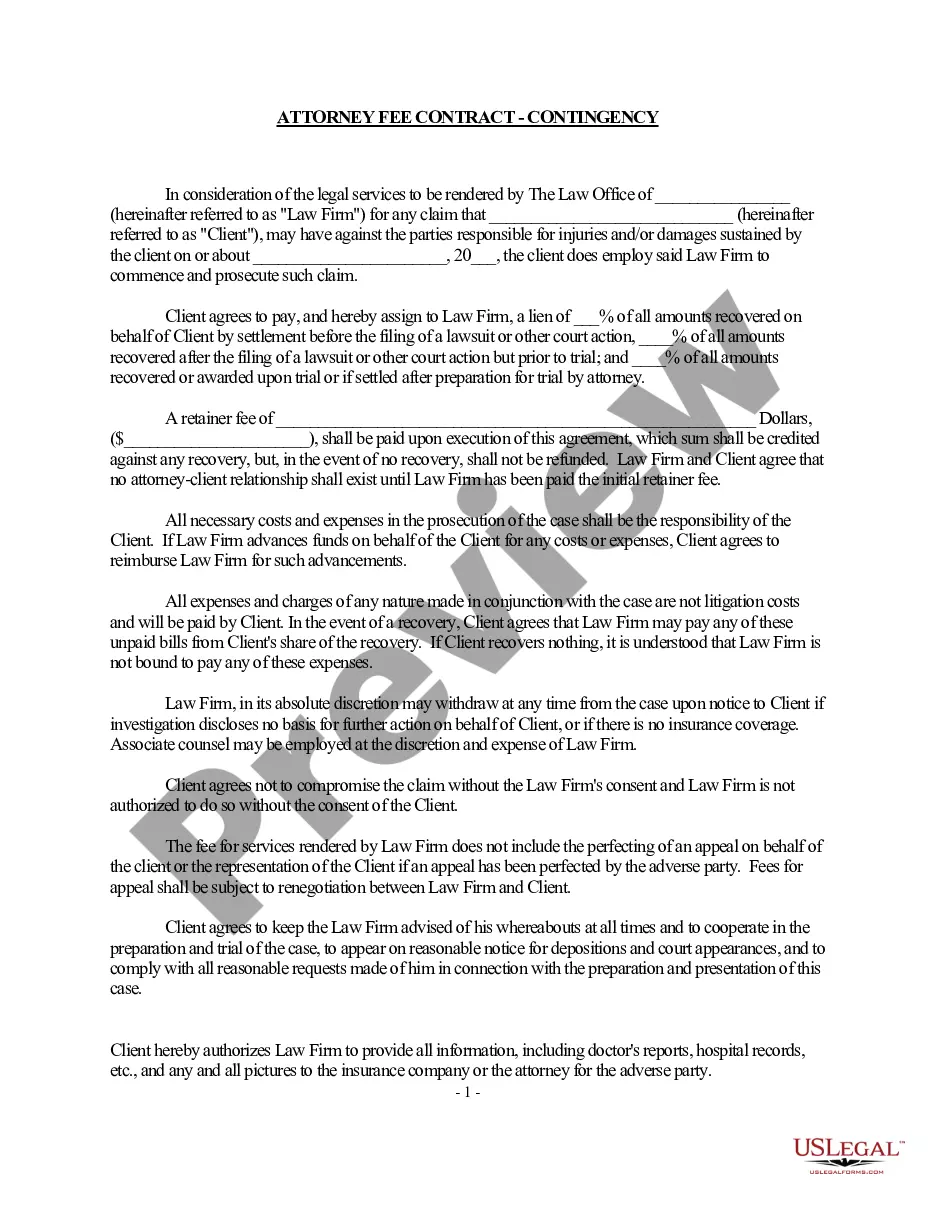

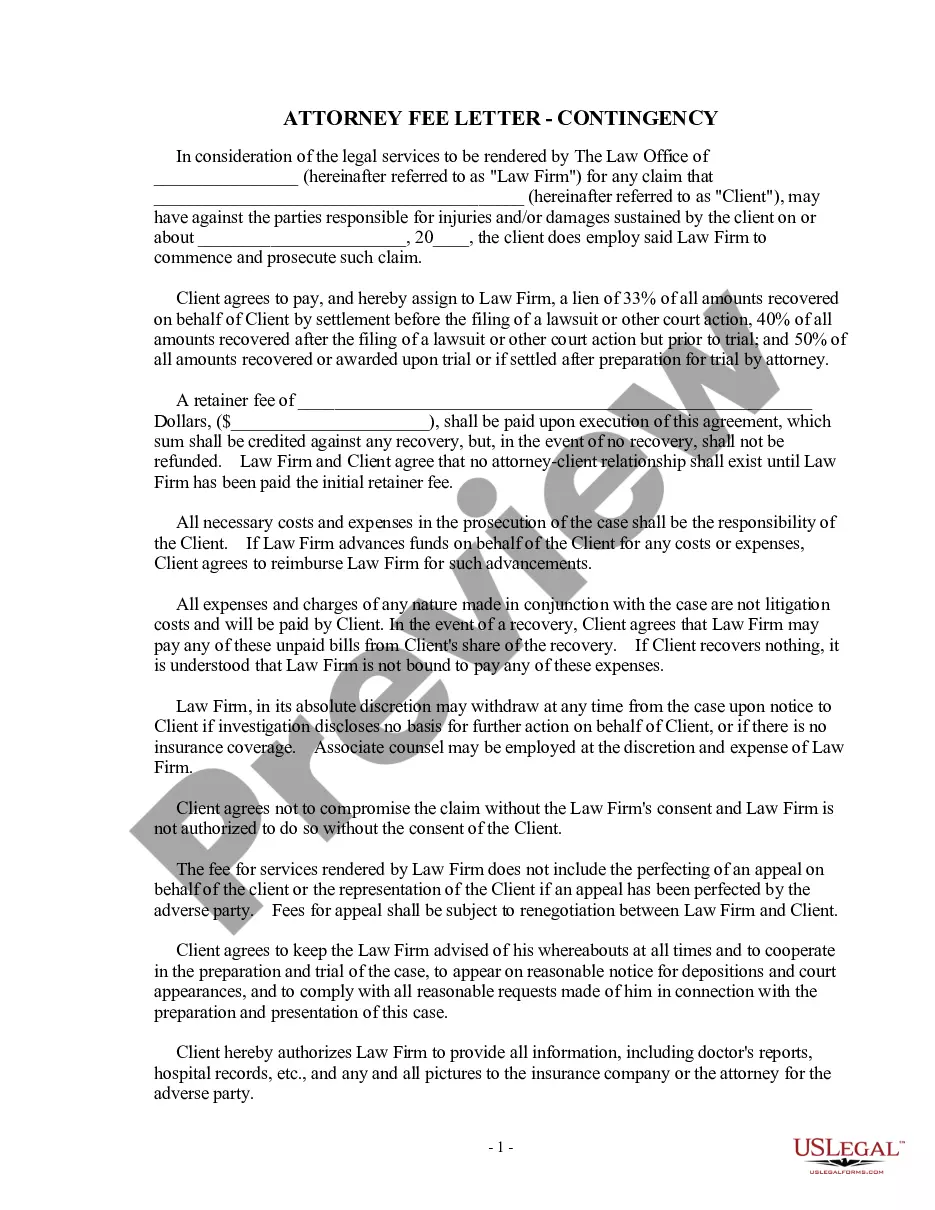

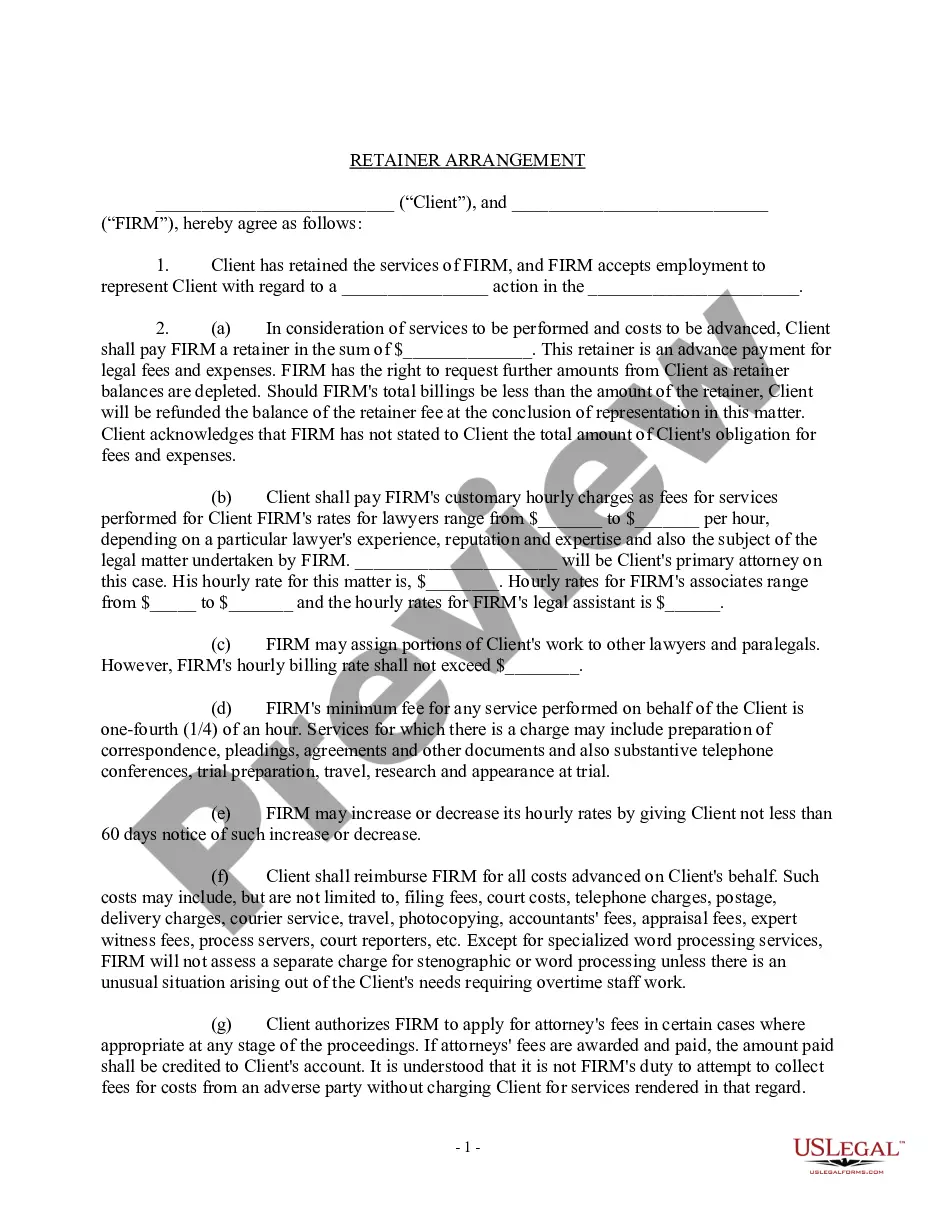

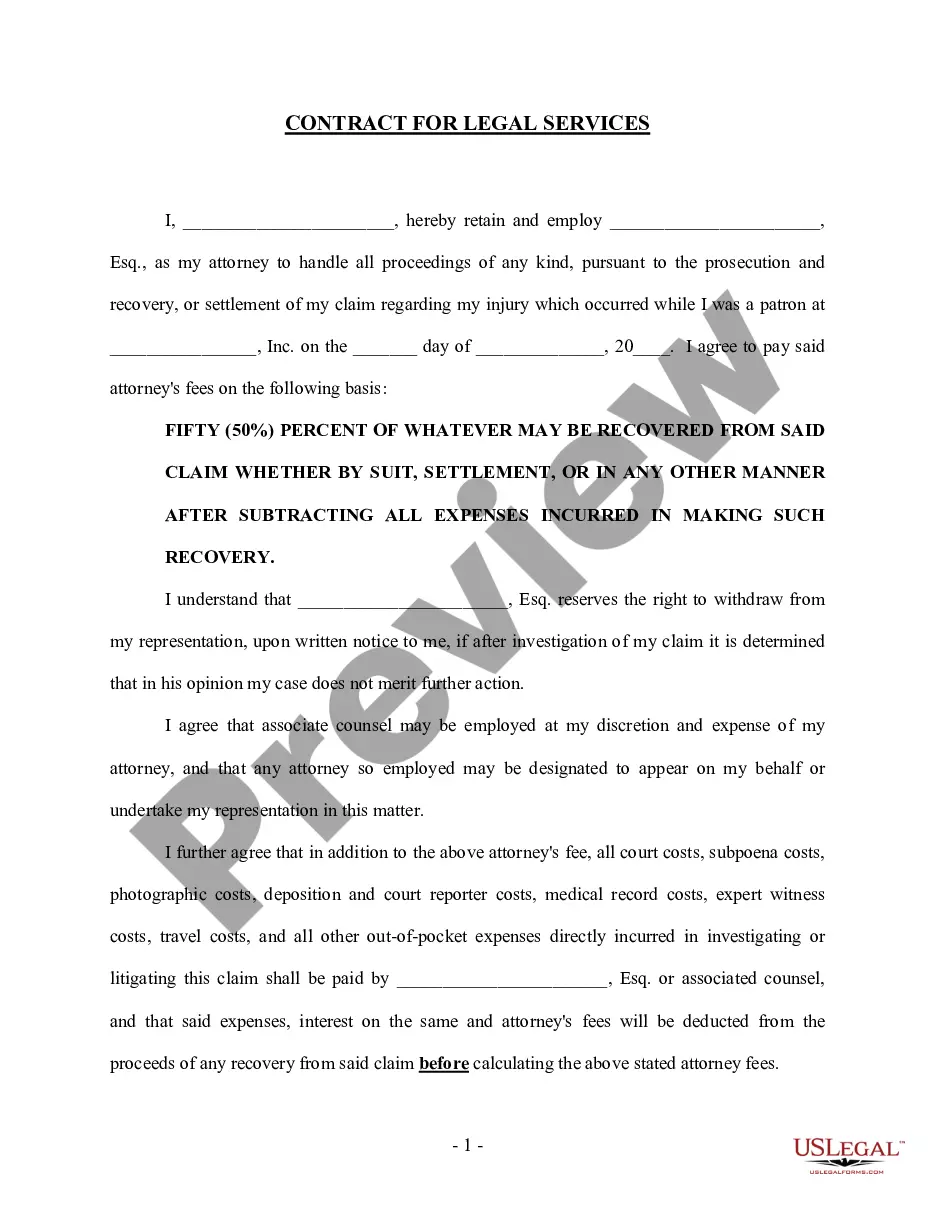

Contingency Fee For Erc In Hillsborough

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The ERC budget is supported by the European Commission and is supplemented by contributions from the EU associated countries.

The statute of limitations generally expired on April 15, 2024, for ERC 2020 claims and will expire on April 15, 2025, for ERC 2021 claims.

The IRS has ended its moratorium on processing employee retention tax credit claims that were filed after September 14, 2023, through January 31, 2024.

Calculating credits for 2021 The ERC applies only to the first three financial quarters of 2021, and the eligible wages for each of these quarters are calculated at 70%. As such, the credit per employee per quarter maxes out at $7,000.

The statute of limitations (SOL) on amending payroll tax returns (Form 941-X) for 2021 ends on April 15, 2025, and the ERC ends on the same date.

Open Form 1120, p1-2. Scroll down to the Salaries and Wages Smart Worksheet. Enter the employee retention credit on Line G, Other credits.

Credit amount The total ERC benefit per employee can be up to $26,000 ($5,000 in 2020 and $7,000 per quarter in 2021).

Going forward, the only way to apply for the ERC is to file an amended Form 941X (Quarterly Federal Payroll Tax Return) for the quarters during which the company was an eligible employer.

Amount per quarter: Each employee has $10,000 in qualifying wages per quarter, and 70% of this amount is $7,000 per quarter. Amount per employee: Since Company A is eligible for the ERC for all the available quarters, each employee's quarterly credit is multiplied by 3, which equals $21,000 per employee for the year.

Reminder: If you file Form 941-X to claim the Employee Retention Credit, you must reduce your deduction for wages by the amount of the credit for that same tax period.