Cease And Desist Sample Letter For Collection Agency In Chicago

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

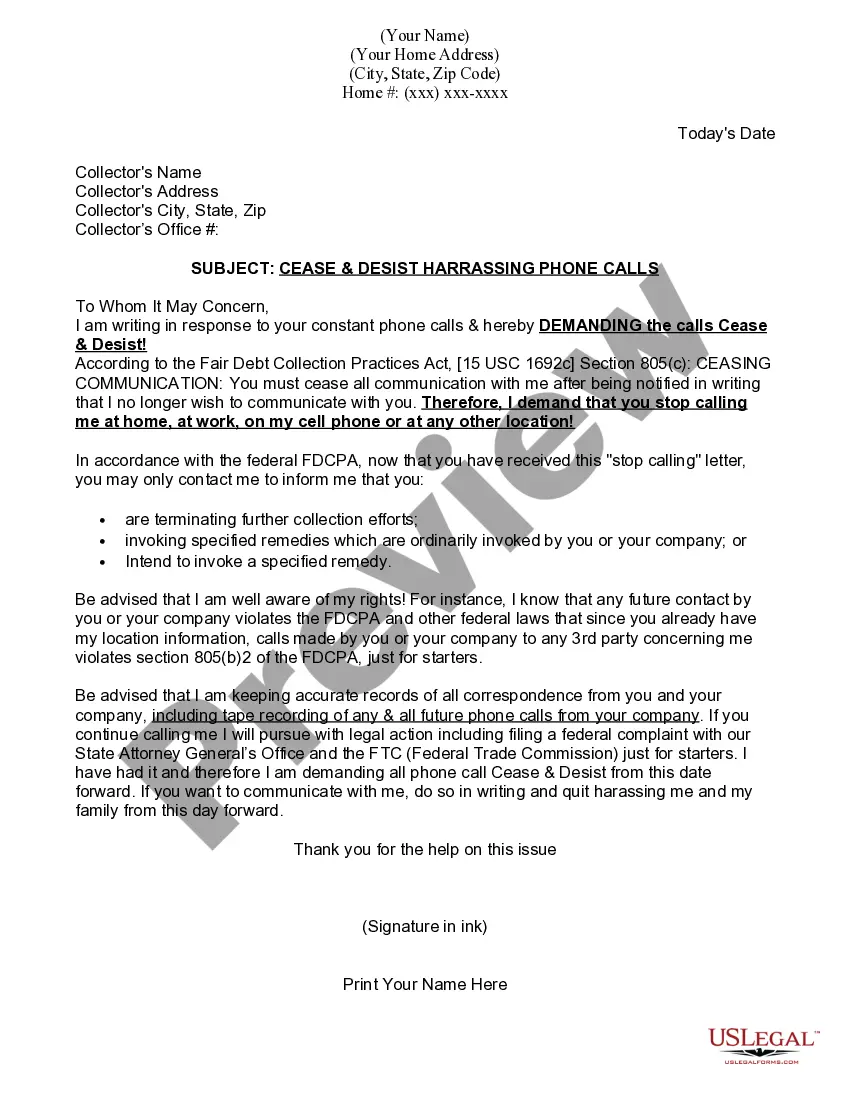

If you write a letter, instead of using the tear-off form, the debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request the debt not be reported to credit reporting agencies until the matter is resolved or ...

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

You'll want to include specific information concerning your account in your debt settlement letter. List your name, account information, the original creditor of the debt, and the debt collection agencies identifying information. Include the current amount you owe and the amount you'd like to offer to settle the debt.

If you are writing the letter yourself, you should include the following information: Your name and contact information. Name and contact information of the person or business being asked to stop the behavior. Specifics about the activity you wish them to stop.

The Fair Debt Collection Practices Act lays out the rules for debt collectors and states that if the creditor is told to stop contacting the debtor, they must comply. If the harassing calls and letters persist, a cease and desist letter can be sent by an attorney to formally advise the creditor to stop violating the de.

What is the 11 word credit loophole? The 11 word credit loophole does not exist, despite common misconceptions. If you're wondering, the phrase “Please cease and desist all calls and contact with me immediately” is often mistakenly believed to have special legal power.

A cease and desist letter is a formal written request that tells a debt collector to stop contacting you. It is your right under the Fair Debt Collection Practices Act (FDCPA) to limit how debt collectors can communicate with you.

Debt Relief Calculator: - You Can Use an 11 Word Phrase to stop debt collectors in their tracks. Here's the phrase: Please cease and desist all calls and contact with me, immediately. After you stop the debt collectors, you can then understand which options you have to resolve your debt. He.

Bottom line: You can stop a collection agency from calling you by writing them a letter telling them not to call you anymore- that you're not paying the debt, and why. If they call again, then google ``FDCPA attorneys'', call one, tell them whats going on.