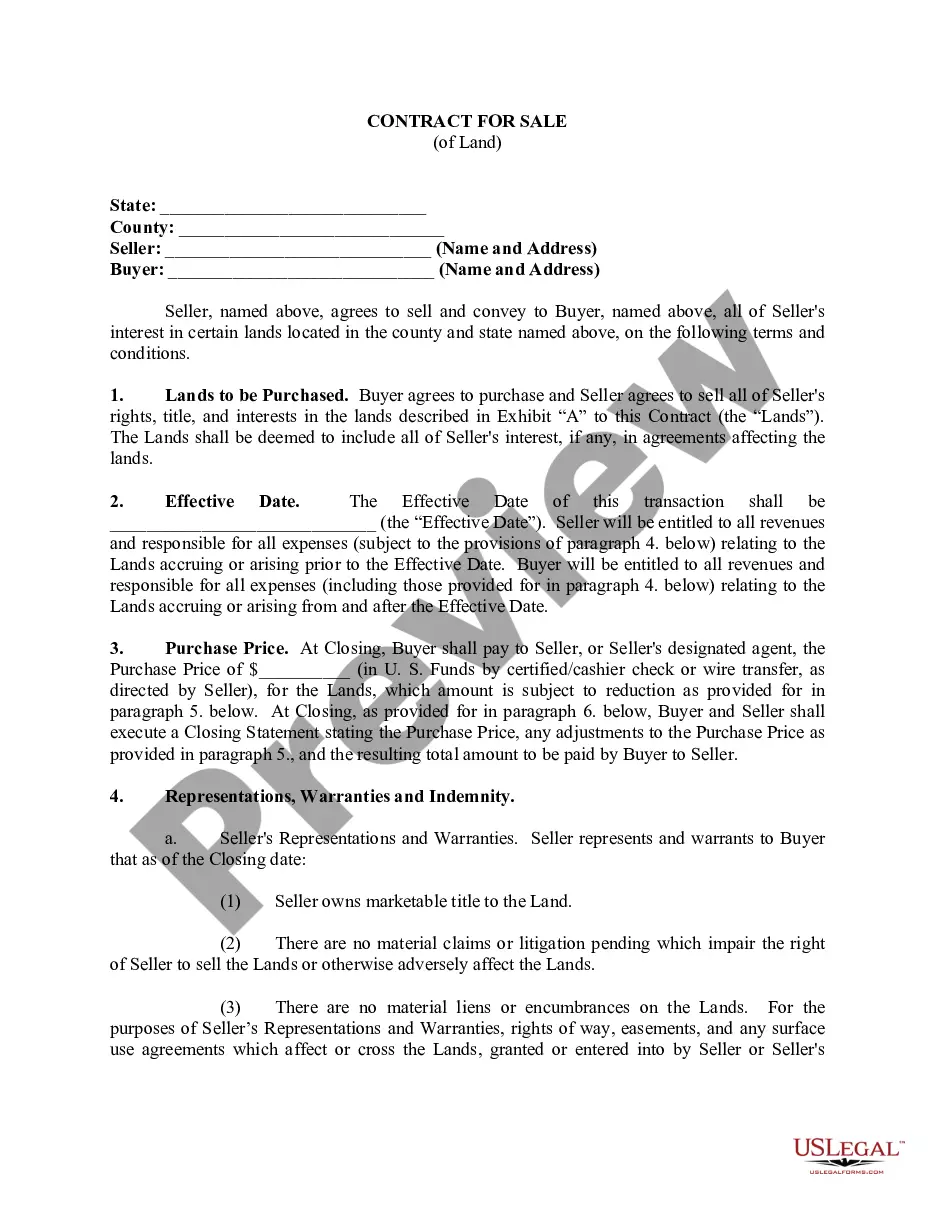

Tax Closing Property For Portability

Description

How to fill out Contract For The Sale And Purchase Of Real Estate - No Broker - Residential Lot Or Land?

Managing legal documentation and processes can be a lengthy addition to your whole day.

Tax Closure Property For Portability and similar forms typically necessitate that you search for them and comprehend how to fill them out efficiently.

For this reason, whether you are dealing with financial, legal, or personal issues, utilizing a comprehensive and convenient online repository of forms readily available will greatly assist.

US Legal Forms is the leading online platform for legal templates, featuring over 85,000 state-specific forms and a variety of resources that will aid you in completing your paperwork with ease.

Is this your first time using US Legal Forms? Sign up and create an account in a few minutes to gain access to the form library and Tax Closure Property For Portability. Then, follow the steps below to complete your form: Ensure you have the correct form using the Preview feature and reviewing the form description. Select Buy Now when ready, and choose the subscription plan that suits you best. Click Download, then fill out, eSign, and print the form. US Legal Forms has 25 years of experience assisting users with their legal paperwork. Find the form you need today and streamline any process effortlessly.

- Explore the collection of relevant documents accessible with just a single click.

- US Legal Forms provides you with state- and county-specific forms available anytime for download.

- Protect your document management processes with a premium service that enables you to prepare any form in minutes without extra or hidden fees.

- Simply Log In to your account, locate Tax Closure Property For Portability, and obtain it directly from the My documents tab.

- You can also retrieve previously saved forms.

Form popularity

FAQ

Portability election. An executor can only elect to transfer the DSUE amount to the surviving spouse if the Form 706 is filed timely, that is, within 9 months of the decedent's date of death or, if you have received an extension of time to file, before the 6-month extension period ends.

The IRS has now extended the timeline for filing for portability to five years after the decedent's date of death. The IRS reasoned in Rev. Proc 2022-32 that the number of requests for private letter rulings requesting extensions placed a significant burden on IRS resources.

Time to file for portability is now extended to five years In July 2022, the IRS issued a revenue procedure (Rev. Proc. 2022-32), which extended the filing of estate tax returns to elect portability to five years from the date of death of the decedent.

In order to elect portability of the decedent's unused exclusion amount (deceased spousal unused exclusion (DSUE) amount) for the benefit of the surviving spouse, the estate's representative must file an estate tax return (Form 706) and the return must be filed timely.