Assignment Of Promissory Note Sample With No Experience

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note Assignment And Notice Of Assignment?

Regardless of whether for corporate objectives or personal issues, everyone must handle legal matters at some point in their life.

Completing legal documents necessitates meticulous care, beginning with choosing the appropriate template.

Once it is saved, you can fill out the form using editing software or print it to complete it manually. With an extensive US Legal Forms catalog available, you will never need to waste time searching for the correct sample online. Use the library’s user-friendly navigation to find the appropriate form for any situation.

- For example, selecting an incorrect version of the Assignment Of Promissory Note Sample With No Experience will result in its rejection upon submission.

- Thus, it is crucial to find a trustworthy source of legal documents such as US Legal Forms.

- If you need to acquire an Assignment Of Promissory Note Sample With No Experience template, follow these simple steps.

- Utilize the search bar or catalog to find the sample required.

- Review the form’s details to confirm it aligns with your circumstances, state, and locality.

- Click on the form’s preview to examine it.

- If it is the incorrect document, return to the search tool to find the necessary Assignment Of Promissory Note Sample With No Experience.

- Download the file if it meets your requirements.

- If you already possess a US Legal Forms account, simply click Log in to retrieve previously stored documents in My documents.

- If you do not yet have an account, you can obtain the form by clicking Buy now.

- Select the appropriate pricing option.

- Fill out the account registration form.

- Choose your payment method: you can opt for a credit card or PayPal account.

- Select the document format you prefer and download the Assignment Of Promissory Note Sample With No Experience.

Form popularity

FAQ

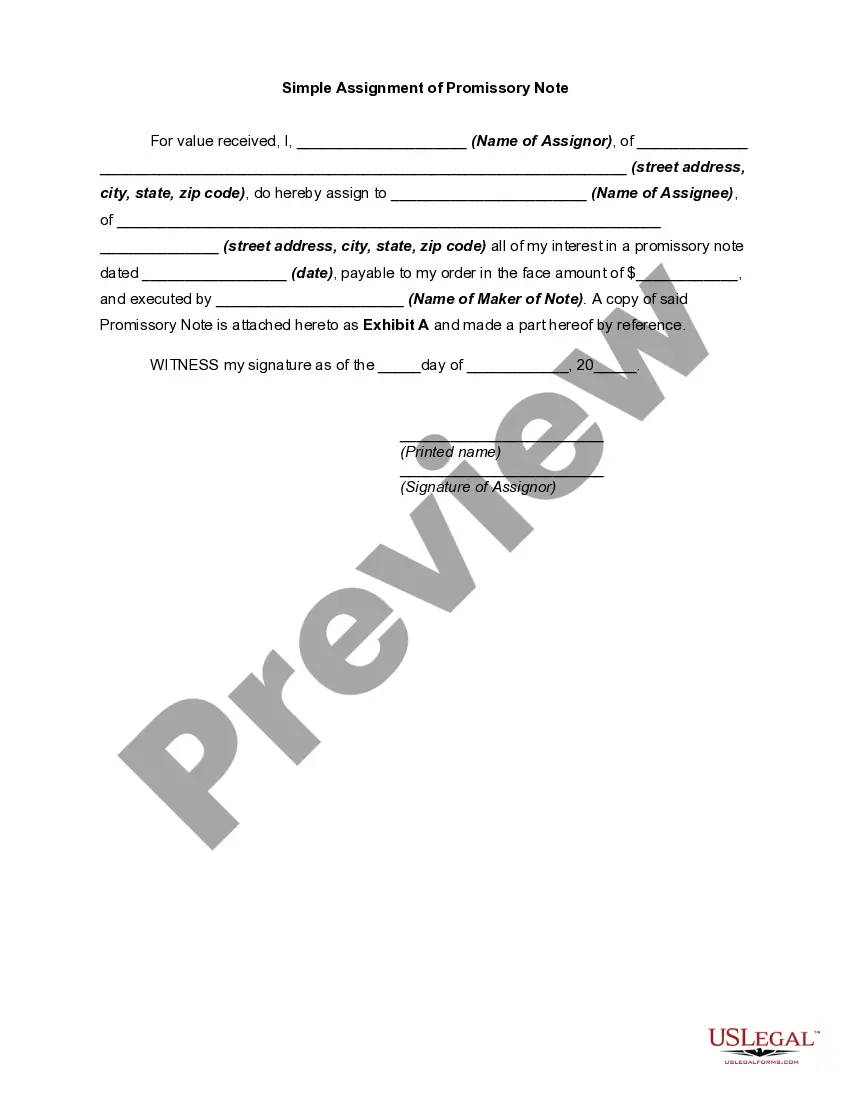

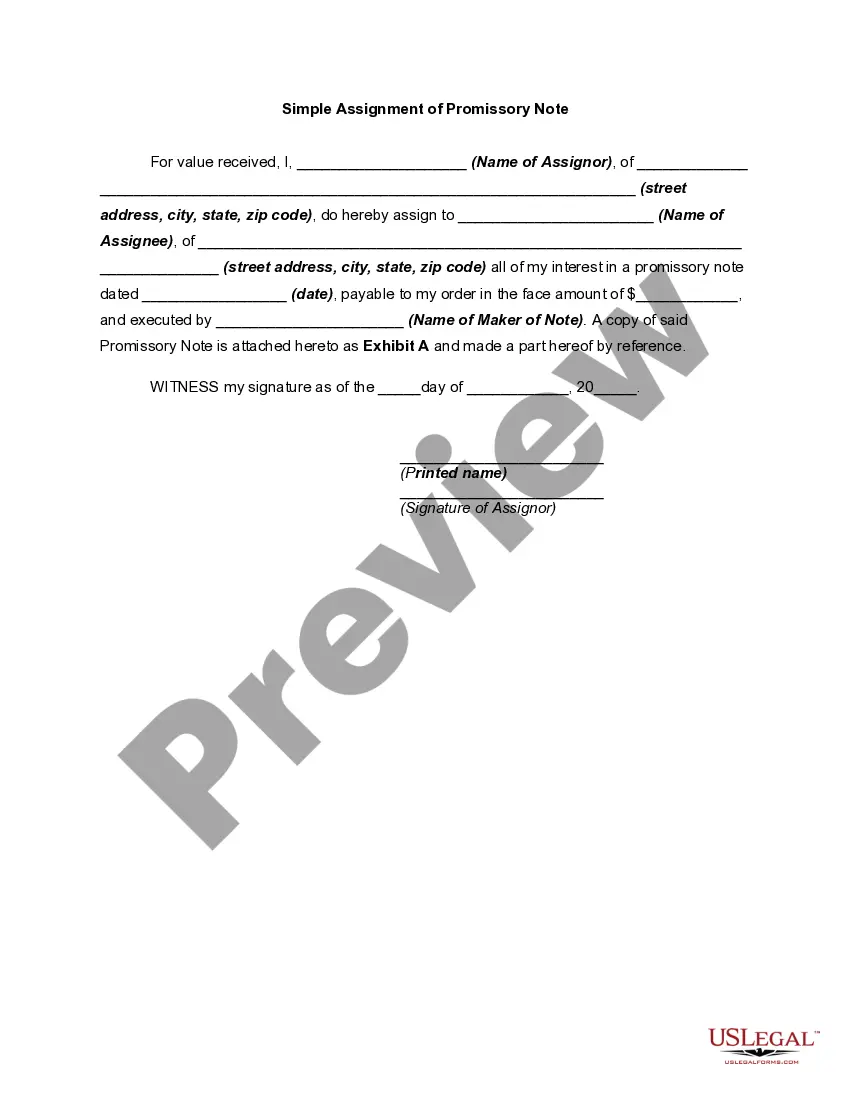

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

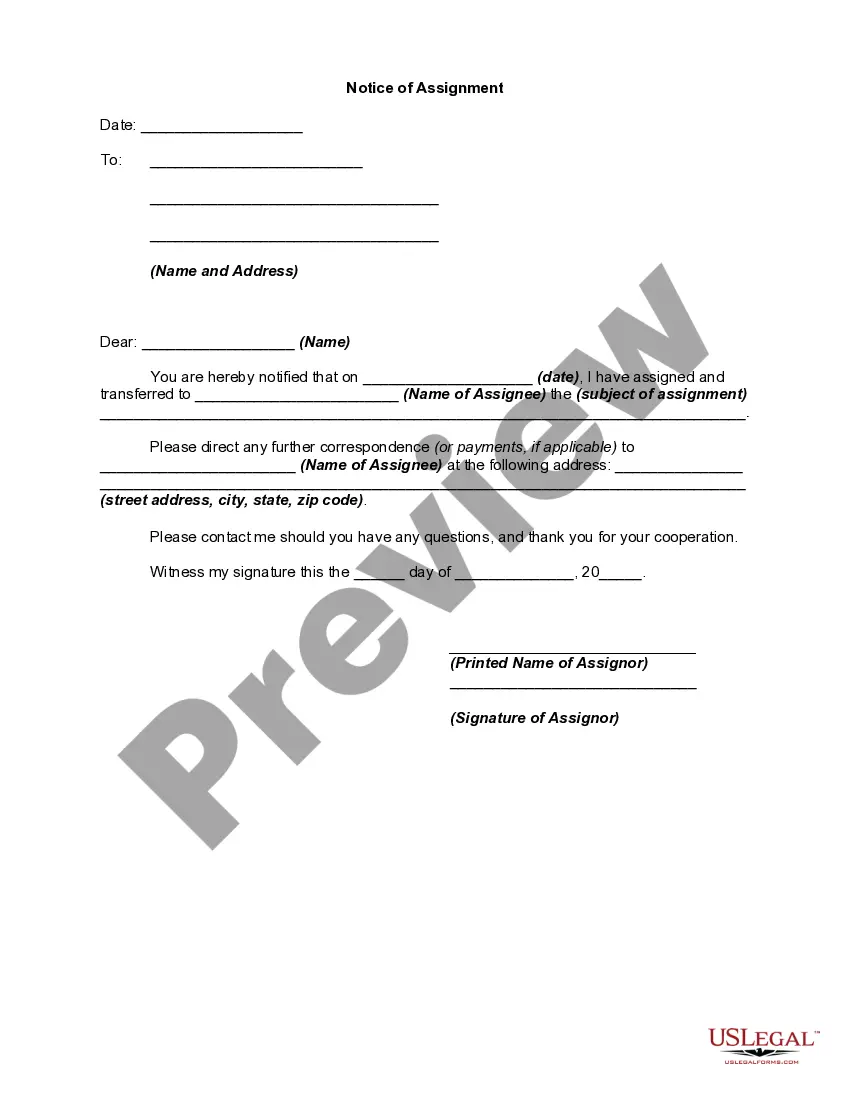

If you are the borrower, issue the promissory note to the institution or individual that needs it to obtain a loan for you. This should be done with an addendum stating the assignment of your rights or the completion of the assignment paperwork required by the lender.

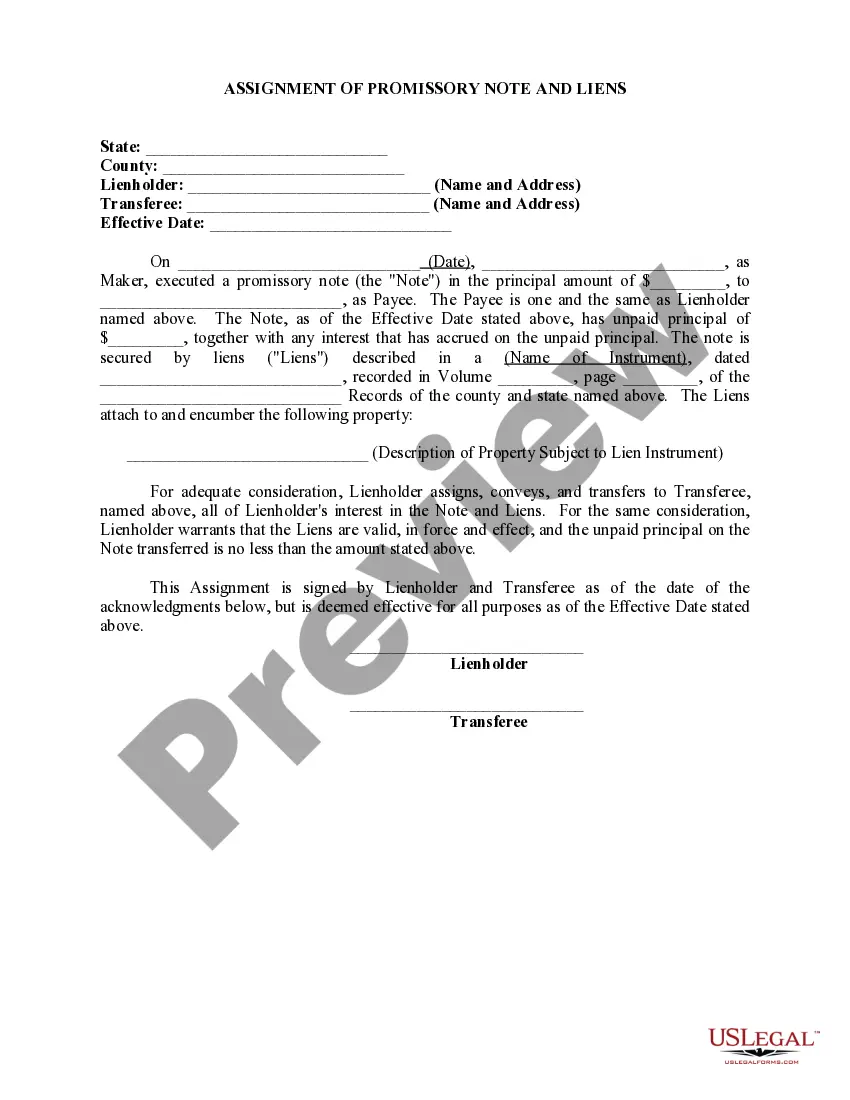

Because promissory notes are negotiable instruments, the basic promissory note is a negotiable promissory note. Therefore, if you, as payer, give a promissory note to someone who has given you a loan, that person can then turn around and transfer or assign the note to a third party.

A banknote is frequently referred to as a promissory note, as it is made by a bank and payable to bearer on demand. Mortgage notes are another prominent example. If the promissory note is unconditional and readily saleable, it is called a negotiable instrument.

Negotiable promissory notes are freely transferable by endorsement (if made to order) or by delivery (if made to bearer), and are highly liquid. A transferee of a negotiable instrument generally takes it free and clear of any claims or defenses that the Borrower (the Maker) has against the original Lender (Holder).