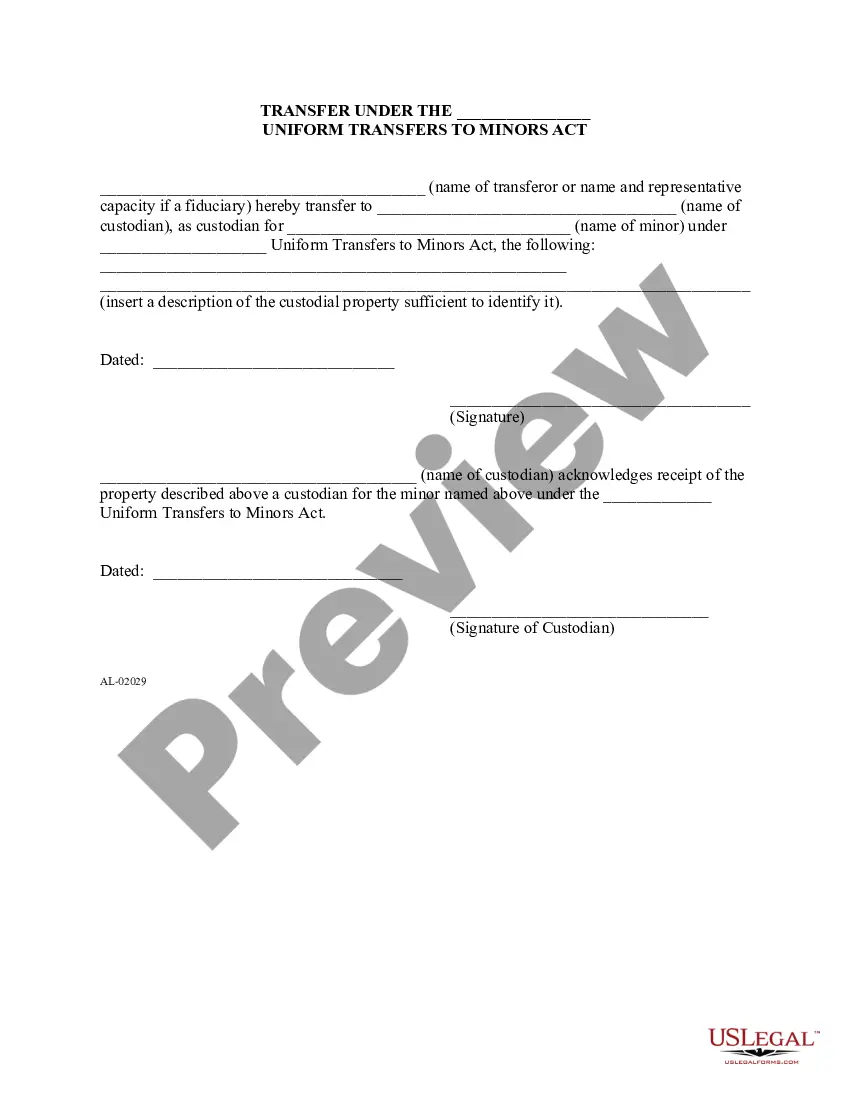

Transfer Uniform Minors Act With Example

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Transfer Of Property Under The Uniform Transfers To Minors Act?

Managing legal papers and tasks can be a lengthy addition to your schedule.

Transfer Uniform Minors Act Along with Example and similar forms often require you to search for them and understand how to fill them out correctly.

Therefore, if you are handling financial, legal, or personal issues, having a thorough and user-friendly online collection of templates readily available will be extremely beneficial.

US Legal Forms is the top online source of legal documents, providing over 85,000 state-specific templates and various tools to assist you in completing your paperwork effortlessly.

Is it your first experience using US Legal Forms? Sign up and create your account in just a few moments, and you will gain access to the form library and Transfer Uniform Minors Act Along with Example. Then, follow the steps below to finalize your form: Ensure you have located the correct form by utilizing the Preview feature and reviewing the form details. Click Buy Now when ready, and choose the monthly subscription plan that suits you best. Select Download then fill out, sign, and print the form. US Legal Forms boasts twenty-five years of experience assisting users manage their legal documents. Find the form you need today and simplify any procedure effortlessly.

- Browse the collection of pertinent documents accessible to you with just one click.

- US Legal Forms provides state- and county-specific templates available for download at any time.

- Protect your document management processes by utilizing a reliable service that allows you to prepare any form within minutes without extra or concealed charges.

- Simply Log In to your account, find Transfer Uniform Minors Act Along with Example and obtain it immediately in the My documents section.

- You can also retrieve previously saved forms.

Form popularity

FAQ

Transferring a UTMA account to a child is simple. You can do so with most financial or investment institutions. You can also consult a tax or business lawyer to help you set up the legal structure, although most financial institutions can do this for you.

No limits exist to how much a donor can contribute to a UTMA. However, contributions over $17,000 per child (if married, $34,000) are subject to federal gift tax.

UTMA accounts offer parents a way to give their children a head start in life. But just because a child holds the account doesn't mean they avoid taxes. UTMA account holders may owe taxes at their personal rate and their parents' rate if the account earns any investment income or capital gains on asset sales.

UGMA/UTMA account assets can be transferred into a new account established by the now adult beneficiary as a sole or joint owner.

Because money placed in an UGMA/UTMA account is owned by the child, earnings are generally taxed at the child's?usually lower?tax rate, rather than the parent's rate. For some families, this savings can be significant. Up to $1,050 in earnings tax-free. The next $1,050 is taxable at the child's tax rate.