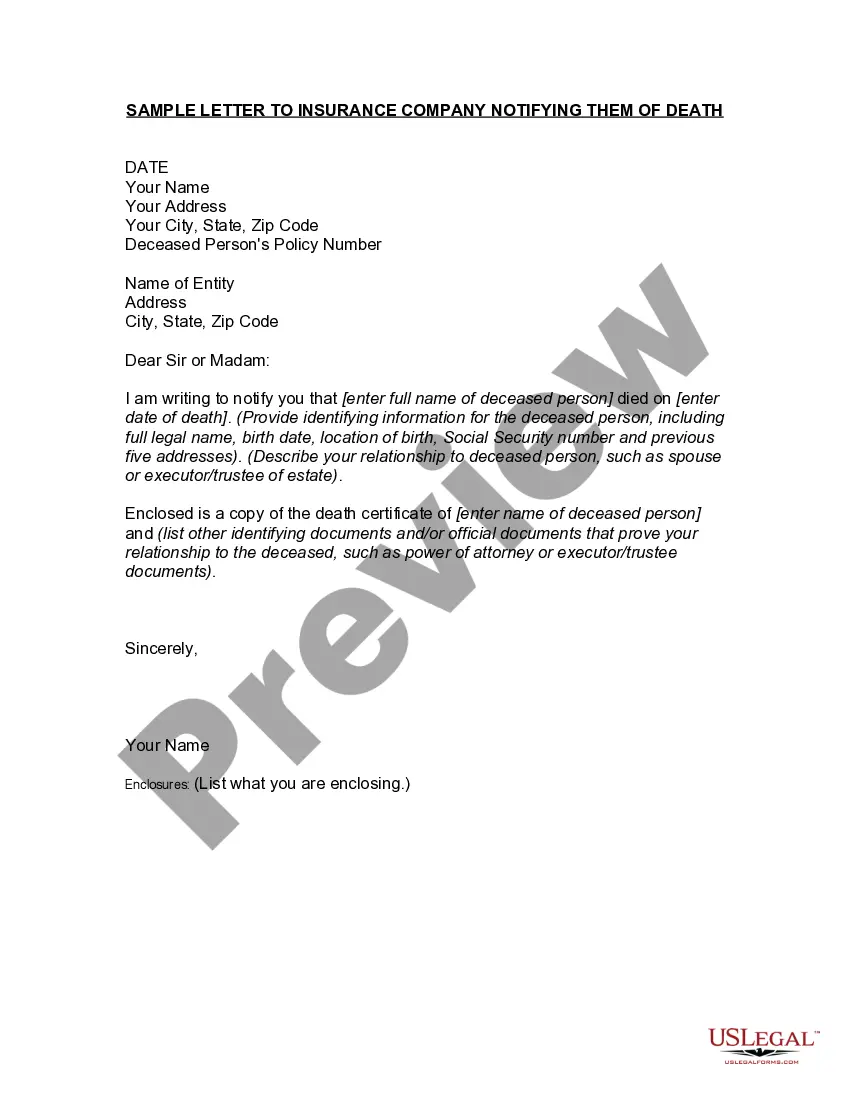

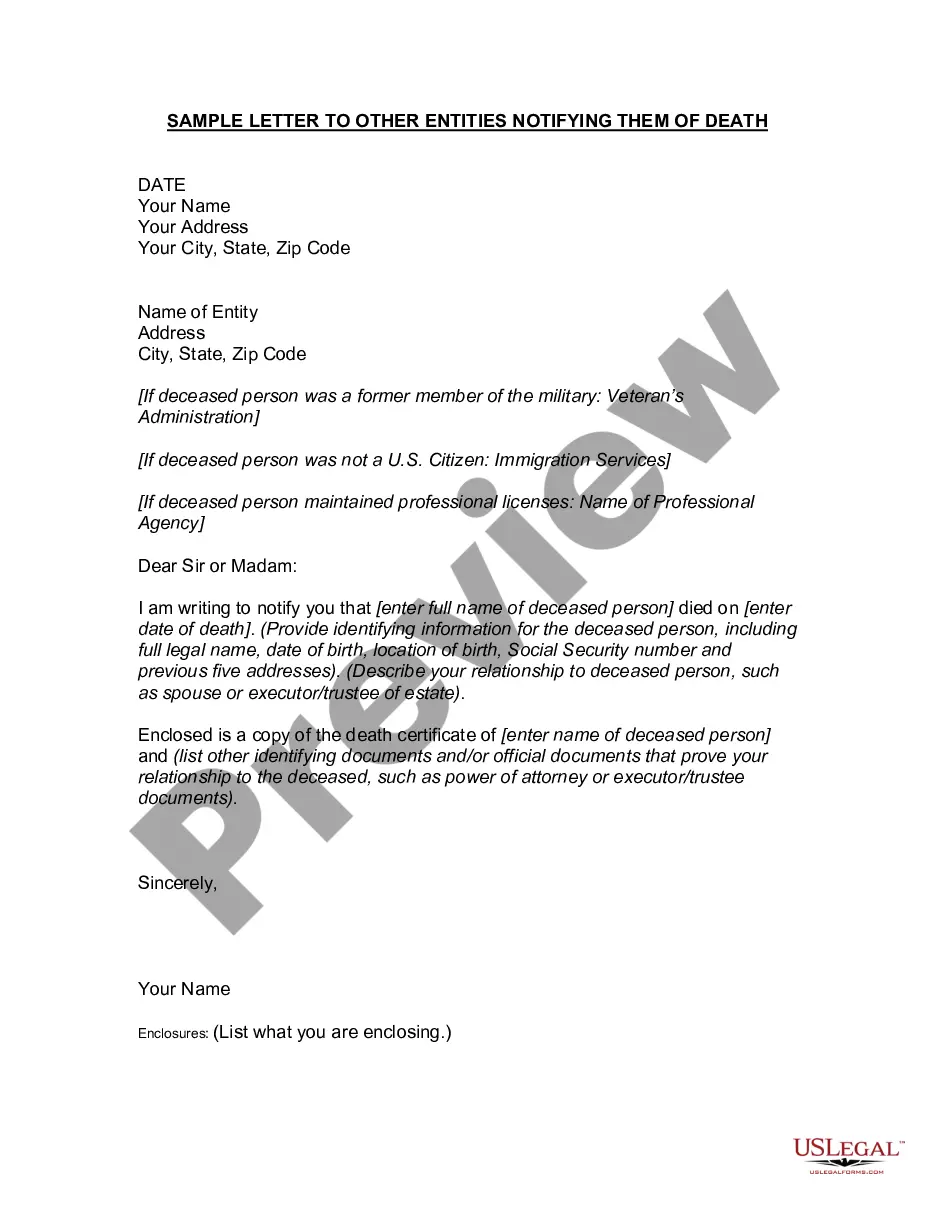

Creditor At Death

Description

How to fill out Letter To Creditor, Collection Agencies, Credit Issuer Or Utility Company Notifying Them Of Death?

Creating legal documents from the beginning can occasionally feel overwhelming.

Some situations may require extensive research and significant finances.

If you seek a simpler and more affordable method of producing a Creditor At Death or other forms without unnecessary obstacles, US Legal Forms is readily accessible.

Our online collection of more than 85,000 current legal forms encompasses almost every dimension of your financial, legal, and personal matters. With just a few selections, you can efficiently obtain state- and county-compliant templates meticulously prepared by our legal experts.

Examine the form preview and descriptions to confirm that you have located the document you need. Verify if the form you select meets the standards of your state and county. Opt for the appropriate subscription plan to acquire the Creditor At Death. Download the form, then complete, sign, and print it. US Legal Forms holds a solid reputation and over 25 years of experience. Join us today and simplify document completion!

- Utilize our site whenever you require dependable and trustworthy services that allow you to effortlessly locate and download the Creditor At Death.

- If you’re already familiar with our services and have an existing account, just Log Into your account, choose the form and download it, or access it again anytime in the My documents section.

- No account yet? That’s not an issue. It requires minimal time to sign up and browse the library.

- However, prior to diving directly into downloading Creditor At Death, consider these suggestions.

Form popularity

FAQ

When a person passes away, the responsibility for their debt typically falls on their estate. This means that creditors at death can claim against the deceased's assets to settle outstanding debts. If the estate lacks sufficient funds, the debts may remain unpaid, and family members generally are not liable unless they are co-signers or joint account holders. To navigate these complexities, US Legal Forms offers resources and documents to help you manage estate matters effectively.

The three-year rule generally refers to the time frame in which creditors must submit their claims against a deceased person's estate. This rule varies by state, so it's important to consult local laws. Failure to file a claim within this period may bar creditors from recovering their debts. As a creditor at death, understanding this timeline is crucial.

Filling out a creditor's claim begins with obtaining the appropriate form, often available through the estate's executor or the probate court. Provide clear information about the debt owed, including dates and amounts. Ensure you include any supporting documents that verify the claim. This process is essential to protect your rights as a creditor at death.

Upon your death, unsecured debts such as credit card debt, personal loans and medical debt are typically discharged or covered by the estate. They don't pass to surviving family members. Federal student loans and most Parent PLUS loans are also discharged upon the borrower's death.

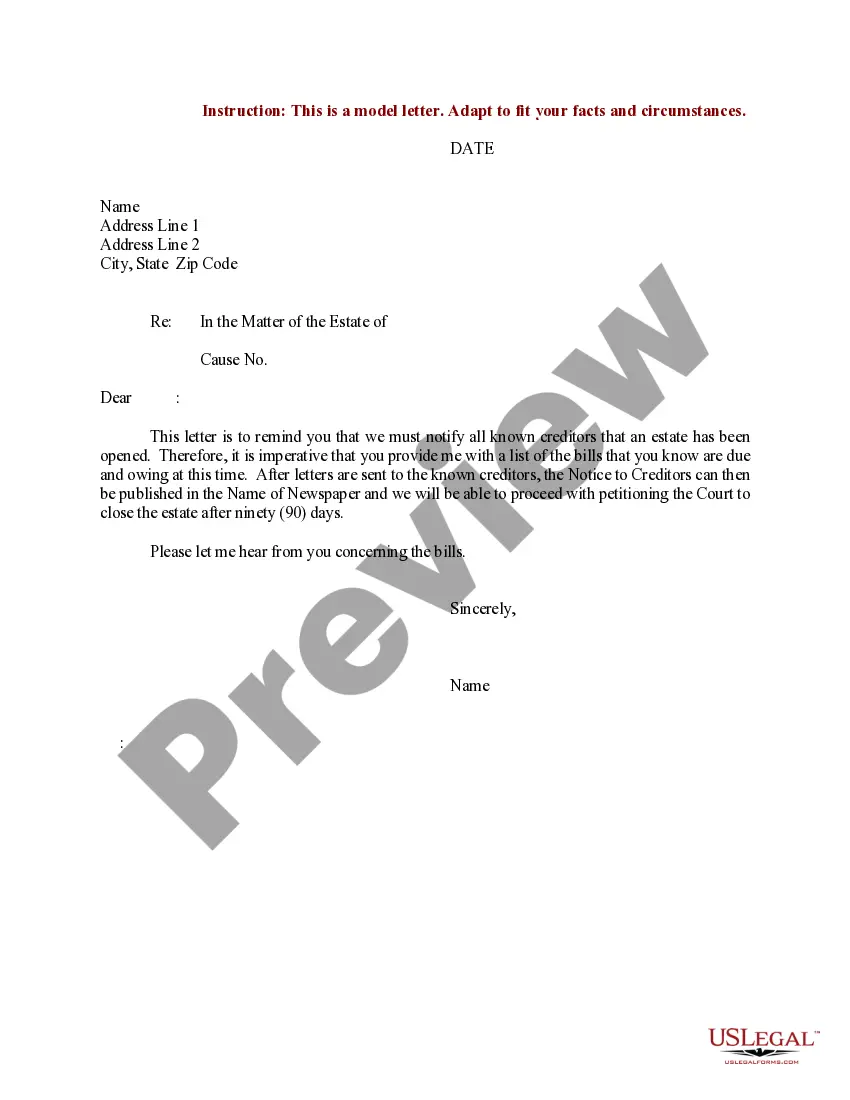

General Information: A creditor of an estate is a person or entity (business or organization) to whom the decedent owed money. ?Decedent? is the term used to refer to the person who died.

There are three major points that a notice to creditors needs to contain: the name of the person who has passed away, the amount of time creditors have to come forward, and contact information for the executor or the executor's lawyer.

Life insurance payments go to your beneficiaries and don't have to be used to pay your debts. Living trusts allow you to pass on property to your heirs and avoid probate. Assets held in a living trust are protected from creditors.

Unfortunately, ?(Detail Deceased's name) ?passed away on ?(Detail Date)?. I enclose a copy of their death certificate. They didn't leave behind any assets and there is no money to pay what they owe. Please consider writing off this debt because there is no prospect of you ever recovering any money towards it.