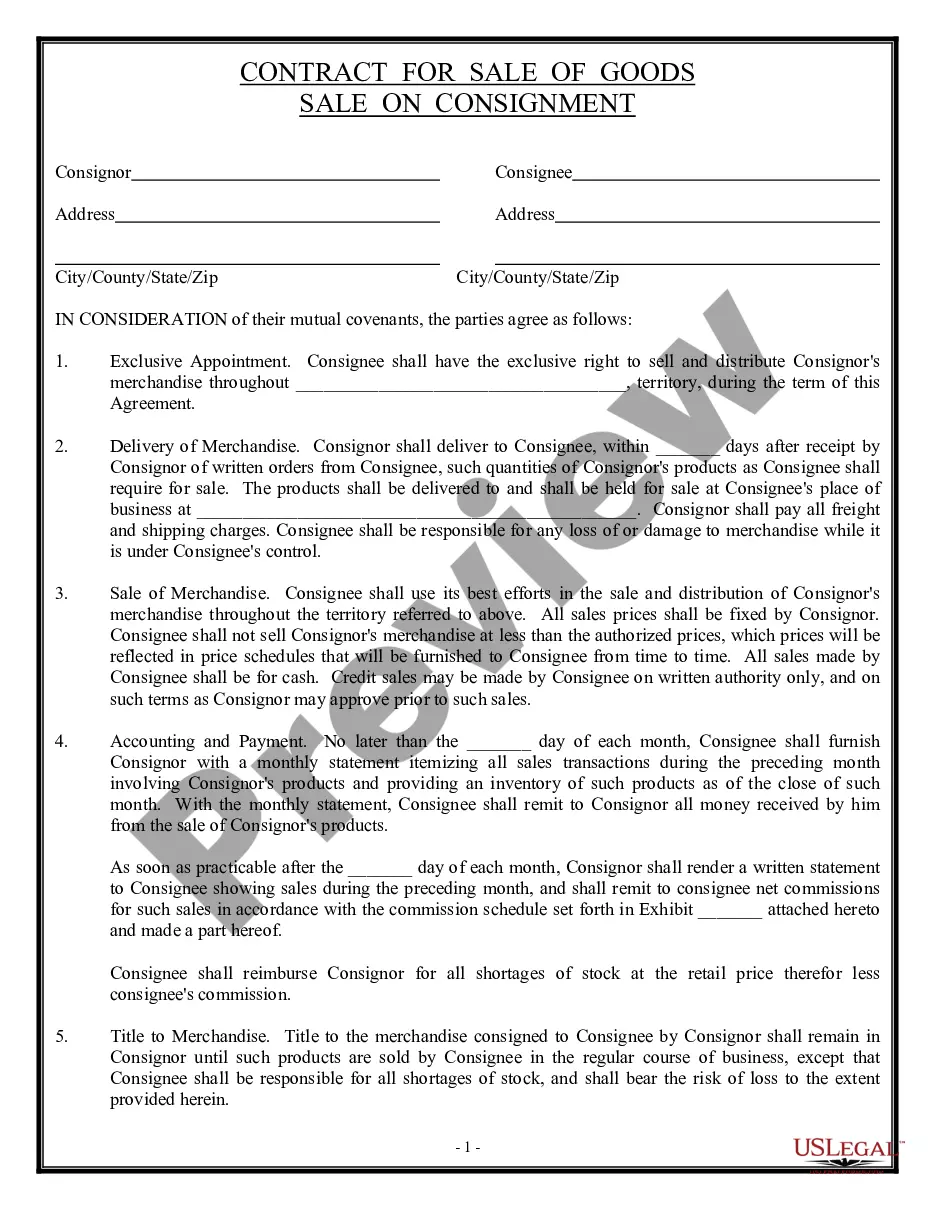

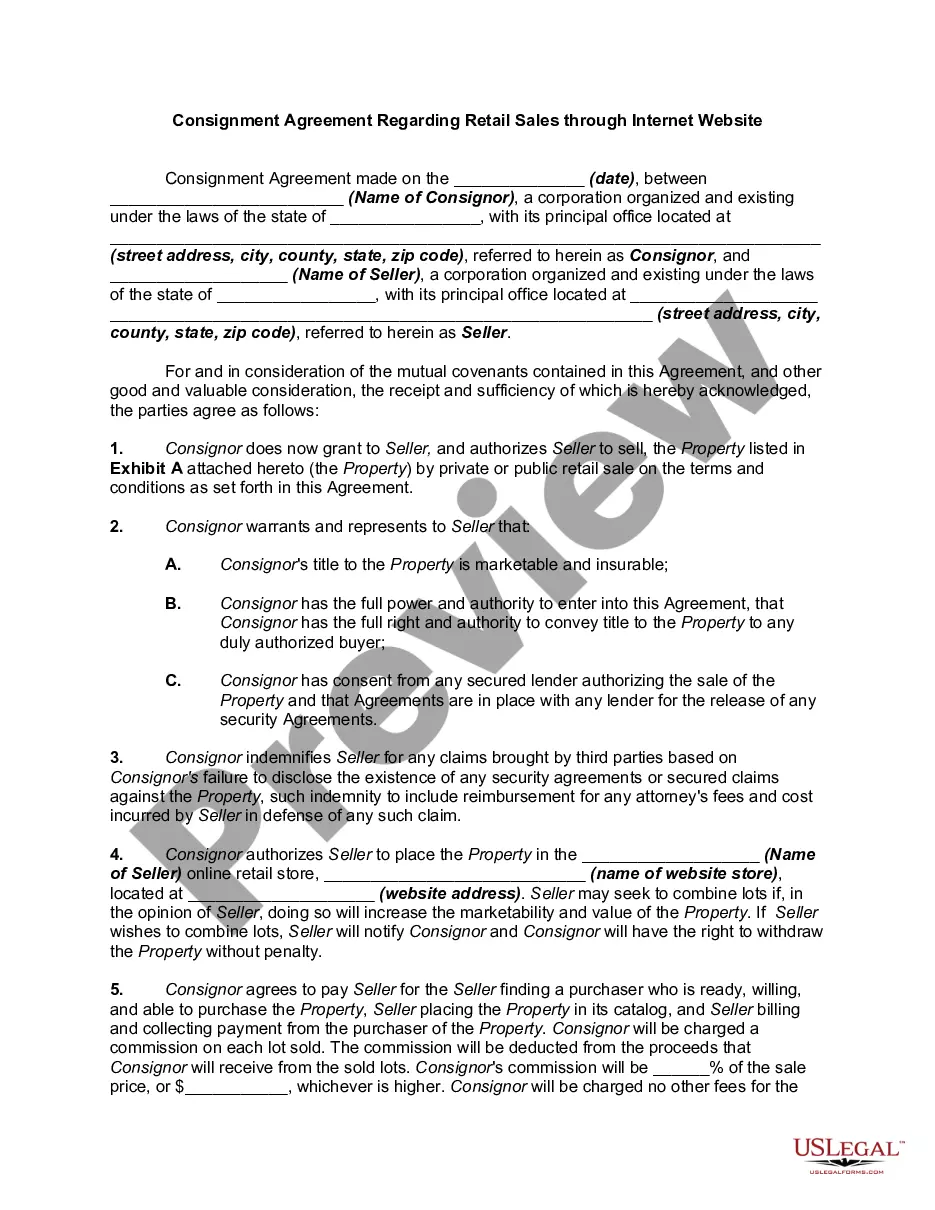

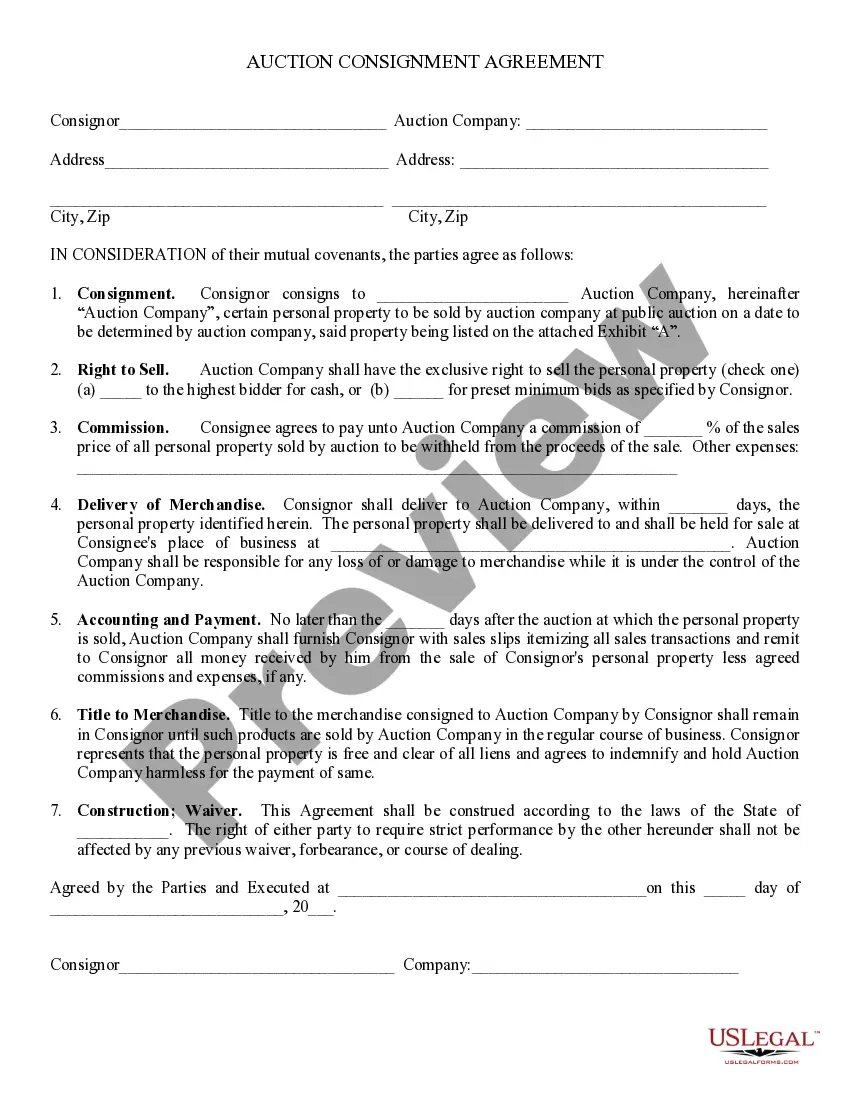

Consignment Account Example In Orange

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The consignor will make a journal entry for the goods received. The journal entry for the consignment accounting will have a credit and a debit. It is recorded as a debit for the consignment inventory, and a credit for the store's inventory. The consignee does not make an entry.

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)

Goods sent on Consignment Account is a real account. It is closed up by transferring its balances to trading accounting. It shall be shown on credit side of trading account. For each consignment these sets of accounts will be prepared separately.

Tracking Consignment Inventory: Methods and Tools Establish an ERP Integration Framework. Ensuring inventory levels in a consignment stock location and within the ERP are accurate is essential. Leverage Mobile Data Collection Tools. Apply Remote Management Functionality.

The journal entry accounts for the sales and expenses of the consignment inventory. No entry is made by the consignee. It's important to note that the import duty of 200 is debited to the consignment inventory account.

Consignment accounting is a type of business arrangement in which one person send goods to another person for sale on his behalf and the person who sends goods is called consignor and another person who receives the goods is called consignee, where consignee sells the goods on behalf of consignor on consideration of ...

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)

Abnormal loss arises due to certain conditions like theft of goods, damage to goods due to substandard material, faulty equipment or natural calamities like fire, earthquake, floods, etc.

They expected a normal loss of ₹10,000 under regular conditions. Fortunately, they are covered by insurance, and the insurance claim is approved for ₹40,000. In this example, the abnormal loss is calculated as ₹10,000 (normal loss) - ₹50,000 (actual loss) = ₹-40,000, indicating a ₹40,000 higher loss than anticipated.