Consignment Form Template With Prices In Washington

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

There are several types of consignees in logistics: Ultimate consignee. The final recipient of the goods, often the buyer or end-user. Intermediate consignee. An entity that receives the shipment temporarily before forwarding it to the ultimate consignee. Notify party.

This kind of arrangement is called Consignment. Definition. The contract or an agreement of sending several goods by the producers or manufacturers of a place to their agents for the sale is known as a consignment. Types of Consignment. Outward Consignment. Inward Consignment. Consignment Processing. Sale. Features of a Sale.

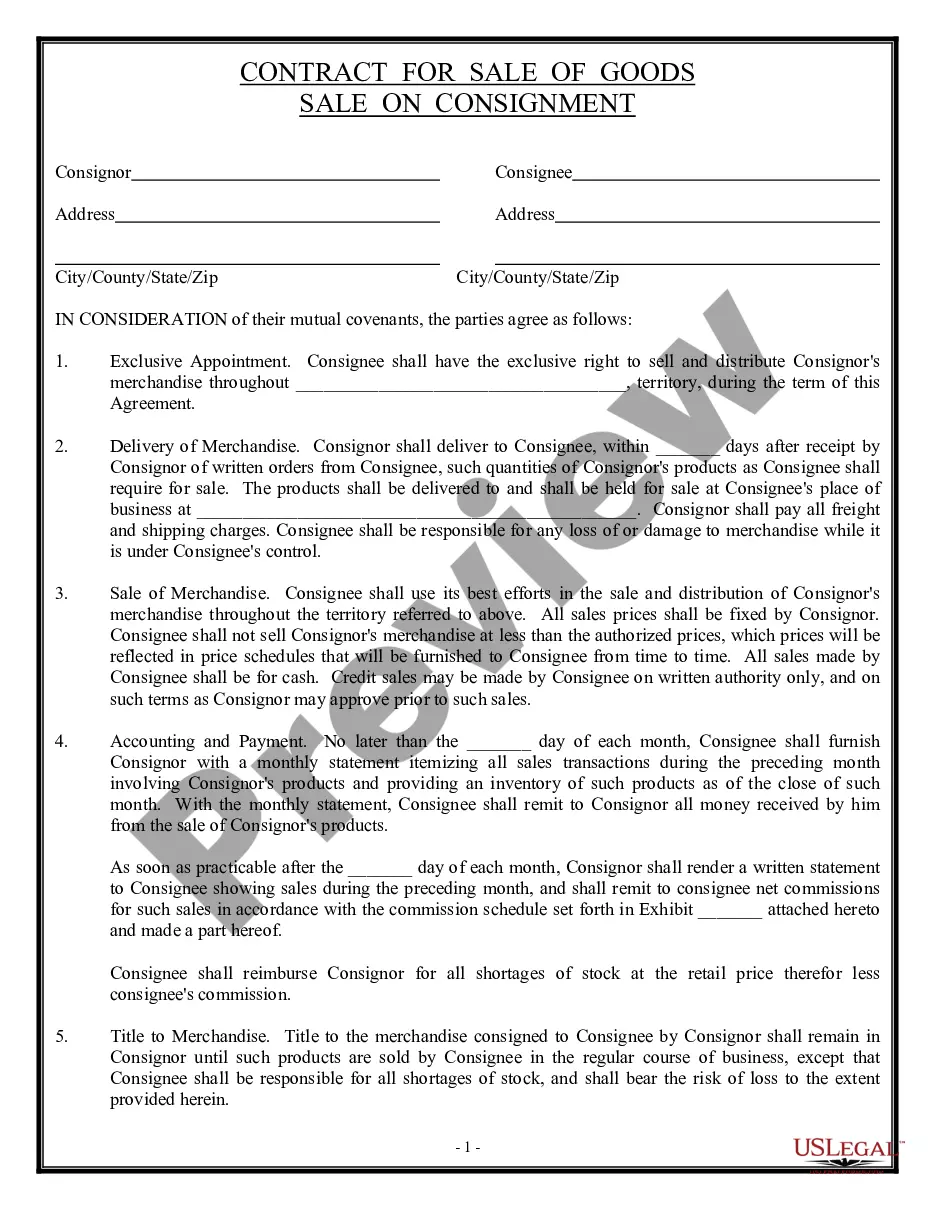

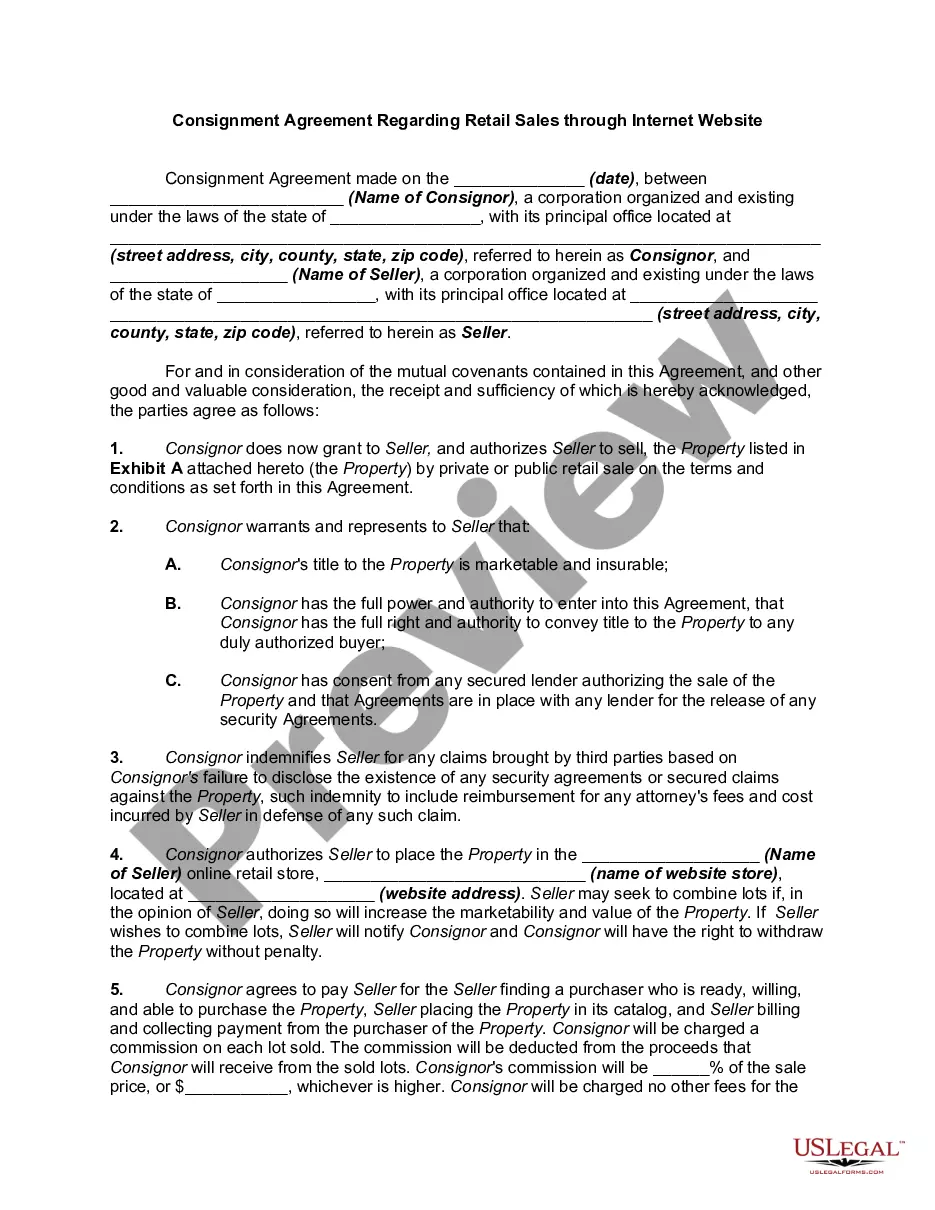

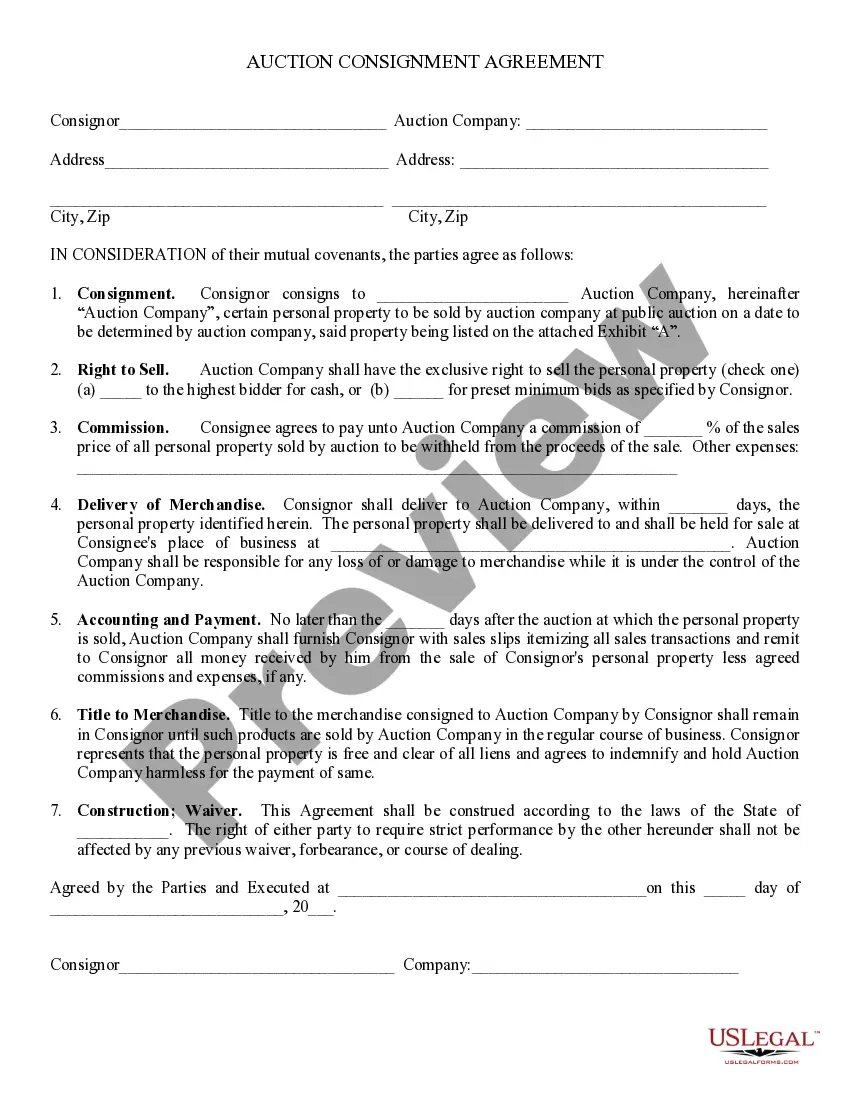

How to Write a Consignment Agreement Parties Involved: Names and contact information of the consignor and the consignee. Consigned Goods: Detailed description of the goods being consigned, including quantities and specifications. Consignment Period: Duration of the consignment arrangement.

Now that you know what consignment is, here's how to calculate consignment inventory. Step 1: Establish a Listing of Your Inventory of Consignment Products. Step 2: Subtract the Seller's or Shipper's Portion of the Consignment Product Sold. Step 3: Update the Inventory After the Sale.

Types of Commission:- 1) Ordinary Commission. The term commission simply denotes ordinary commission. 2) Del-credere Commission. To increase the sale and to encourage the consignee to make credit sales, the consignor provides an additional commission generally known as del-credere commission. 3) Over-riding Commission.

This kind of arrangement is called Consignment. Definition. The contract or an agreement of sending several goods by the producers or manufacturers of a place to their agents for the sale is known as a consignment. Types of Consignment. Outward Consignment. Inward Consignment. Consignment Processing. Sale. Features of a Sale.

Sale occurrence: The consignor can recognize revenue only when the consignee sells the consigned goods to a third party (i.e., the end customer). Reliable transaction information: The consignor can recognize revenue when they have received reliable and timely reports from the consignee about sales transactions.

A consignment agreement involves two parties: the consignor, who owns the goods, and the consignee, who agrees to sell the goods on behalf of the consignor. This type of agreement outlines the responsibilities, terms of sale, and financial arrangements between the parties involved.

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)

For this you will need a report that includes all transactions over the tax year. This report should naturally detail the sale of consigned items, surcharges, and taxes collected or any additional revenue streams. These will all be reported under “total sales” in the tax form.