Contract Contractor Building Format In Kings

Description

Form popularity

FAQ

When it comes to business, understanding the 4 elements of a contract business law is essential. A valid contract is built on these cornerstones: Offer, Acceptance, Consideration, and Intention to Create Legal Relations. Here's a quick look: Offer: A clear proposal to make a deal.

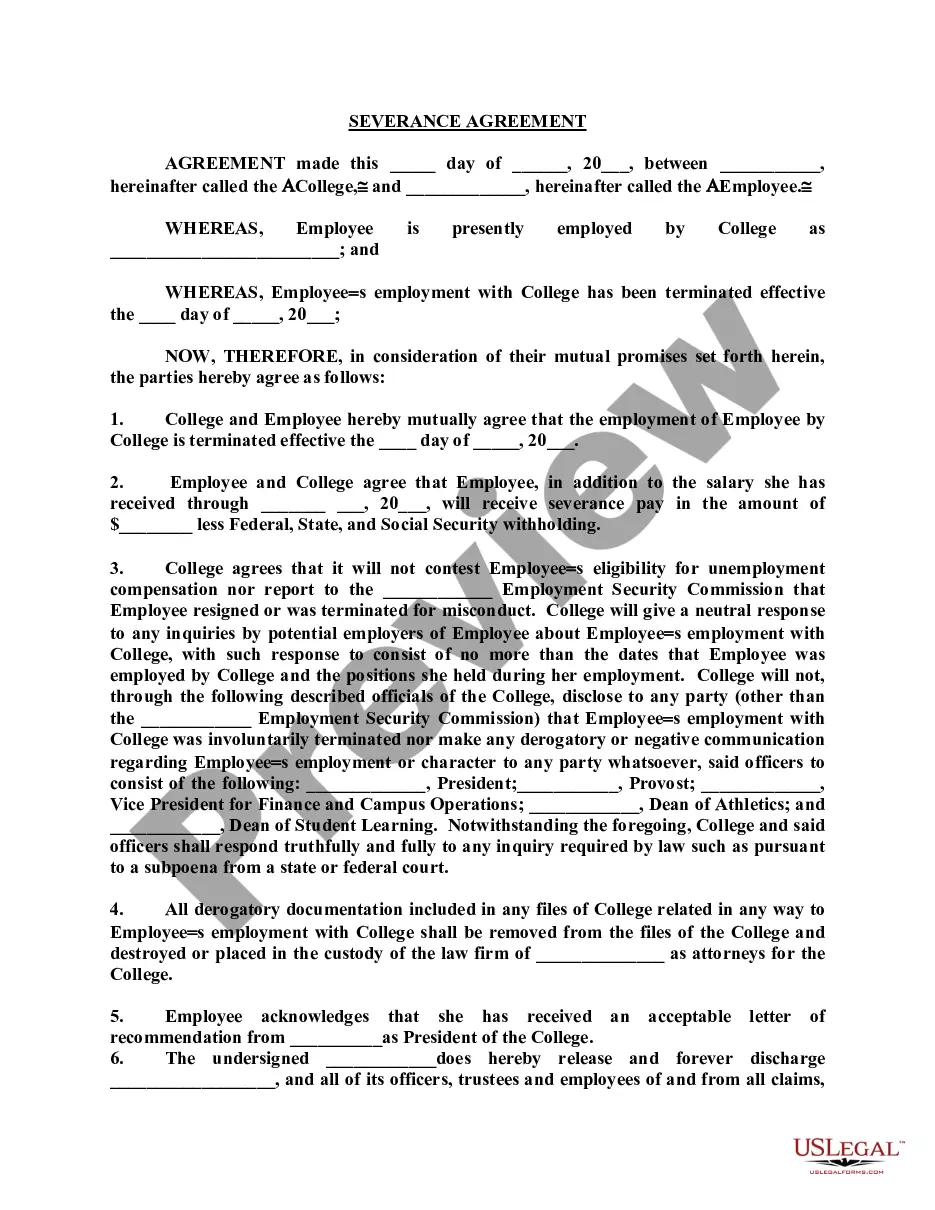

To be legally enforceable, an agreement must contain all of the following criteria: An offer and acceptance; Certainty of terms; Consideration; An intention to create legal relations; Capacity of the parties; and, Legality of purpose.

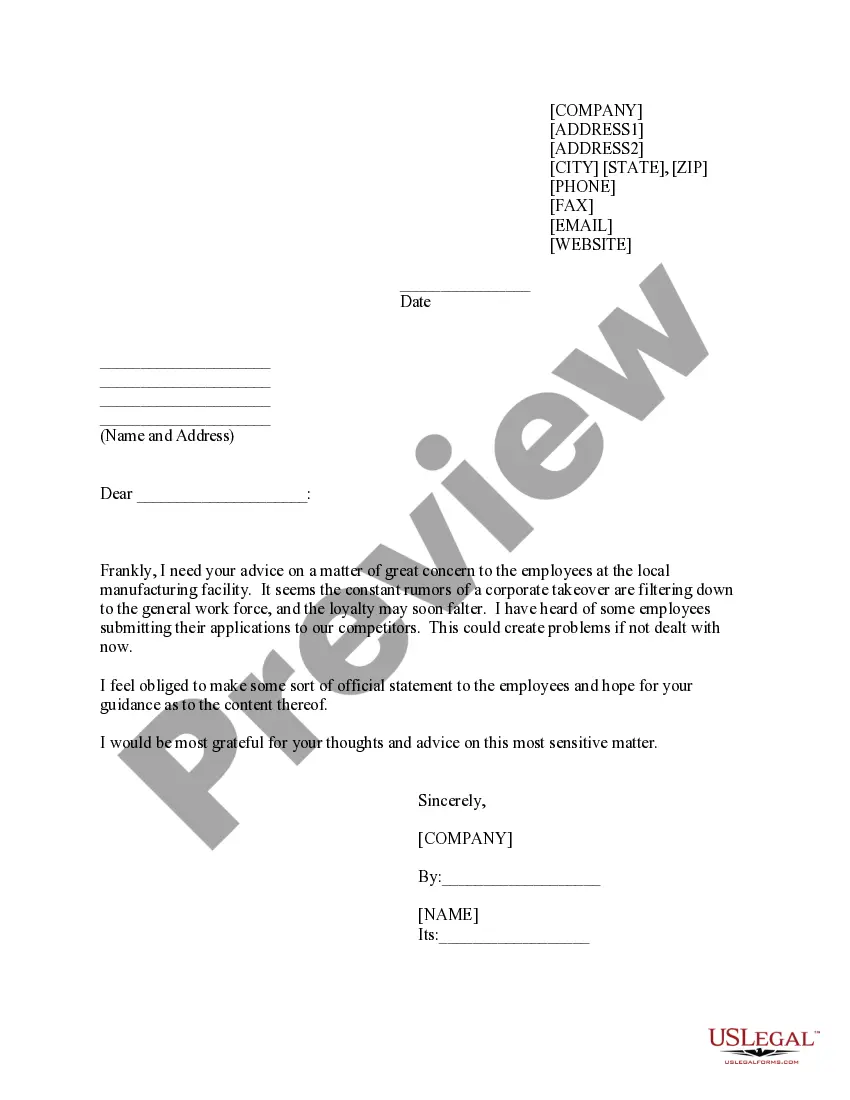

Contracts don't need to be in legal language, but they do need to outline exactly who is responsible for what from obtaining various permissions (such as building control approval) to timings, tidying up, materials, insurance and how payments will be made. A written contract will protect you and reduce risks.

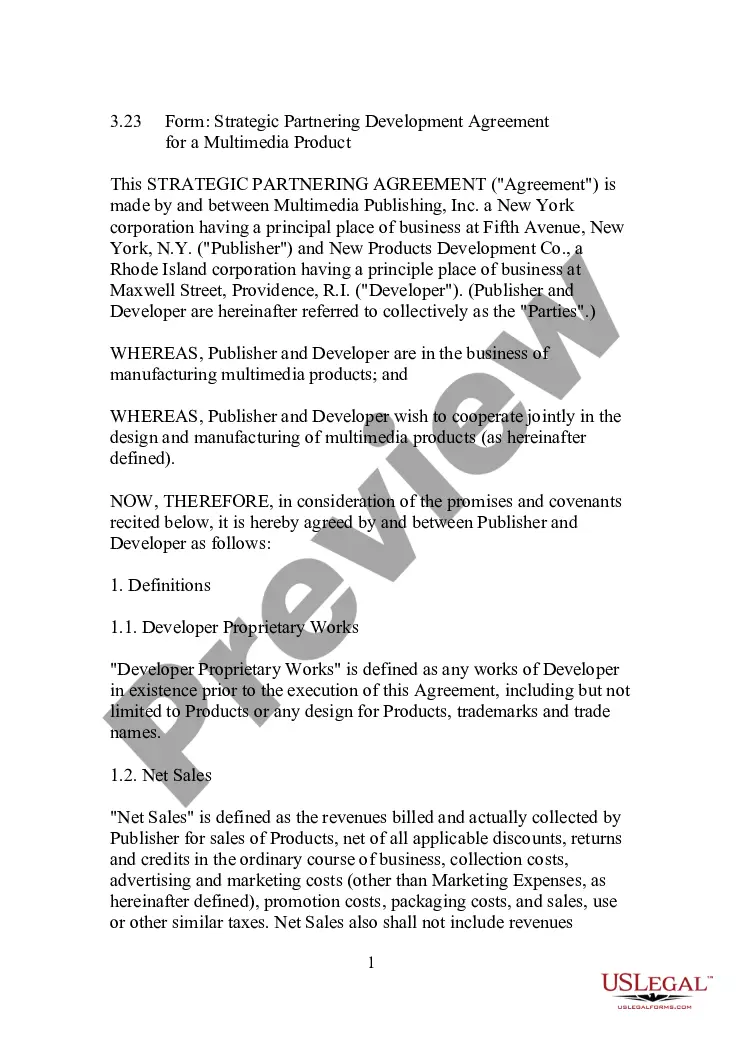

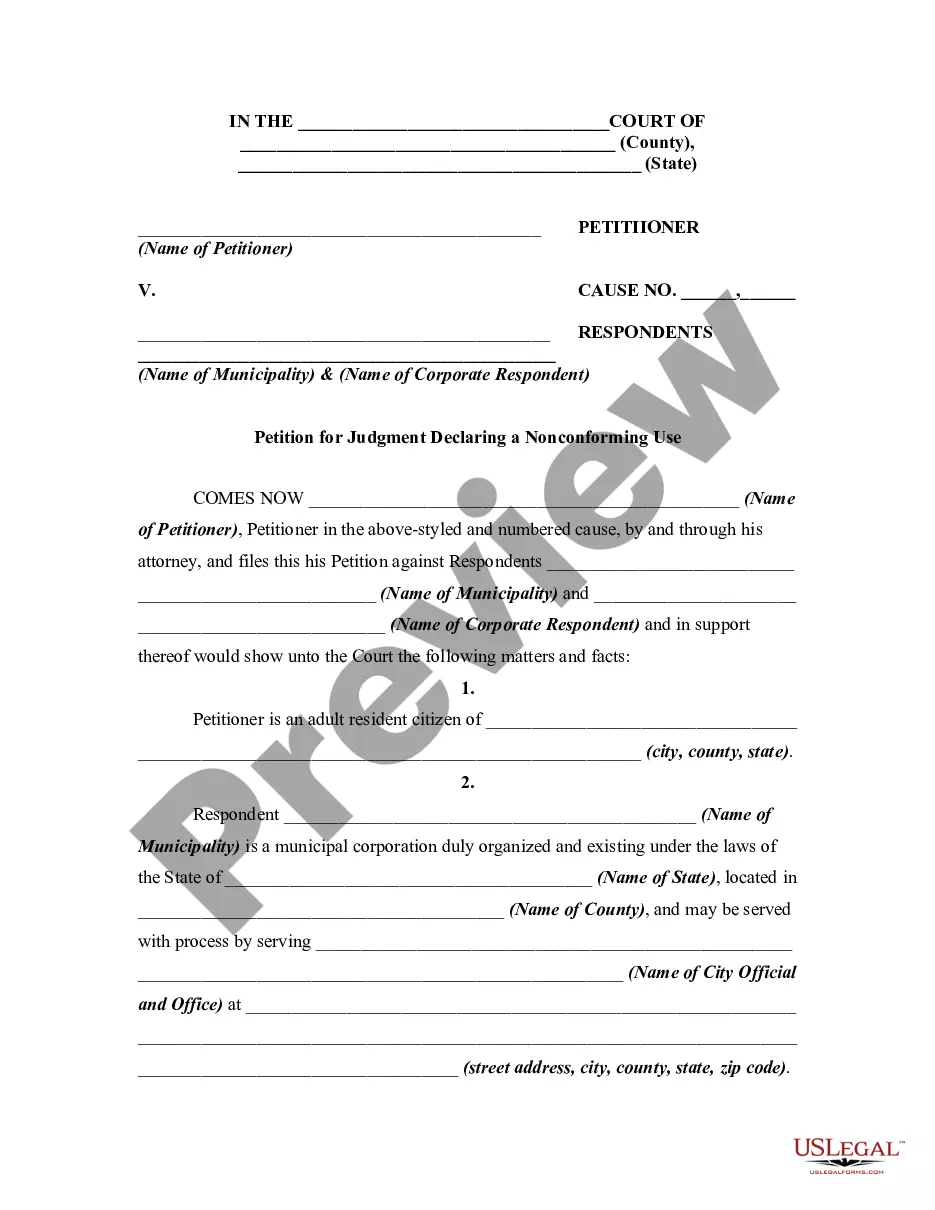

Ing to Boundy (2012), typically, a written contract will include: Date of agreement. Names of parties to the agreement. Preliminary clauses. Defined terms. Main contract clauses. Schedules/appendices and signature provisions (para. 5).

Below are eight important points to consider including in an independent contractor agreement. Define a Scope of Work. Set a Timeline for the Project. Specify Payment Terms. State Desired Results and Agree on Performance Measurement. Detail Insurance Requirements. Include a Statement of Independent Contractor Relationship.

How to draft a contract in 13 simple steps Start with a contract template. Understand the purpose and requirements. Identify all parties involved. Outline key terms and conditions. Define deliverables and milestones. Establish payment terms. Add termination conditions. Incorporate dispute resolution.

What is a standard form contract? While many contracts are entirely purpose made, standard form contracts consist of standardised, pre-written terms and conditions. Because standard form contracts are familiar to people in an industry, they often function effectively without the need for much negotiation.

Standard-form contracts are pre-drafted templates with standard terms and conditions popular in similar transactions. By using a standard form, parties can save time and resources negotiating individual contract terms. It can be especially beneficial in industries with frequent transactions and similar terms.

A standard form contract will typically be one prepared by one party to the contract and not negotiated between the parties—it is offered on a 'take it or leave it' basis.