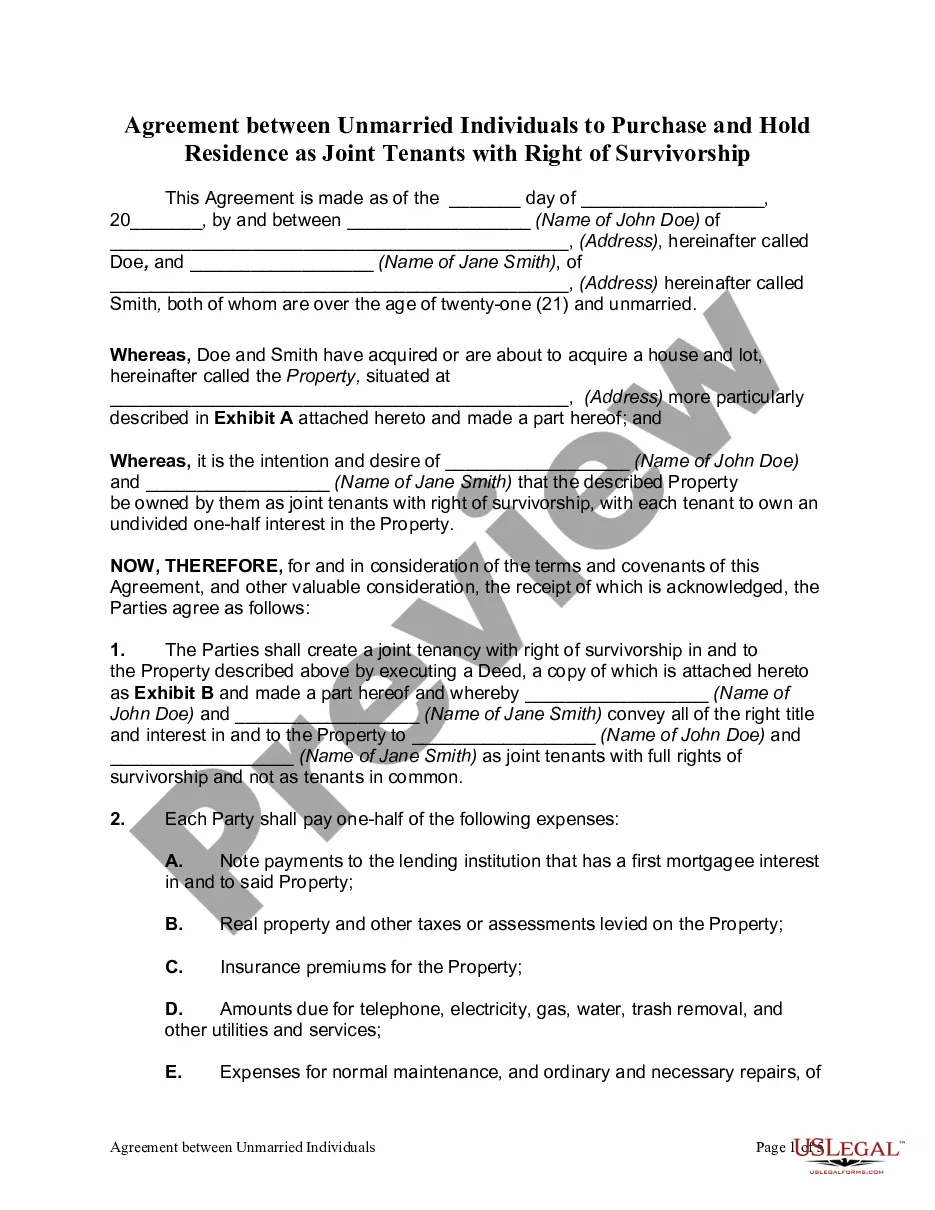

Joint Tenancy With Right Of Survivorship In California

Description

How to fill out Agreement Between Unmarried Individuals To Purchase And Hold Residence As Joint Tenants With Right Of Survivorship?

The Joint Tenancy With Right Of Survivorship In California displayed on this page is a versatile formal template prepared by experienced attorneys in accordance with federal and state regulations.

For over 25 years, US Legal Forms has supplied individuals, businesses, and legal practitioners with more than 85,000 authenticated, state-specific documents for any commercial and personal circumstances. It’s the quickest, easiest, and most reliable method to acquire the paperwork you require, as the service ensures bank-level data protection and anti-malware safeguards.

Subscribe to US Legal Forms to access verified legal templates for all of life's situations whenever needed.

- Search for the document you require and review it.

- Browse the sample you searched and preview it or check the form description to confirm it meets your needs. If it does not, utilize the search bar to find the appropriate one. Click Buy Now when you've found the template you need.

- Register and Log In.

- Choose the pricing plan that works for you and create an account. Use PayPal or a credit card for a quick transaction. If you already possess an account, Log In and review your subscription to proceed.

- Acquire the editable template.

- Select the format you prefer for your Joint Tenancy With Right Of Survivorship In California (PDF, DOCX, RTF) and download the sample to your device.

- Complete and sign the documents.

- Print the template to fill it out manually. Alternatively, use an online multifunctional PDF editor to swiftly and accurately fill out and sign your document with a legally-binding electronic signature.

- Redownload your files.

- Utilize the same document again whenever needed. Access the My documents tab in your profile to redownload any forms you have purchased previously.

Form popularity

FAQ

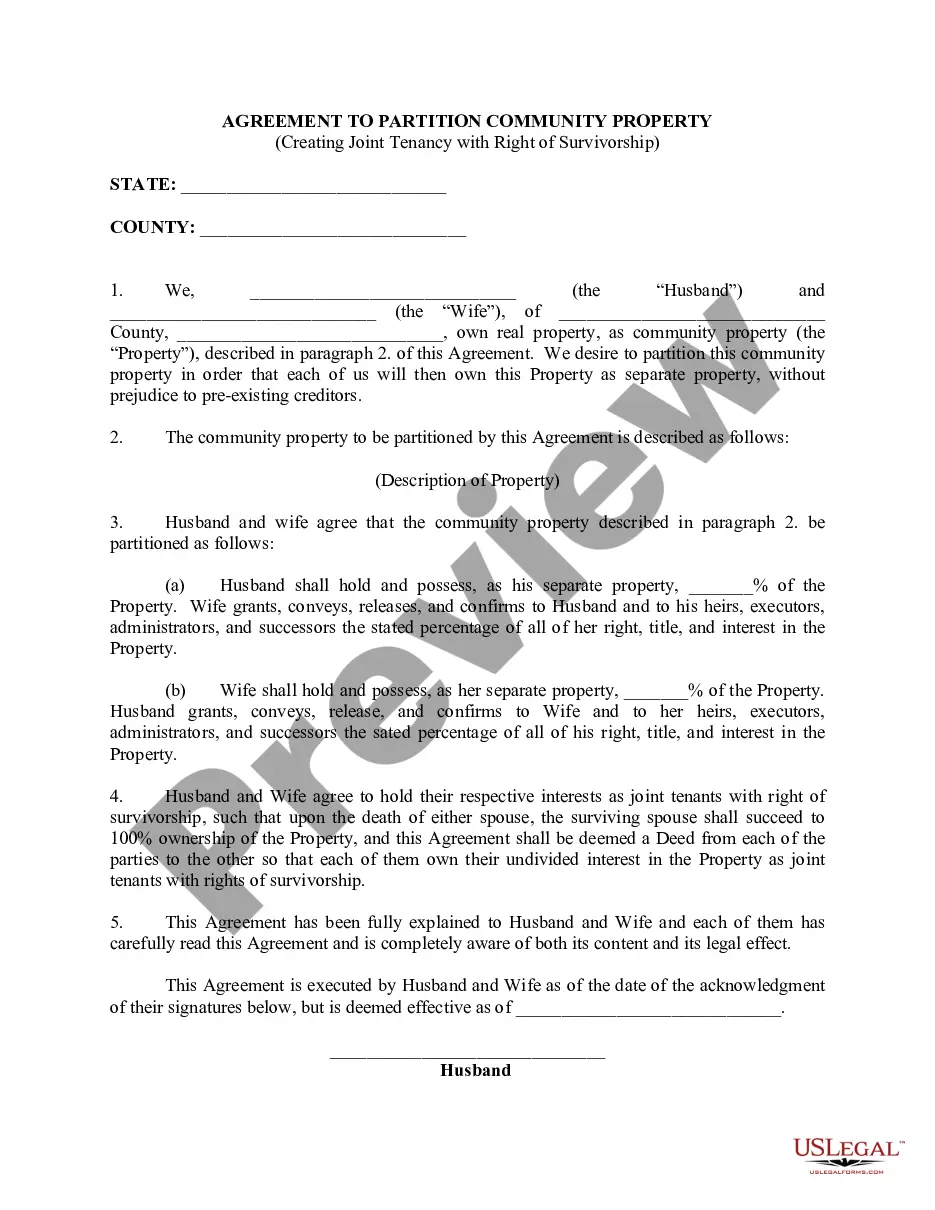

The most significant feature of joint tenancy with right of survivorship in California is that it allows co-owners to automatically inherit each other's share without passing through probate upon death. This means that when one owner passes away, their interest in the property directly transfers to the surviving owner. Therefore, this arrangement not only simplifies the transfer of property but also provides financial security to the surviving tenant.

With joint tenancy? the right of survivorship is implied, so if one joint tenant dies, the other joint tenant or tenants automatically become the owners of the deceased tenant's interest in the property without the property having to pass through probate.

Joint tenancy is a way for two or more people to own property in equal shares so that when one of the joint tenants dies, the property can pass to the surviving joint tenant(s) without having to go through probate court.

Joint Tenancy Has Some Disadvantages They include: Control Issues. Since every owner has a co-equal share of the asset, any decision must be mutual. You might not be able to sell or mortgage a home if your co-owner does not agree.

For spouses: Assets in JTWROS accounts may get a step-up on cost basis when either spouse passes away. This can help reduce capital gains taxes when selling a property, but you can only step-up half of the full value of the asset. This 50% step-up represents the portion owned by the joint owner who died.